This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Now that 2021 income tax season has been over for a month and the dust has settled, it is time to start some serious tax planning for 2022. Planning now provides seven months to take action and/or implement changes to avoid a stressful “tax scramble” at the end of the year. 401(k), 403(b), and traditional IRA).

Many older adults also have multiple income sources including Social Security, a pension, full-or part-time work or self-employment, withdrawals from retirement savings (including taxable required minimum distributions or RMDs), and interest, dividends, and capital gains on investments. In other instances (e.g.,

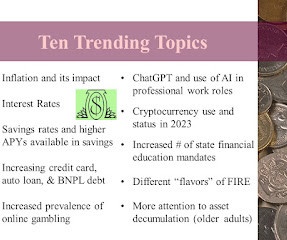

Below are seven information tidbits that caught my eye: Defensive Investing- Financial markets were volatile in 2022 and, for a while, “there was no (good) place to hide.” Tax Planning - Until 12/31/25, taxes are “on sale.” There are only two ways to reduce taxes: 1. When the government lowers tax rates.

If you picture retirement planning and taxes as a Venn Diagram, there is lots of overlap between these two areas of personal finance. This is true both during one’s working years (when taxpayers are saving for retirement) and later, when people are older and withdrawing taxable income from tax-deferred accounts.

One of the niche audiences for my business, Money Talk , is older adults grappling with financial issues such as creation of a retirement “paycheck,” paying taxes on required minimum distributions (RMDs), and simplifying financial accounts. Tax-free accounts (e.g., Tax-free accounts (e.g., Tax-deferred accounts (e.g.,

As we close out 2021 and get ready to welcome 2022, it is a good time to consider the impact of indexes (a.k.a., In 2022, beneficiaries will receive a 5.9% Pension COLAs - Pension benefits for some retirees are also indexed for inflation. a $59 increase for every $1,000 of benefits) in 2022.

Many are middle income taxpayers who diligently saved and invested for 4-5 decades in tax-advantaged plans. As I wrote in my book Flipping a Switch , some older adults must “plan for higher taxes in the future, especially when required minimum distributions (RMDs) kick in.” IRMAA surcharges. to $573.30 for Medicare Part B and $12.40

The year 2022 was chock full of news about inflation, with a year-to year Consumer Price Index increase of 9.1% This includes Social Security recipients, retirees with COLA-adjusted pensions, and workers with COLAs stipulated in their job or union contracts. When bracket incomes rise, people may be taxed at lower tax rates.

What is a group personal pension (GPP)? A group personal pension is a defined contribution (DC) arrangement whereby an employer agrees to make monthly contributions into a scheme, but the contract is between the employer and the pension provider. The rest will be taxed. What are the tax issues?

Inflation-induced price hikes on goods and services are like a regressive sales tax and hurt those with low incomes the most. Interest Rates- Between March 2022 and May 2023, the Federal Reserve raised interest rates 10 times in an effort to decrease inflation by slowly increasing the cost of borrowing.

The year 2022 is equally noteworthy for a “Great Unretirement” as millions of older workers who left jobs during the pandemic decided to come back into the labor force. 67 for workers born in 1960 or later), Social Security deducts $1 from benefits for every $2 earned above the annual limit ($19,560 in 2022).

One of the most daunting financial aspects of retirement, especially for people who have been diligent savers throughout their working years, is taking required minimum distributions (RMDs) from their tax-deferred retirement savings accounts beginning at age 72. New RMD tables went into effect in 2022, so this is a good time to discuss RMDs.

Need to know: Employers can tailor content and communication channels to different employee groups to help with their pensions knowledge. Losing the jargon will make the language of pensions easier to understand and more relevant to staff. They could invest in financial coaching for a more personal approach to pensions education.

For example, workers with a guaranteed pension and/or a high investment risk tolerance might want to have more stock exposure in a TDF and would chose a target date farther off in the future. Make Tax-Advantaged Gifts - Consider “bunching” charitable donations with other tax deductions (e.g.,

In what may bring a sigh of relief, 2022 is not a year with new legal requirements incumbent on employers regarding pensions. But there are many ongoing requirements to be mindful of, and changes within the pensions environment that could lead to future impacts. Then there is the issue of tax relief for low earners.

lost pension pots in the UK, worth around £26.6 billion WEALTH at work explains how employees can track down lost pensions and provides guidance on whether to consolidate The total value of lost pension pots has grown from £19.4 billion in 2022. find-pension-contact-details). find-pension-contact-details).

