This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For years,high-deductible health plans have been the most common type of health insurance that employers offer. How HDHPs work and their drawbacks An HDHP typically featureslower monthly premiumsin exchange for ahigher annual deductible. HDHPs surged in popularity between 2013 and 2021, peaking at 55.7% enrollment.

An employment tribunal has ruled that a former hotel worker employed by Luxury Family Hotels was unfairly dismissed and had an unlawful deduction of wages. The tribunal judge ruled that unlawful deductions were made from Murphy’s pay and ordered the hotel pay her £3,044.18.

It’s no secret that the use of high deductible health plans (HDHPs) continues to skyrocket. For 2020, the IRS defines an HDHP as any plan with a deductible of at least $1,400 for an individual or $2,800 for a family.

provisions make some significant changes for retirement plans , but CAA 2023 also extends the telehealth plan safe harbor for high-deductible health plans (“HDHPs”) that were first introduced in the 2020 CARES Act. Generally, a participant must pay their HDHP’s deductible before the plan can cover medical services.

Effective April 1, 2022, high-deductible health plans can once again offer first-dollar coverage for telehealth and other remote services without making participants ineligible for health savings account (“HSA”) contributions.

Does this mean you’ll get an extra paycheck in 2020? Does this mean you’ll earn more than your annual salary in 2020? Or will the amount of each paycheck in 2020 be lower than in 2019? lower each pay period during 2020 (although you’d make the same total salary). This means that gross pay would be 3.7%

1 payday back into 2020, you’d still have 27 biweekly pay periods, this time in 2021. Hourly-paid nonexempts are impacted only to the extent of withholding and deductions. Employees’ benefits deductions and allowances (e.g., Most payroll systems allow you to suppress benefits’ deductions for the extra pay period.

Deductible options The words “health”, “coverage”, “insurance”, and “deductible” were among the most frequent words to appear when participants were asked in our survey what was missing from their benefits. Specific responses included: “A lower deductible or copay options would be an improvement.” Deductibles are too high.

Healthcare is complicated, so how can you get the most out of Open Enrollment 2020? These are general guidelines to give you a basic understanding of your healthcare expenses from the past year and guide your decisions for Open Enrollment 2020. You’ll also want to factor in your deductible.

2020 HSA Contribution Limit. The HSA limits for contributions are set to increase in 2020 according to Revenue Procedure 2019-25 , released today by the IRS. The minimum deductible requirements and maximum out-of-pocket requirements are set to increase in 2020. Individual : $3,550 (up from $3,500 in 2019).

The percentage of workers covered under HDHP plans has increased from four percent of all employer-sponsored health insurance plans in 2006 to 31 percent in 2020. A high deductible health plan (HDHP) paired with a Health Savings Account (HSA) is growing in popularity because it allows employees to pay for medical expenses tax-free.

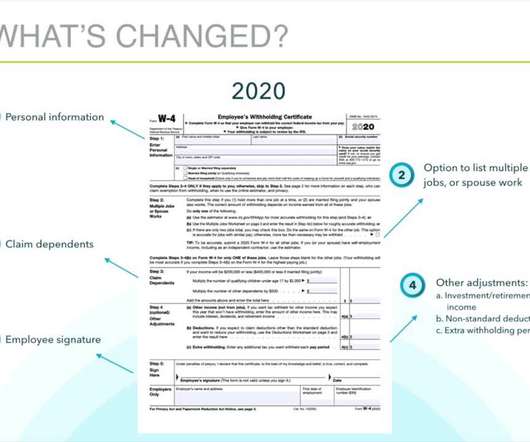

On December 5, 2019, the IRS released the final version of the 2020 Form W-4, which was retitled as the Employee’s Withholding Certificate. The 2020 version of Form W-4 is presented on a single, full-page– followed by instructions, worksheets, and tables. Deductions other than the standard deduction. What's next?

HSAs are paired with a high-deductible health plan (HDHP) and have an annual contribution limit. A health savings account (HSA) is a tax-advantaged savings account a family or individual can use to pay for qualified medical expenses. Each year, the IRS adjusts the guidelines regarding HDHPs and HSA contribution limits.

