This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you’re a small business owner interested in starting a 401(k) plan for your employees, you already understand how they will benefit, but you should also understand how the plan will affect you. Sometimes, the traditional 401(k) plan doesn’t end up providing you the full benefit you’d hoped for.

Make sure you are getting the 401(k) match. Many employers will offer a 401(k) match up to a certain percentage. Additionally, contributions to a 401(k) are made will pre-tax dollars, so you save on taxes as well. That’s a lot of opportunities to use your HSA tax-free.

Act of 2022 Expanding on the provisions laid out in the original SECURE Act of 2019, the SECURE 2.0 employer-sponsored 401(k) plans. This enables workers to pay taxes up front on the funds they contribute, and then grow and withdraw these larger funds at a later date tax free. The SECURE 2.0 The SECURE 2.0

Figuring that defined-contribution plans such as 401(k)s weren’t nearly secure as they should be after the passage of the Setting Every Community Up for Retirement Enhancement Act of 2019, Congress is taking another stab at it with the Securing a Strong Retirement Act of 2021 (H.R. Tax credits for start-up costs.

As part of our continuing series on SECURE 2.0 , signed into law December 29, 2022, this post focuses on significant changes for section 403(b) tax-sheltered annuity plans (“403(b) plans”). Historically, the Code restricted 403(b) plans more than 401(k) plans in terms of the contributions and earnings available for hardship withdrawal.

The median household income in the United States was $67,521 in 2020, down from $69,560 in 2019. Dollar-cost averaging works best if investment deposits are “automated,” such as authorizing 401(k) plan payroll deductions or automatically debiting a bank account monthly for mutual fund share purchases.

Despite all the options available, only 36 percent of non-retirees said in a 2019 survey that their retirement saving is on track. Despite all the options available, only 36 percent of non-retirees said in a 2019 survey that their retirement saving is on track. Withdrawals for HSA eligible medical expenses are tax-free.

There are no tax penalties for incorrectly coding items reported in Box 12 of your W-2s. The IRS uses those codes to determine compliance with other sections of the tax code, like 401(k) compliance and teasing out employees who earn too much to make tax-deductible IRA contributions.

Act of 2022 —90+ provisions focused on 401(k) and other retirement plans. which was enacted in 2019. Congress has chosen to pay for it by mandating that plans offering certain 401(k) features, like catch-up contributions, be made on an after-tax, Roth basis. 401(k) plans established after Dec.

Or will the amount of each paycheck in 2020 be lower than in 2019? For example, if you make $50,000 a year, your biweekly gross pay over 26 pay periods is $1,923.07, minus any deductions like health insurance, 401(k) contributions and taxes. Similarly, federal income tax withholdings might differ on your paycheck as well.

The tax savings. It will help you save on taxes and on health expenses. An HSA is a tax-free benefit. The money comes out of your paycheck before taxes, similar to a 401(k) and health insurance. Because your gross income (your income before taxes) is reduced, you pay less in taxes.

builds on the Setting Every Community Up for Retirement Act (the “SECURE Act”), which passed in 2019. Catch-up contributions will now be subject to Roth after-tax treatment for those earning more than $145,000 in the prior year. Act of 2022.” An official summary of all of the provisions is available here. Increase in Cash-out Limit.

It was signed into law on December 20, 2019, and has taken effect on January 1, 2020. It allows long-term, part-time workers to take part in 401(k) plans. You are no longer required to withdraw assets from IRAs and 401(k)s at age 70½. It allows IRA owners to defer paying taxes on those funds while they are growing.

It was signed into law on December 20, 2019, and has taken effect on January 1, 2020. It allows long-term, part-time workers to take part in 401(k) plans. You are no longer required to withdraw assets from IRAs and 401(k)s at age 70½. It allows IRA owners to defer paying taxes on those funds while they are growing.

In particular, traditional business financing options like bank loans have been declining since 2020 — where they fell 6% from 2019 (43% to 37%, respectively). A fiscal year simply represents the 12-month period that a business uses for its accounting, taxes, and budgeting purposes. Why is that? The good news? What is a ROB?

Important Changes to Know About The Consolidated Appropriations Act of 2023 was signed into law in December 2022, and it’s collectively referred to as SECURE 2.0 – an update to the SECURE Act from 2019. encourages employers to provide retirement plans by offering tax incentives and credits. not signing up for your 401(k) plan).

According to a 2019 study by HealthView Services , couples in their 50s today are expected to pay around $400,000 in lifetime retirement health care costs. There is also an extra $1,000 additional contribution allowed for eligible individuals aged 55 or older at the end of the tax year. Love HSAs and want to keep reading?

In 2019, the houseplant craze hit and while some of you may have been enjoying your gardens before it was trendy, we’re still impressed with how many plant aficionados there are out there. We talked previously about how HSAs and 401(k)s pair nicely together. You also get to keep them into retirement and if you switch employers.

On April 5, 2022, the IRS released a proposed rule that would change the existing rules for eligibility for the premium tax credit (PTC). If this rule is finalized, the change would likely mean that more individuals will be newly eligible for a premium tax credit for coverage purchased through the Exchange. Employer Takeaway.

