This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Below are the top 10 employee benefits certifications for professionals in 2024. Certified 401(k) Professional (C(k)P®) The Certified 401(k) Professional (C(k)P®) credential, offered by The Retirement Advisor University in collaboration with UCLA Anderson School of Management, focuses on the complexities of managing 401(k) plans.

International Foundation of Employee Benefit Plans

DECEMBER 12, 2024

Many 401(k) plans allow participants to take out loans from their individual 401(k) account. According to Employee Benefits Survey: 2024 Results, 81% of corporate employer plans offered a 401(k) loan provision.

The Internal Revenue Service is making some changes to how much you can contribute to your 401(k) plans. As per the IRS, 401(k) limits for 2025 have been increased to an annual amount of $23,500, up from $23,000. Will the 401(k) Cap Increase Be Enough to Help Employees Save for Retirement?

International Foundation of Employee Benefit Plans

SEPTEMBER 4, 2024

Many 401(k) plans allow participants to take out loans from their individual 401(k) account. According to Employee Benefits Survey: 2024 Survey Report, 81% of corporate employer plans offered a 401(k) loan provision.

Hobby Lobby’s 2024 pay hike went into effect on October 1, 2024, so employees who apply to the company now should be able to benefit from the change. The arts and crafts supply store recently announced that it has increased the starting wages for its employees again, making this the thirteenth increment since 2009. Data from the U.S.

All other tax-deferred plans, like 401(k)s and the thrift savings plan (TSP), must have RMDs calculated separately. 2022 for 2024) and can be avoided by lowering adjusted gross income or making an appeal to Medicare based on life events. IRMAA is based on income earned two years earlier (e.g.,

About 7 in 10 US employees say they’re stressed about money, per PNC’s 2024 Financial Wellness in the Workplace report. Some employees have resorted to borrowing from their 401(k) to help make ends meet. However, not all employees face the same financial woes. Engaging a multi-generational workforce can be difficult.

The changes, which the IRS releases in November each year, will affect contribution limits for HSAs, FSAs and 401(k) and other retirement accounts. Funds in an HSA can be rolled over indefinitely year after year and invested, much like a 401(k) plan. The catch: These funds must be spent by March 15, 2024.

Act of 2022 (“SECURE 2.0”), the IRS issued Notice 2024-02 , which addresses SECURE 2.0 Although Notice 2024-02 offers helpful guidance for employers and plan administrators, it does not include hotly anticipated guidance on SECURE 2.0 401(k) Plan : A spin-off plan from a pre-SECURE 2.0 Merger of Pre-SECURE 2.0

A California district court recently denied a motion to dismiss claims that the fiduciaries of a 401(k) plan breached their ERISA fiduciary duties of prudence and loyalty by selecting underperforming, high-cost investments and causing the plan to pay excessive fees for services. The case is Coppel v. Seaworld , No. 21-cv-1430 (S.D.

The day after Thanksgiving, while many of us were fortunate enough to be reaching for leftover pie, the IRS released proposed regulations implementing the requirement that 401(k) plan sponsors permit “long-term part-time employees” to make elective contributions to a 401(k) plan. How did we get here?

With the 2023 tax filing deadline in the rear view mirror, now is a good time to look ahead to 2024 taxes that you will owe in April 2025. This post extends that discussion with a description of seven key steps to take to plan for your 2024 tax return due in 2025. 401(k) plan).

The 2023 income tax filing deadline is only days away (April 15, 2024 in most of the U.S.). Baby Boomer Challenges - Baby boomers (born 1946-1964) were the first generation with the ability to save money for retirement in 403(b)s, 401(k)s, and IRAs for decades (their parent’s generation had pensions). There is no way out.

This rule takes effect in 2024 and Roth IRA income limits do not apply. The limit will be the greater of $10,000 or 150% of the standard catch-up amount for 401(k)s and similar salary reduction plans. Employer Retirement Plans - A “starter 401(k)” plan for employers with no current retirement plan will take effect in 2024.

Workplace Roth Accounts - Effective January 1, 2024, no required minimum distributions (RMDs) are required from workplace Roth accounts (e.g., 401(k), 403(b), 457b, and TSP). With a debt snowball, you list debts by outstanding balance and pay extra on smallest balances first.

While HSAs combine several of the best features of 401(k)s and flexible spending accounts (FSAs), they are often overlooked and underutilized. The post WEX celebrates HSA Day 2024 with resources for HR leaders, employees appeared first on WEX Inc. It is not legal, tax, or investment advice.

