This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As an employer, you are responsible for withholding various taxes from employees’ wages. After you subtract all of the taxes and other deductions, money left over is considered take-homepay. Read on to learn more about what is take-homepay and how to calculate it. What is takehomepay?

As of 2012, the introduction of auto-enrolment mandates all employers to provide a workplace pension. More complex aspects like varying tax relief methods and payroll integration will be covered later. Which Tax Relief Method is Used? Relief at Source pension contributions from your employee are taken after tax deduction.

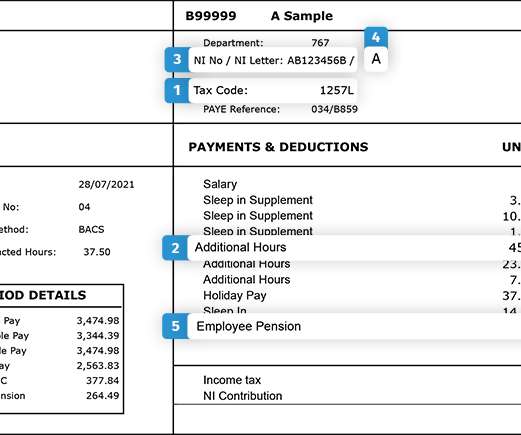

It’s worth remembering that it’s an employee’s responsibility to check they’re on the right tax code, as it impacts how much tax they pay – whether it’s too much tax or too little. For the 2021/22 tax year (and through to 2025/26), the tax code for most people under 65 who only have one job or pension is 1257L.

As an employer, you’re obliged to provide your staff with a workplace pension – a mandate made compulsory by the UK government in 2012. In a nutshell, this mechanism allows employees to maintain their pension contributions and even enjoy a slightly higher take-homepay. Is your provider helping with this?

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content