Retirement plan sponsors need to utilize updated Form W-4P (for periodic pension and annuity payments) and new Form W-4R (for nonperiodic payments and eligible rollover distributions) for income tax withholding elections beginning January 1, 2023.

lawn care, tax preparer, hair dresser), natural gas for home heating, electricity, and auto and homeowners insurance. January 2022 to January 2023) so there is no need for seasonal adjustments. pensions, Social Security, annuities) can “ride it out.” 5+ for 12 eggs!), services (e.g.,

of Americans age 65+ were working in 2022. Tax on Social Security Benefits - Those who work and claim benefits will trigger taxes with a combined income above $25,000 (individuals) or $32,000 (married couples filing jointly). Continued FICA Tax - Like all workers, employed older adults must pay Social Security/ Medicare tax.

Spring Budget 2023: Chancellor of the Exchequer Jeremy Hunt announced in his Budget statement today (15 March 2023) that government will abolish the lifetime allowance for pensions. Jeremy Hunt’s decision to raise the tax free pension allowance will help retain older staff who want work to pay.”

As of December 2022, the UK Inflation rate stood at 10.5% Therefore, people’s pension savings will likely start catching up with the frozen Allowance. This could particularly affect those who never check the value of their pension or haven’t done so for some time. and therefore exceed the current LTA.

The FCA announced that more over 55s are accessing their pensions, and over half are cashing out their pension pots completely. Jonathan Watts-Lay, Director, WEALTH at work – a leading financial wellbeing and retirement specialist comments; “It’s concerning that so many pensions are being cashed out in full.

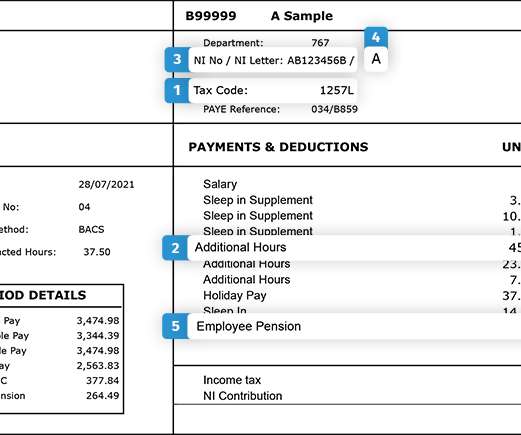

It’s worth remembering that it’s an employee’s responsibility to check they’re on the right tax code, as it impacts how much tax they pay – whether it’s too much tax or too little. For the 2021/22 tax year (and through to 2025/26), the tax code for most people under 65 who only have one job or pension is 1257L.

The BP Pensioner Group has begun legal action against senior members of BP management and directors of the BP pension fund trustee due to concerns around the value of 2,500 members’ pensions. According to the BP Pensioner Group, the dispute is about decisions made by BP and the pension fund trustee in 2022 and 2023.

Whilst more than one in ten (13%) have either stopped or reduced the amount they pay into their pension due to rising costs, worryingly, almost three in ten (29%), admit they may consider stopping payments in the future, and a third (30%) may consider reducing future payments. Whilst this is understandable, it really should be a last resort.

Yet, many businesses might be inadvertently losing money because they lack a competitive pension package. Consider this: A 2022 survey conducted by tech giant Lattice, which included 200 HR professionals and 2,000 UK-based workers, revealed that 14% switched jobs due to superior benefits. Think this isn’t a big deal?

Autumn budget 2022: The government has confirmed that the pensions triple lock and credit will be protected, and rise by 10.1% He reported that increase should result in up to £1,470 extra for a couple and £960 for a single pensioner. The single tier state pension will rise from £9,627.80 in April 2023.

