This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you’re a small business owner interested in starting a 401(k) plan for your employees, you already understand how they will benefit, but you should also understand how the plan will affect you. Sometimes, the traditional 401(k) plan doesn’t end up providing you the full benefit you’d hoped for.

Fortunately, there’s an often overlooked way to help employees build wealth and prepare for retirement. Why HSAs for retirementplanning? These accounts provide another way for your employees to diversify their efforts to prepare for retirement. Click below to get your free HSA retirement white paper.

The day after Thanksgiving, while many of us were fortunate enough to be reaching for leftover pie, the IRS released proposed regulations implementing the requirement that 401(k) plan sponsors permit “long-term part-time employees” to make elective contributions to a 401(k) plan. How did we get here?

For the first time, Americans as a whole aren’t saving nearly enough for retirement. According to data from Northwestern Mutual’s 2019Planning & Progress Study, fifteen percent Americans have no retirement savings at all. The post Americans don’t have access to retirementplans appeared first on The HR Digest.

Act of 2022 Expanding on the provisions laid out in the original SECURE Act of 2019, the SECURE 2.0 At its most basic level, the law encourages people to not only save money for retirement , but to save more and also become financially stable in the present. employer-sponsored 401(k) plans. The SECURE 2.0

Figuring that defined-contribution plans such as 401(k)s weren’t nearly secure as they should be after the passage of the Setting Every Community Up for Retirement Enhancement Act of 2019, Congress is taking another stab at it with the Securing a Strong Retirement Act of 2021 (H.R. Church plans.

IRS regulations have established standards for plans to approve financial hardships and a safe harbor for six types of hardships automatically considered to create an immediate and heavy need. Historically, the Code restricted 403(b) plans more than 401(k) plans in terms of the contributions and earnings available for hardship withdrawal.

Plaintiffs, a proposed class of current and former Baptist Health employees, sued the nonprofit health care organization in the Southern District of Florida, alleging that defendants breached their fiduciary duties in their management and selection of investments for the organization’s 403(b) retirementplan. See Dorman v.

Act of 2022 —90+ provisions focused on 401(k) and other retirementplans. which was enacted in 2019. Congress has chosen to pay for it by mandating that plans offering certain 401(k) features, like catch-up contributions, be made on an after-tax, Roth basis. Auto-enrollment plans.

Look beyond the 401(k) Employees tend to think of a 401(k) retirementplan as a standard, commonplace benefits offering. Furthermore, a 401(k) is focused on the future and long-term goals – a more urgent and timely concern for older employees closer to retirement.

Congress made several changes to retirementplans as part of the Consolidated Appropriations Act of 2023 , which recently passed both the House and Senate. The final bill contains several provisions affecting retirementplans under Division T of the bill titled “Secure 2.0 Act of 2022.”

This is a full time/part-time position and you are required to join us by December 23, 2019, Monday. The company has a retirementplan, applicable 90 days after your start date. On acknowledgement, details of the benefit and retirementplans will be shared. You will be responsible for (give job details here).

It was signed into law on December 20, 2019, and has taken effect on January 1, 2020. It aims to improve the private employer-based retirement system’s success by making it easier for companies to provide retirementplans. It allows long-term, part-time workers to take part in 401(k) plans.

It was signed into law on December 20, 2019, and has taken effect on January 1, 2020. It aims to improve the private employer-based retirement system’s success by making it easier for companies to provide retirementplans. It allows long-term, part-time workers to take part in 401(k) plans.

You also get to keep them into retirement and if you switch employers. In 2019, the houseplant craze hit and while some of you may have been enjoying your gardens before it was trendy, we’re still impressed with how many plant aficionados there are out there. We talked previously about how HSAs and 401(k)s pair nicely together.

A thoughtfully crafted retirementplan can positively impact employee morale. Increase the productivity of employees nearing retirement. A handsomely distributed retirementplan increases job satisfaction. Let's quantify the significance of retirement rewards.

Important Changes to Know About The Consolidated Appropriations Act of 2023 was signed into law in December 2022, and it’s collectively referred to as SECURE 2.0 – an update to the SECURE Act from 2019. encourages employers to provide retirementplans by offering tax incentives and credits. How does it do that?

The Internal Revenue Service (IRS) is strategically working to execute the statutory changes that were outlined by the Setting Every Community Up for Retirement Enhancement Act (SECURE Act) of 2019.

because it builds on the Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2019. proposals include: Expanding automatic enrollment in 401(k) and 403(b) retirementplans (for plan years beginning after Dec. The act is often referred to as “SECURE 2.0” Key SECURE 2.0 31, 2022); and.

The employee elected to contribute to a retirementplan. If an employee elected to contribute to a pre-tax retirementplan, their W-2 Box 1 wages are likely lower than their Box 3 wages. An employee’s elected retirementplan contributions are not subject to federal income taxes.

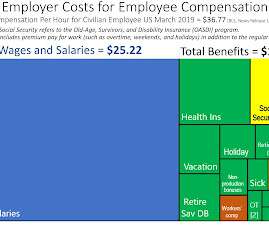

The March 2019 release [USDL-19-1002] provides the following synopsis: Employer costs for employee compensation for civilian workers averaged $36.77 per hour worked in March 2019, the U.S. Maryland has a corporate officer minimum at $57,200 and a maximum value set at $228,200 with partners as a flat rate of $56,900 [as at Jan 2019].

For example, in 2019, Walmart agreed to pay $14 million to settle a class-action lawsuit alleging that the company failed to pay appropriate overtime wages to its employees. Some jurisdictions now require certain types of preventative care to be included in employer-sponsored plans.

a long-awaited (and debated) package of retirementplan reforms. Given the breadth of the changes and the anticipated regulatory efforts to implement the new law, virtually all qualified retirementplans will need to be reviewed in conjunction with SECURE 2.0’s The wait is over for SECURE 2.0, may be viewed here.

These incentives span a wide array, from health benefits and retirementplans to flexible work arrangements, financial bonuses, and professional development opportunities. Paid parental leave, support for fertility-related expenses, and assistance with adoption or surrogacy costs are also part of the benefitws plan.

In fact, one in four LGBTQ Americans say they’ve experienced financial challenges due to their gender identity or sexual orientation, according to a 2019 Morning Consult poll. Gaps also exist when it comes to retirement savings among same-sex and LGBTQ couples.

Compensation and Benefits: Compensation Planning : Helps design and manage salary structures, bonuses, and other forms of compensation. Benefits Administration : Manages employee benefits, such as health insurance, retirementplans, and other perks.

Almost all American workers now depend on defined-contribution plans such as 401(k)s and 403(b)s to fund their retirements. State and the federal government have been taking significant steps to make it easier for more employers to set up 401 (k) retirementplans. Here are a few highlights.

Way back at the end of last year, Trump signed into law a bill that included one of the biggest overhauls to the way we manage retirementplanning in the US. In particular, the Setting Every Community Up for Retirement Enhancement. Don’t have a 401(K) plan but think it’s time to set one up?

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content