The law also extends expiring tax provisions and everything that could be jammed into 5,593 pages of federal legislation three days before Christmas. The key payroll provisions include: An extension of the paid sick/ family leave provisions and your tax credit for providing leave. Extensions of popular payroll tax provisions.

Contributions made by the account holder are generally tax-free, but withdrawals are only tax-free when used to pay for eligible medical expenses. Withdrawals for non-eligible expenses are allowed, but taxed and subject to a 20-percent penalty, until the employee reaches age 65. The FSA cap for 2019 is $2,700.

mostly provided traditional 401(k), while 68% also offered Roth 401(k) plans. Also known as the 401(k) bill, this makes it mandatory for businesses with 10 or more employees to offer a retirement solution to their employees. - The same study also revealed that 94% of the employers in the U.S.

You likely know that you must report an employee’s wages and withheld taxes from the previous year on Form W-2. If you imported information from your payroll software or used a tax preparer, you may not know the ins and outs of Box 1. Do not include pre-tax benefits in Box 1. About Form W-2 Box 1. So, what is Box 1?

Win #2: There is no vesting requirement like a 401K. Example: For 2019, an employer offers a high deductible health plan with a $3,000 individual deductible. While the IRS no longer provides tax-favorable treatment for bicycle commute programs, employers might consider building their own bicycle commute program.

The formula for calculating net or spendable earnings may vary but is generally considered as Gross earnings less income taxes (state/federal/provincial) and other mandatory deductions. Workers’ like Marion will have a higher proportion of their gross earnings withheld for taxes. Burton, Jr.,

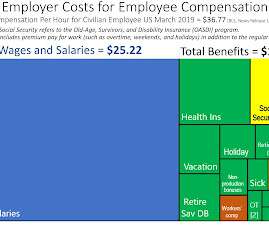

The March 2019 release [USDL-19-1002] provides the following synopsis: Employer costs for employee compensation for civilian workers averaged $36.77 per hour worked in March 2019, the U.S. Maryland has a corporate officer minimum at $57,200 and a maximum value set at $228,200 with partners as a flat rate of $56,900 [as at Jan 2019].

For example, in 2019, Walmart agreed to pay $14 million to settle a class-action lawsuit alleging that the company failed to pay appropriate overtime wages to its employees. Changes to tax laws affecting employee benefits Tax laws are always in a state of flux, and this is no less true when it comes to those affecting employee benefits.

Supplementary Pay – Usually left to the company’s discretion, supplementary pay includes stock options, 401 (k) plans, bonuses, tips, etc. LinkedIn’s 2019 Workforce Learning Report 3. You can usually gauge how employee-centric an organization is by looking at its benefits package. What are rewards?

Among other changes, it: Requires automatic enrollment for new 401(k) and 403(b) plans that are first established after SECURE 2.0’s Among other changes, it: Requires automatic enrollment for new 401(k) and 403(b) plans that are first established after SECURE 2.0’s Building on SECURE Act of 2019.

Retirement Plans: Such as 401(k) plans with employer matching contributions Retirement plans, especially 401(k) plans with employer matching contributions, are paramount among employee perks in the United States. A 401(k) is a tax-advantaged retirement savings program provided by employers.

In fact, one in four LGBTQ Americans say they’ve experienced financial challenges due to their gender identity or sexual orientation, according to a 2019 Morning Consult poll. These individuals are 5% less likely to have a 401(k) or retirement plan and 12% less likely to have an IRA.

It saves the time needed to move from one module to another and since the system talks to each other pretty well, getting data is also seamless…” (Source: G2 ) “It is a performance management, benefits administration , and core HR tool that tracks your tax documents and payroll/benefits. Paycor is a must have software.

According to Student Loan Hero , 69 percent of the Class of 2019 took out student loans, and they graduated with an average debt of $29,900. But it’s not just like the Class of 2019 was on some kind of scary spending spree. Further, offering to repay a portion of student loans can help offset a lower base salary.

The Treasury Inspector General for Tax Administration has a flyer you may want to hand out to employees. The core payroll -related provisions include: An extension, expansion, and reordering of the paid sick/family payroll tax credits. A requirement for employers to subsidize COBRA and a payroll tax credit for doing so.

Congress and the IRS know that many owners of tax-deferred retirement accounts (e.g., traditional IRAs, 401(k)s, 403(b)s, TSP), especially super-savers with $1 million + balances, will die and leave money in their plans. the so-called stretch IRA). the so-called stretch IRA). Now they have 10 years to withdraw inherited funds.

Almost all American workers now depend on defined-contribution plans such as 401(k)s and 403(b)s to fund their retirements. State and the federal government have been taking significant steps to make it easier for more employers to set up 401 (k) retirement plans. Here are a few highlights. Texas) and Patrick J.

SECURE) Act of 2019, which was enacted as part of the broader Further Consolidated Appropriations Act (no nifty acronym for that one!), has a number of important repercussions for any business that administers a 401(K) (or has thought of doing one, but always felt that it wasn’t financially feasible). This bill has you covered!

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content