This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

On January 15, 2022, the New York City Council enacted Local Law 32 of 2022 (Wage Transparency Law or Law) to amend the New York City Human Rights Law (NYCHRL) to require that most employers include compensation data in their job advertisements. The Law was supposed to take effect on May 15, 2022, however, it […].

The increased penalties generally apply to reporting and disclosure failures if the penalty is assessed after January 15, 2022, and if the violation occurred after […]. The post Inflation and ERISA Penalties: Hand in Hand for 2022 appeared first on EMPLOYEE BENEFITS BLOG.

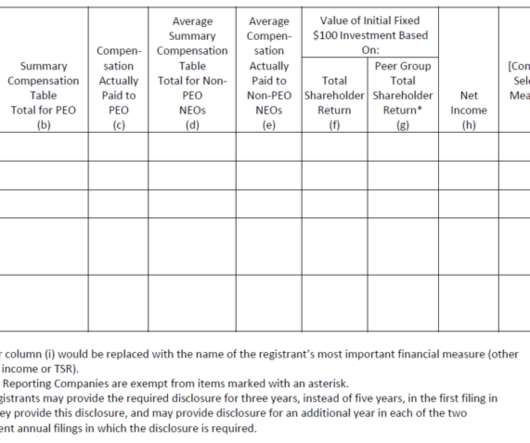

On November 28, 2022, the Securities and Exchange Commission (the “SEC”) published the final clawback rules (the “Final Rules”) under the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”) in the Federal Register.

The post Restrictive Covenants Evolve from Common Law to Statutory Regulation: The 2022 Watershed appeared first on EMPLOYEE BENEFITS BLOG. Unlike state statutes regulating trade secrets (which largely follow the Uniform […].

January 20, 2022. We’ll provide tips for successfully filing 2021 ACA reporting forms (1094-C / 1095-C) and we’ll also cover recent legal and regulatory changes, including certain “transparency” rules taking effect in 2022. 9:00 a.m. – Topic – Employee Benefits Update. Presented by Stacy Barrow. Employee Benefits Attorney.

The SEC’s final rule on Pay Versus Performance becomes effective on October 8, 2022, and will require new executivecompensation disclosures for the upcoming proxy season (for annual proxy statements that include executivecompensation disclosure for fiscal years ending on or after December 16, 2022).

Fast forwarding to the year 2022, will it be a happy new year? Specifically, in its recent Statement of Regulatory and Deregulatory Priorities, released on December 10, the PBGC reported that it expects to publish in January 2022 a final rule on multiemployer pension relief for troubled plans, known as “special financial assistance.”.

On September 26, 2022, the Internal Revenue Service (IRS) extended the amendment deadline for non-governmental qualified retirement plans, plans covered under Section 403(b) of the Internal Revenue Code (Code) and individual retirement accounts (IRAs).

The Securities and Exchange Commission adopted the final clawback rules under Dodd-Frank (the “ Final Rules ”) on October 26, 2022, and we discussed the detailed requirements of the Final Rules and related practical considerations in this earlier blog post.

In September 2022, Deputy Attorney General Lisa Monaco delivered remarks unveiling the Department of Justice’s revised corporate crime guidance to “prioritize and prosecute corporate crime.” To that end, Monaco emphasized that the DOJ will “reward” companies that claw back compensation from executives “when misconduct occurs.”

On May 5, 2022, McDermott Partner Erin Turley delivered a presentation during the 2022 TEA National Conference titled “Understanding a Trustee’s Role in Management Incentive Plans.”

Proxy advisory firms Institutional Shareholder Services (“ISS”) and Glass Lewis (“GL”) each published their annual policy updates for 2023, which updates made certain changes relating to executivecompensation. [1] Value-Adjusted Burn Rates for Equity Plan Evaluations. Please contact a member of the team with questions. . [1]

82830-4-I, 2022 WL 2206828 (Wash. June 21, 2022). Last month, the Washington Court of Appeals affirmed a lower court’s decision to dismiss a challenge to the recently enacted payroll expense tax in Seattle, WA. Seattle Metro. Chamber of Commerce v. City of Seattle, No. The tax, which went into effect on January 1, 2021, […].

ROB PROJANSKY : Hello and welcome to Proskauer Benefits Brief, Legal Insights on Employee Benefits and ExecutiveCompensation. JUSTIN ALEX : First to set the stage, the Special Assistance Program is available to plans that fall into one of four categories: First, plans that are in critical and declining status in 2020, 2021 or 2022.

On August 25, 2022, the US Securities and Exchange Commission (SEC) adopted final rules to implement the pay versus performance disclosure requirement mandated by the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act).

On August 25, 2022, the US Securities and Exchange Commission (SEC) adopted final rules imposing new mandatory “pay for performance” disclosures for most public companies (foreign private issuers, emerging growth companies and registered investment companies are excluded).

