This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

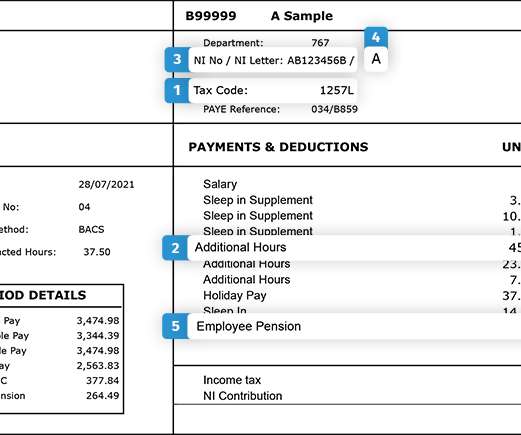

As an employer, you are responsible for withholding various taxes from employees’ wages. After you subtract all of the taxes and other deductions, money left over is considered take-homepay. Read on to learn more about what is take-homepay and how to calculate it. What is takehomepay?

At its core, a workplace pension is a retirement savings plan organised by an employer for the benefit of their employees, who also contribute to the pension. As of 2012, the introduction of auto-enrolment mandates all employers to provide a workplace pension. Net Pay contributions from your employees is deducted before tax.

This means people can earn £12,500 tax-free, and only start paying tax on income over that amount. However, if they have any other form of income, get benefits-in-kind from their employer (health insurance, life insurance or a company vehicle etc) or claim tax relief for any other reason, it will affect this tax code. Pension payments.

As an employer, you’re obliged to provide your staff with a workplace pension – a mandate made compulsory by the UK government in 2012. The required minimum contribution is set at 8%, typically comprising of a 3% contribution by the employer and a 5% contribution by the employee. Is your provider helping with this?

If you’ve been reading here for a while, you’ll recall that we’ve talked a lot about how millennials and the new generation Z (which includes those born between 1996 and 2012) are poised to transform the work place with their command of all things tech and desire to make the world a better place.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content