If you sponsor a high deductible health plan (“HDHP”) and have been tracking telehealth relief, your head may be spinning and rightfully so! There have been various laws and guidance impacting HDHPs and telehealth since 2020 and most recently, new legislation extended relief for 2023 and 2024 plan years.

The IRS announced the 2021 HSA contribution limits in May in Revenue Procedure 2020-32 , as well as minimum deductible and maximum out-of-pocket expenses for the HDHPs (high-deductible health plans) that HSAs must be paired with.

More employees are enrolling in a high-deductible health plan (HDHP) each year, including more than half of U.S. HDHP vs. PPO deductible Nearly two-thirds of large employers provide their employees with the choice of an HDHP and a traditional health plan , such as a preferred provider organization (PPO).

The ever increasing cost of healthcare combined with uncertainty about coverage, deductibles and copays keep some employees from getting the medical care they need. According to the Kaiser Family Foundation, the average annual premium is $7,470 for single coverage and $21,342 for family coverage in 2020.

Tax deductions if you have a fleet of commercial vehicles Are you a small or large business owner with commercial vehicles, or a fleet manager? Rather than taking the traditional vehicle depreciation over time, business owners and fleet managers can now take immediate deductions during tax season.

The Australian Taxation Office (ATO) has created short-cuts for employers and workers in order to deduct certain home office expenses. For example, employees may deduct a rate of 52 cents per hour for operating costs in addition to $50 per year for work related phone and Internet costs.

One of the health insurance trends that went largely unnoticed in 2021 was that employers halted cost-shifting to their employees by reducing or holding steady workers’ deductibles and other cost-sharing. Among large employers (500 or more workers), the median PPO deductible for individual coverage remained steady at $750.

The median household income in the United States was $67,521 in 2020, down from $69,560 in 2019. Dollar-cost averaging works best if investment deposits are “automated,” such as authorizing 401(k) plan payroll deductions or automatically debiting a bank account monthly for mutual fund share purchases.

As a reminder, if an HDHP covers medical items and services before the participant satisfies the IRS minimum deductible (self-only or family), that coverage may disqualify the participant’s HSA contributions. Can an HDHP continue to provide pre-deductible coverage of COVID-19 testing and treatment without impacting HSA eligibility?

Employees may account for tax dependents in Step 3 of the 2020 W-4. Regulations on deducting employees’ meal expenses. This follows up on Notice 2018-76, which sets five criteria for corporate deductions for employees’ meals. But it is useful as a road map for what the IRS wants to accomplish by June 30, 2020.

Premium increases, higher deductibles and copays, and soaring prescription drug prices result in spikes in healthcare costs. Despite the decrease in health services accessed in 2020 due to the COVID-19 pandemic, national health expenditures are expected to reach $6.8 trillion by 2030 2.

More questions have been generated since the 2020 form went in effect on Jan. An employee who’s been working since before 2020 never filed a W-4. Does this mean we’ll have to individually calculate their pay each pay period to account for deductions in Steps 3 and 4? Here’s our roundup. How do we withhold now? Pretty close.

Only California employers that do not offer retirement plans are required to register for CalSavers and there are different registration deadlines depending on employer size, staggered over a few years as follows: Employers with 100 or more workers – The deadline for registration was June 30, 2020. 401(k) plans. 403(a) plans. 403(b) plans.

HDHP telehealth services — The CARES Act, signed into law in 2020 after the pandemic started, temporarily allowed high-deductible health plans to pay for telehealth services before an enrollee had met their deductible. 1, 2022, HDHPs must charge enrollees for telehealth services if they have not yet met their deductible. .

A new study has found that individuals enrolled in high-deductible health plans (HDHPs) are more engaged than their traditional plan counterparts during open enrollment, spending more time on choosing plans and using employer-provided tools to help them make their choices. workers were enrolled in them. In 2022, 32% were.

That’s up from 26% in 2020 and 2021. Even if you are providing them with a robust plan, there are often out-of-pocket cost-sharing and deductibles to contend with. For employees in high-deductible health plans, the costs can be steep. The rapid increase occurred in a year where inflation was at a 40-year high.

