This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Now that 2021 income tax season has been over for a month and the dust has settled, it is time to start some serious tax planning for 2022. Improve Your Tax Records - If disorganized records were a problem for 2021 taxes due in 2022, set up a better system. In an earlier blog post , I described 12 tax planning topics for 2022.

2021 has been another challenging, exciting, and ever evolving year for the business world. As 2021 comes to an end, here are some year-end tips and compliance guidance to ensure you are ready to kick off 2022 on the right track! Cafeteria Plan and FlexibleSpendingAccount (FSA) Plan Amendments. Happy 2022!

In this post, I continue my discussion of tips from webinars, podcasts, and virtual conferences that I heard during the last quarter of 2021. Reflect on Your Successes - Think back on 2021 and write down a few things that went well for you, despite all the challenges associated with COVID-19. You’ll do well over time.

Top 10 employee benefits for 2021. HR trends forecast the most desired employee benefits for 2021 like financial wellness programs and flexible work arrangements. It’s time for employers to start planning their employee benefits packages for 2021. Top 10 Employee Benefits for 2021. #1 1 Financial Wellness Programs.

A Dependent Care FlexibleSpendingAccount (often shortened to ‘Dependent Care FSA’) is a pre-tax benefit account used to pay for eligible services such as preschool, summer day camp, before/after school programs, and child or adult daycare. 2022 Changes to Dependent Care. Who is Eligible?

Since many areas of the country did not see COVID-related expenses increase until this summer, we will not see a full year’s worth of expenses until well into 2021. So, watch out for mid-year 2021 renewals and beyond. The post Top 5 Health Care Trends for 2021 appeared first on BRI | Benefit Resource.

31, 2021, and for plan years that start on or after Jan. Mid-year election changes — The Consolidated Appropriations Act of 2021 (CAA) and ensuing guidance from the IRS relaxed a number of rules that will come to an end for plans incepting on or after Jan. That comes to an end Dec. That’s a change from the prior threshold of 250.

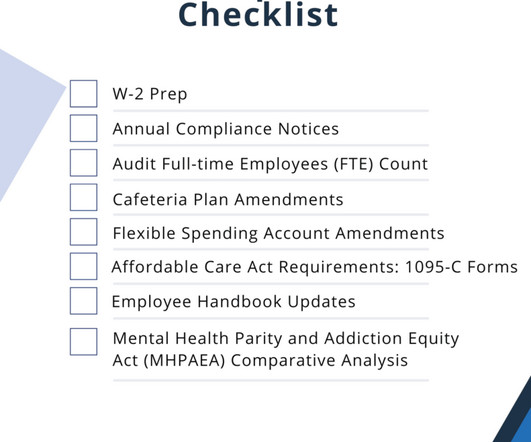

2021 has been another challenging, exciting, and ever evolving year for the business world. As 2021 comes to an end, here are some year-end tips and compliance guidance to ensure you are ready to kick off 2022 on the right track! Check out the 7 tips and download your very own checklist below!

A flexiblespendingaccount (FSA) carryover is one way you can provide flexibility to employees who participate in these accounts. This blog was originally published in August 2021 and most recently updated in August 2023. We break down FSA carryovers below. Can FSA funds carry over to next year?

A flexiblespendingaccount (FSA) allows participants to save money by setting aside pre-tax dollars to pay for eligible medical, dental , vision and dependent care expenses incurred by you, your spouse, or your eligible dependents. We offer a number of tools and resources to help you make the best FSA decisions.

FlexibleSpendingAccounts allow employees to set aside pre-tax dollars from their paycheck to use for medical or dependent care expenses. These funds are placed in an FSA account that employees can use to pay for eligible expenses. Many people are surprised to learn how many everyday items are actually FSA eligible.

The limit for dependent care flexiblespendingaccounts has been stuck at $5,000 since the account’s inception in the 1980s. The American Rescue Plan Act of 2021 has affected both continuation coverage and the limit for dependent care FSAs. But a new bill from Congress passed last week and is changing that.

