This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A new report has found that small businesses that purchase their group healthinsurance online or through payroll vendors saw the largest premium hikes in 2022, significantly higher than those that went through brokers. Since 2018, individual premiums have increased by 21% while family premiums have increased by 18%.

The traditional concept refers to legally mandated benefits plus a few voluntarily added by employers. Employers are responding with a menu of voluntary employee benefits, driven by generational shifts and technology that is dramatically changing the workplace. . labor force with 56 million people working or looking for employment.

Employment laws continue to evolve, and 2018 will usher in some big changes in two of our most populous states, California and New York. The HR world is abuzz with all the implications of implementing New York state’s paid family leave legislation and California’s ban-the-box law, both of which went into effect January 2018.

Despite group healthinsurance costs expected to rise 5.4% this year, the tight labor market is forcing employers to prioritize enhancing benefits over cost-cutting measures, according to a new report by Mercer. The expected healthinsurance cost growth of 5.4% What employers are doing.

While it is too soon to know whether the Fifth Circuit’s decision is an anomaly or a harbinger of greater judicial oversight of advisory opinions, employer plan sponsors, especially those in the Fifth Circuit, will want to pay close attention to future developments in this area. Department of Labor , No. 20-11179, 2022 WL 3440652, __F.

(Editor’s Note: Today’s post is brought to you by our friends at ComplyRight , providers of practical, affordable products and services that help employers of all sizes streamline essential tasks and compliance with federal, state, and local employment laws. The new due date to provide Forms 1095-B or 1095-C is now March 2, 2018.

Here are 12 tax topics to consider: Itemized Deductions- Only about 10% of taxpayers can itemize since the Tax Cuts and Jobs Act went into effect in 2018. Tax-Deferred Investing - One way to avoid a higher tax bracket is to increase tax-deductible contributions to an employer retirement plan (e.g., 401(k), 403(b), 457, TSP).

The time when the IRS offers relief from financial penalties to employers that make errors on their group healthinsurance reporting forms has come to an end. The change starting with the 2021 tax reporting year means that employers can face steep penalties for mistakes on their forms. Issues to bear in mind.

The dip, while seemingly small, represents millions of workers that have opted for other plans as employers are offering a greater variety of plans to their employees, including preferred provider organizations (PPOs) and health maintenance organizations. Employers can also contribute to the account.

The dip, while seemingly small, represents millions of workers that have opted for other plans as employers are offering a greater variety of plans to their employees, including preferred provider organizations (PPOs) and health maintenance organizations. Employers can also contribute to the account.

Stop-loss insurance contracts offer important protection for self-funded employers—but employers must ensure they’re providing the right coverage. Responsibly transitioning to self-funded healthinsurance can provide cash flow flexibility for some employers—and they are taking the plunge. In 2018, 38.7%

Healthcare is an essential and a necessary investment for both employers and employees. Do they drive down a company’s health investment costs or not? A study conducted by Harvard in 2015 found for every dollar spent on wellness programs, the employer saves $3 in healthcare costs and another $3 in absenteeism. Let us find out.

In fact, Forbes magazine named Cox Automotive to its first-ever list of America’s Best Employers for Diversity in 2018. Horizon Blue Cross Blue Shield of New Jersey (BCBSNJ) has offered healthinsurance to New Jersey families and businesses since 1932. Horizon Blue Cross Blue Shield of New Jersey.

If you’re like most business owners, one of the biggest things you may worry about in relation to your company is the cost of providing healthinsurance to your employees. In one 2018 report, almost 80 percent of respondents said they worry about the cost of health benefits. world of healthinsurance.

Households released in May 2018. The report provides insight into the financial health of families across America, examining factors like employment, student loans, and retirement. If you are currently employed, there is one change you can make to start saving: Enroll in a Health Savings Account (HSA). The tax savings.

Through this portal, eligible persons who did not file taxes in 2018 or 2019 can enter basic identifying information so the government can easily distribute their stimulus payments. . Reach out to your employer for clarification if you sense something is suspicious about a Zoom invitation. .

Individual Coverage Health Reimbursement Arrangements (ICHRAs) were rolled out prior to COVID-19 striking the United States, but the demand for this new product is expected to skyrocket, as more and more employers look for ways to bring stability to their healthcare costs. How does an ICHRA work? What are the employee classes?

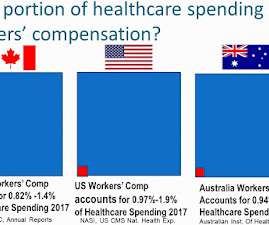

Workers' compensation is a primary payer in the event of an injury in the course and scope of employment. Those benefits are usually the only recovery an injured worker may receive from the employer. In broad terms, it is in the best interest of the employee and the employer that the tort recovery is maximized.

ROUND ONE: Which account(s) is funded by the employer? An HRA is always funded by an employer (and only the employer). According to the 2018 Bright Ideas quiz just one in two respondents understand that an HRA is solely funded by the employer. HRAs, on the other hand, are owned by the employer. HRA or HSA?

Viewing health & welfare benefits as a business investment is a mindset shift. Our 2019 Employer Education Series is designed to help you get more bang for your benefits buck. Corporate Synergies is set to launch its 2019 Employer Education Series. Don’t Miss Our 2019 Employer Education Events: Get Info Here.

The first is related to health issues, such as healthinsurance. On the health front, there’s a lack of employee awareness and understanding of certain benefits, including healthcare savings and caregiving support. 62% of those caregivers reported that their employer is unaware of those commitments.

