How prepared are workers’ compensation systems for COVID-19?

Workers' Compensation Perspectives

MARCH 23, 2020

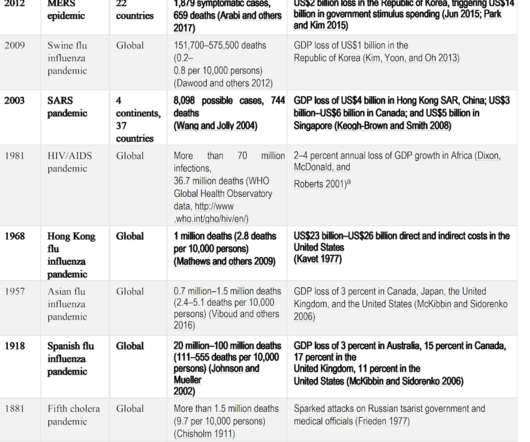

The “Unknown” occupational disease risk in workers’ compensation When workers’ compensation systems started a century ago, the focus was “industrial accidents”. page U47] Over time, most workers’ compensation systems adapted to include coverage for occupational diseases. Premiums and deductibles may be high.

Let's personalize your content