The IRS released the 2021 limits for Mass Transit, Parking, Medical FSA and Adoption Assistance in Revenue Procedure 2020-45. The limits are effective for plan years that begin on/or after January 1, 2021. There were no changes to limits for the commuter accounts or medical flexiblespendingaccount.

1, 2021, is a holiday. 1 payday back into 2020, you’d still have 27 biweekly pay periods, this time in 2021. Depending on your payday, this will happen next year, when the 27th payday falls on Dec. Why: Paydays occurring on holidays are usually pushed back a day and Jan. Twist: If you don’t push the Jan. Who’s impacted.

FlexibleSpendingAccounts are not eligible for subsidy. The subsidy period begins on April 1, 2021 through September 30, 2021. occurring from April 1, 2021 through September 30, 2021. Model notices were published on April 7, 2021 and are available of the Department of Labor website.

As the end of 2021 and the plan year looms, it’s crucial to consider what you can do with any remaining funds in your FlexibleSpendingAccount (FSA). Most of the funds in your FSA need to be spent before the end of the plan year because you may lose what you don’t spend.

Indeed, a 2021 study found that 29% of Gen Z respondents are carrying medical debt. The various accounts have different rules for what services or medical costs can be reimbursed by these accounts.

Families utilizing Dependent Care FlexibleSpendingAccounts (FSAs) are up against a December 31st deadline. If you have an FSA, there’s a high chance you’ll have to spend down the money in your account so you don’t lose it. Many are in danger of losing their funds.

The IRS’ use-or-lose rule governs flexiblespendingaccounts (FSAs). A flexiblespendingaccount (FSA) is an employer-sponsored benefit that allows employees to set aside a portion of their pre-tax salary to pay for qualified medical expenses or dependent care expenses. So what is the use-or-lose rule?

Internal Revenue Code (Code) Section 125 imposes a maximum dollar limit on employees’ salary reduction contributions to a health flexiblespendingaccount (FSA). Type of Account. Health Savings Account. Health FlexibleSpendingAccount. What plans must be offered with the account?

Almost all health plans offer add-on accounts — health flexiblespendingaccounts, health savings accounts, or health reimbursement accounts. You need to know how these accounts differ so you can communicate about them to employees. Health flexiblespendingaccounts.

If you have a Medical FlexibleSpendingAccount (FSA), you may have the ability to take leftover funds from one plan year and transfer them to the next. Let’s take a look at this example: Let’s say on December 31, 2021, you have $300 left in your Medical FSA. If so, here’s what you need to know: 1.

It’s important not to lose sight of that when developing content and communicating that you offer a health savings account (HSA) , flexiblespendingaccount (FSA) , or any other benefits. That’s what motivates your employees. Some benefits are better understood than others, which might also factor into your approach.

Census Bureau , the number of businesses offering child care services dropped between the years 2020 and 2021, while the cost of child care increased. It is sometimes called a dependent care flexiblespendingaccount, but it differs from typical health FlexibleSpendingAccounts (FSAs) in both purpose and regulation.

Together, these combined announcements by the IRS detail 2022 adjusted limits to the amounts employees can tuck away pretax into FlexibleSpendingAccounts (FSAs), Health Savings Accounts (HSAs), transportation benefits, and retirement plans such as 401(k)s. Adoption Assistance Increases for 2022.

The following commonly offered employee benefits are subject to these limits: High deductible health plans (HDHPs) and health savings accounts (HSAs); Health flexiblespendingaccounts (FSAs); 401(k) plans; and. Transportation fringe benefit plans.

It has been updated to include a new legislative updates from March 2021 and more. ” What you need to know: COVID-19 PPE items such as masks, hand sanitizer, and sanitizing wipes purchased on 1/1/2020 or later are eligible for reimbursement from Medical FlexibleSpendingAccounts and Health Savings Accounts. .”

The new COVID relief package included in the Consolidated Appropriations Act, 2021 (H.R. The COVID relief package extends paid sick and family leave , and your tax credits for providing through March 31, 2021. The leave and the tax credits are extended, not reset, for 2021. The law extends the payback time to the end of 2021.