Effective January 1, 2023, Washington employers must comply with SB 5761, commonly known as Washington’s Pay Transparency Law, signed by Governor Jay Inslee on March 30, 2022. The post Washington State’s Pay Transparency Law Takes Effect January 1, 2023 appeared first on EMPLOYEE BENEFITS BLOG.

We recently reported on an FAQ issued December 23, 2022 (FAQ About Affordable Care Act and Consolidated Appropriations Act, 2021 Implementation Part 56) by the US Departments of Labor, Health and Human Services and the Treasury (collectively, the Departments).

In late 2021 and early 2022, companies implemented pay raises across the board, even for those below the executive and management levels. This amounted to more than $1.2 million a year in USD. Other organizations, such as the E conomic Policy Institute , have discovered that this disparity has grown since the 1970s.

In other words, companies should not grant spring-loaded awards under any mistaken belief that they do not have to reflect any of the additional value conveyed to the recipients from the anticipated announcement of material information when recognizing compensation cost for the awards.”

Act of 2022 (“ SECURE 2.0 ”) that was signed into law on December 29, 2022 as part of the 2023 Consolidated Appropriations Act includes a slew of changes for retirement plan sponsors and employers. please see our other blog posts or contact a member of Proskauer’s Employee Benefits and ExecutiveCompensation group.

If you have any additional questions regarding the impact of Notice 2023-62 on your retirement plans, please reach out to a member of Stinson’s employee benefits and executivecompensation practice group. As signed into law, Section 603 of the SECURE 2.0

Twelve years after the enactment of the Dodd-Frank Wall Street Reform and Consumer Protection Act, and many years after the Securities and Exchange Commission started considering regulations implementing the clawback provisions of Dodd-Frank, the SEC published the Final “Clawback” Rules (the “Final Rules”) on October 26, 2022.

As described in Part 4 of our 2022 end of year plan sponsor “to do” list , on October 26, 2022, the Securities and Exchange Commission published the final clawback rules under the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”).

For ISO exercises and ESPP transfers occurring in 2022, the Section 6039 employee information statement requirement is satisfied by providing Form 3921 (for ISOs) and Form 3922 (for ESPPs) to employees no later than January 31, 2023.

As reported in Part 4 of our 2022 End of Year Plan Sponsor “To Do” List , Section 6039 of the Internal Revenue Code (the “Code”) requires employers to provide a written information statement to each employee or former employee and file information returns with the IRS regarding: (1) the transfer of stock pursuant to the exercise of an Incentive Stock (..)

For ISO exercises and ESPP transfers occurring in 2022, the Section 6039 employee information statement requirement is satisfied by providing Form 3921 (for ISOs) and Form 3922 (for ESPPs) to employees no later than January 31, 2023.

For a calendar fiscal year employer that sponsors an annual incentive program which provides that an employee will vest in any amounts earned if the employee is employed as of the last day of the calendar year, annual incentive payments earned in 2021 must be paid on or prior to March 15, 2022 to qualify as short-term deferral payments.

Consider the following: An Intelligize search completed in May 2022 for publicly filed proxy statements that contain “self-assessment” or “self-evaluation” within three words of “CEO” returns 623 results. The proxy disclosure of the CEO self-assessment process varies, depending on the issuer.

An HCI is generally defined as the lesser of (1) highest paid 1% of the employee population or (2) 250 highest paid employees (compensation must be in excess of the IRS Highly Compensated Employee compensation limit, which is $135,000 for 2022). When is a Payment Contingent on a Change in Control?

Over 4500 companies globally have become certified B Corps as of February 2022. (To Innovation broadly impacts a board's fundamental responsibilities, including long-term planning, corporate strategy, people and culture, executivecompensation, investments, and acquisitions.

Having the best compensation plan will help you avoid the risk of losing them or scaring away potential hires. In addition, you need the best employee benefits software in 2022 to help you plan your compensation effectively. . Our List of Top Employee Benefits Administration Software 2022. Holland and Knight.

First, for plan years beginning in 2022, the amortization period for underfunded plans is extended to 15 years, rather than seven as previous allowed. Plan sponsors may elect to defer the changes until 2022. Single Employer Pension Plan Provisions. The ARPA contains two funding relief items that benefit single employer pension plans.

Listen to the podcast Tanusha Yarlagadda: Hello and welcome to The Proskauer Benefits Brief: Legal Insights on Employee Benefits and ExecutiveCompensation. That concludes our discussion of the DOL’s 2022 final ESG rules. We will keep you posted on any new developments in this regard.

As foreshadowed by the FTC’s issuance of a Policy Statement in November 2022 outlining new principles to expand its enforcement authority under Section 5 of the FTC Act, the Proposed Rule now invokes that authority to find non-competition clauses to be an “unfair method of competition” under Section 5. Key Takeaways. EPA , 142 S.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content