If you sponsor a high deductible health plan (“HDHP”) and have been tracking telehealth relief, your head may be spinning and rightfully so! There have been various laws and guidance impacting HDHPs and telehealth since 2020 and most recently, new legislation extended relief for 2023 and 2024 plan years.

If you’re covered by an HSA-eligible health plan (or high-deductible health plan ), the IRS allows you to put as much as $3,650 per year (in 2022) into your health savings account (HSA). It takes into account your health plan coverage type, deductible amount, number of years before retirement, monthly healthcare expense and more.

We wanted to share the main lessons BRI employees learned about financial wellness in 2020. . Health Savings Accounts (HSAs) are most appealing to an individual or family that has relatively modest medical care expenses, can afford a high-deductible medical plan and could take advantage of the substantial tax benefits of an HSA.

The 2023 spending bill signed into law on December 29th includes extending pre-deductible telehealth services coverage. WHAT IS PRE-DEDUCTIBLE TELEHEALTH COVERAGE? Pre-deductible telehealth coverage allows HSAs-qualifying high-deductible health plans (HDHPs) to cover telehealth and remote-care services on a pre-deductible basis.

1—all pre-2020 withholding-allowance based W-4s and the 2020 W-4, which is shaping up to be entirely different. The IRS has recently released the second drafts of the 2020 W-4 and Pub. 2020 Form W-4. The IRS released the second draft of the 2020 W-4 in mid-August. Instead, the draft is built on five “steps.”

While health savings accounts have grown in popularity, you can only offer them to employees who are enrolled in high-deductible health plans. You can claim a tax deduction for the funds you transfer to your employees’ HRAs, and the funds they withdraw from the accounts to reimburse for medical-related expenses are generally tax-free.

As well, a growing number of established insurers are starting to sell “virtual-first” plans, often with a zero-dollar deductible and no copays for all visits with virtual-only providers. As this technology matures, the number of services that can be handled via video or phone will continue to increase. 31, 2024.

How to help employees prepare for open enrollment 2020. Terms Employees Need to Know for Open Enrollment 2020. Health Plan Deductible – The amount a person pays for health care services before insurance coverage starts. How to Help Employees Prepare for Open Enrollment 2020. Top 10 Employee Benefits for 2020.

DCAP DEDUCTIONS: Employees can change their pretax contributions into dependent care assistance plans midyear to account for day camps not opening (not sleepaway camps), if their cafeteria plans allow midyear changes. Notice 2020-29, IRB 2020-21). What’s still not allowed: Employees can’t cash out their DCAPs.

Z: The vendor contracts with employees; employees can’t access more than their earned pay; employees pay only a nominal fee for the service; employers make payroll deductions and remit the amount to the vendor; the vendor can’t sue employees who default; and the vendor doesn’t run credit checks on employees. What regulating agencies say.

Download our full infographic below to learn about the actual cost of a free HSA: Despite a steady increase in consumer demand for health savings accounts, employers—even those that already offer an HSA-eligible high-deductible health plan—may struggle to see the value in offering an employer-sponsored HSA program. Cost #1: Show Me the Money.

With off-payroll working rules set to be extended to the UK private sector in April 2020, should end-clients be amending contracts, issuing new terms, or sticking with existing contracts? Equally the client will have additional employer NICs costs to bear and they will be prohibited from deducting these from the payments owed to the PSC.

The first phase of STP reporting included high-level data such as Gross, Tax, Allowances, Deductions, Lump Sums and Fringe Benefits. The next phase sees the reports moving away from Payment Summary Annual Rules (PSAR) and Payment Summaries for allowances and deductions to “Income Types.”

For the most part, people use their funds in FSAs and HSAs to reimburse themselves for out-of-pocket costs like copays, health insurance deductibles and the cost of prescription medications. According to the Employee Benefit Research Institute, 48% of workers forfeited an average of $408 of their FSA funds in 2020.

When we started out 2020, any legislative predictions we had for the year, would have been wrong. But as we all know, 2020 has been anything but typical. Any OTC expenses purchased on or after January 1, 2020 are eligible without a prescription. Tele-health services can be covered prior to the deductible and remain HSA-eligible.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content