Pension and group risk Trust-based defined contribution pension with 12% employer, 3% employee minimum contributions. Employer-paid, but employee can fund up to 10% if it means added affordability, for example a tax efficient electric vehicle. Additional voluntary contributions. Life assurance at 10-times salary.

Most of us spend the majority of our working life saving into our pension. However, all this hard work saving can quickly unravel for those who aren’t aware of common pension mistakes. WEALTH at work outlines below the top 10 pension mistakes individuals could make, to highlight what employees facing retirement may need support with.

At Ashurst, we closely consider the pension and benefits we offer and focus particularly on how we engage our people in these offerings to ensure they are of maximum benefit. Because pension forms part of an employee’s finances, tackling the broader topic of finances also increases engagement with pensions.

Whilst a workplace pension provides a savings vehicle for retirement, many organisations want to put in place a tax efficient savings option for those looking to save in general and build financial resilience. This will provide employees with a convenient, flexible and tax efficient way to invest.

However, French residents pay for these benefits through a substantial amount of taxes. Those who wish to work and reside in France have a variety of taxes to be paid, here is a closer look at the French tax system. Types of Taxes. Primarily there are three types of taxes in France. Income Tax. Income Tax.

Employers with five or more workers – The deadline for registration is June 30, 2022. Qualified retirement plans include: Qualified pension plans. Simplified Employee Pension (SEP) plans. Employers with 50 or more workers – The deadline for registration was June 30, 2021. 401(k) plans. 403(a) plans. 403(b) plans.

With the current tax year ending on 5 April 2022, the 2022/2023 tax year introduces many key pieces of legislation affecting millions of employers and employees across the UK. In preparation for the upcoming tax year end, we’ve prepared an extensive list of all the regulatory changes that you need to be aware of.

It is important that employees understand the importance of saving into their pension from early on. For example, they may not realise that someone in their 20s can increase their pension pot by 25% in retirement by saving an extra 1% a year with an employer match. Don’t neglect your pension.

She was employed by Maximus UK Services, which performs medical assessments on people claiming state benefits for the Department for Work and Pensions, and managed an administrative team of nine. In April 2022, insurers Legal and General, which had protected Henderson’s income, cut her sick pay.

Read on to learn how they supported CIPHR Payroll customers – including seven new clients who have just joined the CIPHR family – as well as a quick summary of the legislative changes that have taken effect for the 2022/23 tax year. Recap of changes for the 2022/23 tax year. Pensions and pension allowances.

According to Wagestream’s The state of financial wellbeing: the cost of living report 2022 , published in July 2022, there has been an upswing in organisations adjusting their benefits budget to support broader financial wellbeing programmes as an additional way of helping their workforce, rising from 51% in 2021 to 93% in 2022.

As the UK government warns that the state pension age might need to rise, a new report from the the International Longevity Centre UK (ILC) claims that, between 2019 and 2022, people’s work span in the UK fell by 6 months.

Most notably, the program has been expanded to include section 403(b) tax-sheltered annuity plans (“403(b) plans”). 2022-40 also includes caveats regarding limitations on the scope of IRS review and the purposes for which a plan sponsor may rely on the determination letter, which are similar to those that apply to 401(a) plans.

2022 was a year of much change, with the cost-of-living crisis raging on and many employers stepping in to help their lowest-paid workers with one-off payments and pay rises. Events impacting pay, financial wellbeing and pensions. Reward and benefits changes. Of those that are considering change, 79% will be enhancing benefits.

On June 3rd of 2022, the Department of Labor announced that it is developing a new proposed rule on determining employee or independent contractor status under the FLSA. They are also typically responsible for the payroll taxes that the employer would typically pay including the employer’s share of Medicare taxes and Social Security taxes.

Recently, the pressures on household income has raised concerns that members will look at their pension contributions as a way of cutting back on their monthly costs. However, new research from the Pensions Management Institute[2] (PMI) has suggested that this may now be changing. 7% have already ceased their contributions.

Reward and benefits can be used to demonstrate an organisation’s values, with examples including environmental, social and governance (ESG) default funds on pensions and electric car schemes. Not everyone wants to save into a pension so offer an ISA too.”. Offer alternatives,” she adds.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content