This reporting is due by December 27 of this year and must include information for the 2020 and 2021 calendar years, regardless of the plan or policy year. Additionally, account-based plans, like health reimbursement arrangements (HRAs) and health care flexiblespendingaccounts (FSAs), are not required to report.

A single card should even be able to correctly pull funds from multiple different pre-tax health accounts (e.g., a Health Savings Account and Limited Purpose FlexibleSpendingAccount). High auto-approval rates. When employees swipe their employee benefits card to pay for an eligible item, they want it to work.

Pre-tax employee benefits plans, such as health savings accounts (HSAs) and flexiblespendingaccounts (FSAs) , let you save money by putting aside pre-tax dollars to pay for eligible medical, dental, vision and other expenses. In 2021, the average employer contribution to employee HSAs was $869.

The 2021 State of Remote Work report by Owl Labs reported that 84% of employees would be happier continuing to work remotely after the pandemic — and some are even willing to take a pay cut to do it! As it turns out, your employees may not be eager to return to the office.

Reporting on Pharmacy Benefits and Drug Costs – Group health plans must report information on plan prescription drug spending to regulators, including plan year dates, number of enrollees, each state where coverage is provided, and most common and costly prescription drugs dispensed by the plan. Likely Effective in 2022.

FSAs (flexiblespendingaccounts) are typically a use-it-or-lose-it benefit. Pre-tax dollars are deducted through payroll and placed into a flexiblespendingaccount to cover eligible medical or dependent care expenses. You may also be eligible to claim refundable tax credits.

As a result, more than 55% of Americans were enrolled in HDHPs in 2021, a new record. Of those, more than seven in ten employers (71 percent) also offer a health savings account with employer funding. An additional tool can be pairing an HSA-HDHP with a Limited FlexibleSpendingAccount (or Limited FSA).

Limits for Health Savings Accounts (HSAs) were released earlier this year. Pre-tax Account Limits for 2022. Health FlexibleSpendingAccount: $2,850 (Up from $2,750 in 2021) Health FSA Rollover: $570 (Up from $550. Health Savings Account Limits for 2022. Up from $270/mo. Family Coverage.

In March 2021, guidance indicated that individual extensions could not exceed 12 months. The “Outbreak Period” will end 60 days after the National Emergency ends. The National Emergency was terminated effective April 10, 2023, placing the Outbreak Period’s end as June 9, 2023.

HSAs have tax documents sent from the custodial banks, and any 121 Benefits migrated employees will receive letters from your prior 2021accounts and letters (and online access) for the custodial bank. A paper statement fee applies (see your HSA account holder agreement). For BRI Customers.

workers who quit in 2021 said that low pay was a reason, and 43 percent said that a lack of good benefits was a reason. According to the 2021 Employer Health Benefits Survey from KFF, 56 percent of firms with three to 49 workers offer health benefits to at least some of their workers. The Benefits of Employee Benefits.

On February 18, 2021, the IRS issued Notice 2021-15, clarifying temporary special rules for cafeteria plans, health flexiblespendingaccounts (“FSAs”), and dependent care assistance programs (“DCAPs”) that were included in the Consolidated Appropriations Act (“CAA”), enacted on December 27, 2020.

We are excited to provide you with some additional insight into the FSA relief options for Health and Dependent Care FlexibleSpendingAccounts, included in the year-end spending bill signed into law on December 27, 2020. Plan sponsors should consider several factors as relief options are being evaluated.

23, 2023, the Departments of Labor, Health and Human Services and the Treasury (Departments) issued FAQs on the prohibition of gag clauses under the transparency provisions of the Consolidated Appropriations Act, 2021 (CAA). 31, 2023 On Feb.

Microsoft offers employees either a Health Savings Account (HSA) or a FlexibleSpendingAccount (FSA). In this article, we will explore a range of innovative employee benefits that can help companies attract and retain the best talent in their industries.

On March 11, 2021, President Biden signed the American Rescue Plan Act of 2021 (the “ARPA”) into law. The individual is a qualifying individual and already enrolled in COBRA coverage on April 1, 2021, or enrolls in COBRA coverage during the “special enrollment period” described below. Subsidized COBRA.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content