This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Figuring that defined-contribution plans such as 401(k)s weren’t nearly secure as they should be after the passage of the Setting Every Community Up for Retirement Enhancement Act of 2019, Congress is taking another stab at it with the Securing a Strong Retirement Act of 2021 (H.R. Student loans and 401(k) plans.

The median household income in the United States was $67,521 in 2020, down from $69,560 in 2019. Dollar-cost averaging works best if investment deposits are “automated,” such as authorizing 401(k) plan payroll deductions or automatically debiting a bank account monthly for mutual fund share purchases.

Act of 2022 Expanding on the provisions laid out in the original SECURE Act of 2019, the SECURE 2.0 employer-sponsored 401(k) plans. Starting in 2024, employees’ annual contribution limits to some SIMPLE 401(k)s or IRAs will rise. Act of 2022 contains more than 90 provisions and covers 358 pages. The SECURE 2.0

The IRS uses those codes to determine compliance with other sections of the tax code, like 401(k) compliance and teasing out employees who earn too much to make tax-deductible IRA contributions. W-2 coding for 401(k) contributions. Use Code D to report 401(k) make-up pretax contributions.

Or will the amount of each paycheck in 2020 be lower than in 2019? For example, if you make $50,000 a year, your biweekly gross pay over 26 pay periods is $1,923.07, minus any deductions like health insurance, 401(k) contributions and taxes. Does this mean you’ll get an extra paycheck in 2020?

Despite all the options available, only 36 percent of non-retirees said in a 2019 survey that their retirement saving is on track. Despite all the options available, only 36 percent of non-retirees said in a 2019 survey that their retirement saving is on track. The missing retirement solution?

The money comes out of your paycheck before taxes, similar to a 401(k) and health insurance. Before saving with an HSA, you need to make sure you take care of the following: Enroll in a High Deductible Health Plan (HDHP). An HSA is typically funded through payroll deductions. You can view the 2019 HSA limits here.

It was signed into law on December 20, 2019, and has taken effect on January 1, 2020. It allows long-term, part-time workers to take part in 401(k) plans. You are no longer required to withdraw assets from IRAs and 401(k)s at age 70½. A Few Key Takeaways. It enables broader options for lifetime income strategies.

It was signed into law on December 20, 2019, and has taken effect on January 1, 2020. It allows long-term, part-time workers to take part in 401(k) plans. You are no longer required to withdraw assets from IRAs and 401(k)s at age 70½. A Few Key Takeaways. It enables broader options for lifetime income strategies.

To establish and make contributions to an HSA, an individual: must be enrolled in a high-deductible health plan ; cannot be covered under a second health care plan; and must not be eligible for Medicare or claimed as a dependent on someone else’s tax return. The FSA cap for 2019 is $2,700. What you need to know about health care FSAs.

The tax credit also applied if you suffered a significant decline in gross receipts, defined as a 50% drop in quarterly gross receipts when compared to the same quarter during 2019. Advances are limited to 70% of average quarterly wages paid during 2019. Expanded meal deduction. PPP loans are expanded. Tax extenders.

So, Benefit Resource brings you “4 Strategies to Strengthen Your Benefits Programs” 1) Add a Post-deductible HRA with an HSA. Win #2: There is no vesting requirement like a 401K. So combining an HSA with a post-deductible HRA just sweetens the deal and acts as a bonus. An HSA on its own can be a sought after benefit.

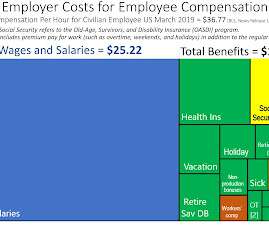

The March 2019 release [USDL-19-1002] provides the following synopsis: Employer costs for employee compensation for civilian workers averaged $36.77 per hour worked in March 2019, the U.S. Maryland has a corporate officer minimum at $57,200 and a maximum value set at $228,200 with partners as a flat rate of $56,900 [as at Jan 2019].

The formula for calculating net or spendable earnings may vary but is generally considered as Gross earnings less income taxes (state/federal/provincial) and other mandatory deductions. For single, high wage earners with few deductions, two-thirds of gross may marginally exceed 90% of net earnings.

Fixed pay – This is the accrued salary mentioned in the payslip or the fixed amount an employee gets at the end of the month minus the deductions (taxable). Supplementary Pay – Usually left to the company’s discretion, supplementary pay includes stock options, 401 (k) plans, bonuses, tips, etc.

Act of 2022 —90+ provisions focused on 401(k) and other retirement plans. which was enacted in 2019. Congress has chosen to pay for it by mandating that plans offering certain 401(k) features, like catch-up contributions, be made on an after-tax, Roth basis. 401(k) plans established after Dec.

In particular, traditional business financing options like bank loans have been declining since 2020 — where they fell 6% from 2019 (43% to 37%, respectively). For instance, if you were going to deduct the use of one of your vehicles from your taxes, you wouldn’t deduct its entire value for just one year. Why is that?

Retirement Plans: Such as 401(k) plans with employer matching contributions Retirement plans, especially 401(k) plans with employer matching contributions, are paramount among employee perks in the United States. A 401(k) is a tax-advantaged retirement savings program provided by employers.

In fact, one in four LGBTQ Americans say they’ve experienced financial challenges due to their gender identity or sexual orientation, according to a 2019 Morning Consult poll. These individuals are 5% less likely to have a 401(k) or retirement plan and 12% less likely to have an IRA.

They can access this site to get their pay stubs, make changes to their direct deposit, enroll/change health benefits , and even make adjustments to their 401k plans…” (Source: Capterra ) “Most things integrate with each other in some way or another to increase productivity.

Almost all American workers now depend on defined-contribution plans such as 401(k)s and 403(b)s to fund their retirements. State and the federal government have been taking significant steps to make it easier for more employers to set up 401 (k) retirement plans. Here are a few highlights. Texas) and Patrick J.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content