These protections include, for example, the prohibition of discrimination based on health status, the prohibition of preexisting condition exclusions, and the prohibition of lifetime and annual dollar limits on essential health benefits. Employer Takeaway Written comments must be received by Sept. 11, 2023, to be considered.

What they have in common is that both are recipients of the 2018 Genesis Community Scholarship Fund. On June 5, 2018, at Town Hall in Lexington, Massachusetts, they were among a group of 75 high school and college students who received help to defray the cost of a college education. What Employers Are Doing About Student Loan Debt.

Job Market Report, two in three job seekers agree that workplace benefits are more important to them now than they were before the pandemic, and 80 percent think that employers need to reevaluate their benefits package. HealthInsurance, Telemedicine and Wellness Programs. Other Common Insurance Options and Voluntary Benefits.

So far, the trend toward retail pharmacy, PBM and healthinsurance industry consolidation doesn’t seem to benefit all stakeholders. Here’s why… Insurance industry consolidation is occurring at an unprecedented rate. Healthinsurance industry consolidation hasn’t been good for healthcare consumers or employers.

If you’ve been around small to midsize businesses for any amount of time over the last decade, you’ve no doubt seen or experienced the frustrations of navigating healthinsurance. And those players often come armed with healthinsurance options that small businesses like yours don’t have access to or can’t afford to offer on your own.

Older workers approaching full retirement age (where they can begin receiving 100% of Social Security), face daunting decisions this, Medicare, and retirement plans such as health savings accounts (HSAs) and 401(k)s. As an employer, you can help Baby Boomers with the retirement benefits education and planning process in 3 ways.

When Rexall was purchased by McKesson Drugs in 2018, it was down to just over 400 stores , largely in Canada. Pharmacies evolved into retail outlets, expanding offerings to include groceries, gifts, health and beauty aids and more. Others that employed the catalog model, such as J.C. I ate many a $.25 See Shrinkflation (December 2021).

There is an $18,500 limit (for 2018) on how much employees can contribute to a 401(k) plan. One exception is if the distributions are made to a participant after separation from employment if the separation occurred during or after the calendar year in which the person reached age 55. Can I stay on company healthinsurance?

Sometimes benefits are paid for wholly by employers; other times they are paid for by employees, and sometimes the expenses are shared. How the benefits expenses are shared (or not) is determined by the employer. The most expensive benefit to offer is healthinsurance. per hour worked in March 2018.

The federal law has been around for a decade, yet many employers still don’t know exactly how to comply. GINA essentially bars using genetic information in employment decisions and bars acquiring genetic information improperly. GINA bars employers from discriminating against or harassing employees based on their genetic information.

Failure to confine and fund the medical cost to the workers’ compensation system by definition will externalize those costs to someone else (often the tax payer or premium payers for other healthinsurance programs, the worker, worker’s family or community, other employers, or other employees of group insurance plans).

A termination letter is an official written statement that informs an employee at the end of their employment with a company. It is usually given from an employer to an employee. Share information on benefits like healthinsurance and similar. What Is A Termination Letter? 2 Being dismissed from a job is never a cinch.

Employee benefits are typically the second-highest expense for employers—right behind payroll. Not knowing what the benefits renewal rate will be until the end of the plan year complicates the balance that employers must strike between offering a rich plan that employees appreciate at a cost the finance team can live with. As Seen In.

First, it’s important to note a common priority (not surprisingly) across all generations: healthinsurance. The Society for Human Resource Management noted in its 2018 Employee Benefits Report that 95 percent of employers offer at least one retirement plan to workers. ” The generational constant.

These four conditions are the most likely mental health conditions employers will encounter, sometimes in combination. The most likely combination of mental health issues in the workplace is depression and anxiety. How you as the employer handle that worker must comply with the ADA.

Are you paying insurance premiums for people who aren’t qualified to be on the plan? For some employers, too often, the answer is “yes,” their benefits program includes ineligible dependents. In our experience, we find that nearly 10% of dependents enrolled in employee health & welfare plans are not eligible to be in the program.

If improving diversity and building a more inclusive culture is one of your top goals for 2018, you are not alone. Look for opportunities to enable as much personalization of benefits as possible, from healthinsurance to tuition reimbursement to gym membership discounts.

According to Josh Bersin, managing people in an organization is said to be the number one challenge faced by companies in 2018. Workplace wellness initiatives are the health promotion activities or policies designed to enhance healthy behavior in the workplaces. Employee health and wellness initiatives are not a new concept.

So it stands to reason that there’s a resurgence of interest in long-term care and long-term disability insurance. As an employer, it’s important to understand the difference and educate employees on why they’d need each type of coverage. Long-term Care Insurance. It ends when the employee changes employers.

So it stands to reason that there’s a resurgence of interest in long-term care and long-term disability insurance. As an employer, it’s important to understand the difference and educate employees on why they’d need each type of coverage. Long-term Care Insurance. It ends when the employee changes employers.

Employers are realizing that they need to provide mental health care. However, simply offering mental health care isn’t necessarily enough. Employees also expect quality mental health care. Minimal coverage means costs can add up quickly, and many insurance plans only cover limited mental health-related needs.

Like almost every other industry, professional employer organizations (PEOs) have been forced by the global pandemic to ask themselves this question. Get an in-depth look at professional employer organizations and why you should consider partnering with one. “What is our industry’s new normal?” Click To Tweet. million to 3.7

Employers and carriers are now shifting from creating narrow networks just to reduce costs to developing smaller networks that focus more on value-based healthcare. Employers and carriers review qualitative elements to measure cost efficiency and high-quality outcomes (what those specific elements are will vary by network).

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content