401(k)s, 403(b)s, and traditional IRAs). For example, if a couple owes $25,000 on a $150,000 taxable joint income, their effective tax rate is $25,000 ÷ $150,000 = 16.7%, even though their 2023 and 2024 marginal tax bracket is 22%. It is calculated by dividing the total amount owed on a tax return by total taxable income.

employer-sponsored 401(k) plans. Act seeks to: Open access to 401(k) retirement plans to more people Provide greater opportunities to save Offer financial incentives to save while removing common barriers and penalties So, what does the law require of employers? The SECURE 2.0 The SECURE 2.0 The SECURE 2.0 The SECURE 2.0

However, with the new rule effective for 401(k) plans beginning January 1, 2024, the guidance leaves employers and plan sponsors very little time to make changes to […] The post Last-Minute Guidance Leaves Little Time for Long-Term, Part-Time Employee Changes appeared first on EMPLOYEE BENEFITS BLOG.

401(k) matching), stock options, or performance bonuses. A 2024 Deloitte study found companies with robust benefits packages saw 25% lower attrition rates. In an era of rising healthcare costs, these benefits are non-negotiable for many workers. Financial Incentives Beyond salaries, employers might offer retirement plans (e.g.,

As 2024 comes to a close, HR professionals are rethinking benefits strategy going into next year. In SHRMs 2024 Employee Benefit Survey, menopause benefits, gender-affirming care and lifestyle savings accounts are becoming benefits trends for the first time. All of these factors mean that employee needs are changing.

In this all-encompassing guide, we look at the best available options concerning Employee Benefits Options in 2024, different types, and significance, along with best practices in designing a benefits package to suit the workforce's needs. FAQ’s What are the main types of employee benefits for 2024?

401(k), 403(b), 457, TSP). 2022, 2023, 2024, and 2025). Pay particular attention if your projected income is close to a “breakpoint” for the next highest tax bracket so you can take proactive steps to stay below that number. Sometimes, saving just 1% more of pay can make a big difference on taxes due.

The Department of Labor’s new fiduciary rule, which mainly applies to 401(k) plans, will also affect employers who offer their staff health savings accounts. The new rule, which takes effect September 2024, bars employers from providing advice to their workers on how they should invest the funds in the HSA they offer.

However, many employees feel their current benefits don’t meet their day-to-day needs, according to a 2024 Wellbeing and Voluntary Benefits Survey from HR consulting Firm Buck. It aims to create a healthier, more engaged workforce by addressing employees’ evolving needs in a way that reflects company values and mission.

Historically, the Code restricted 403(b) plans more than 401(k) plans in terms of the contributions and earnings available for hardship withdrawal. These changes are effective for plan years beginning after December 31, 2024. Before SECURE 2.0, Eligibility of Long-Term Part-Timers SECURE 1.0 However, SECURE 2.0

The saga of 401(k) catch-up contributions under SECURE 2.0 For employees who contribute to more than one 401(k) plan during a year—an old employer’s plan and a new employer’s plan, for example—contributions into each plan would be treated separately for purposes of determining whether the $145,000 threshold has been reached.

On August 19, 2024, the Internal Revenue Service issued Notice 2024-63 (the Notice), providing guidance regarding the implementation of Section 110 of the SECURE 2.0 Act of 2022, which permits employers with a 401(k) plan or 403(b) plan to provide matching contributions to employees based on employee student loan payments.

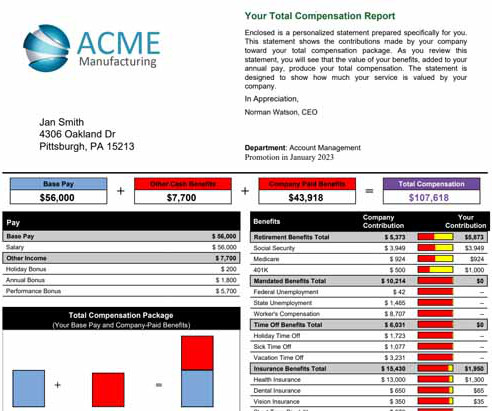

Sample Total Compensation Report Statement Employee Name: John Smith Date: October 10, 2024 Compensation Summary Base Salary: $60,000 annually Benefits: Health Insurance (Employer Contribution): $7,200 annually Dental and Vision Insurance: $1,200 annually Paid Time Off: 20 days vacation, 5 sick days, 10 federal holidays (estimated value: $10,000 annually) (..)

The Internal Revenue Service recently announced the cost-of-living adjustments to the applicable dollar limits for various employer-sponsored retirement and welfare plans for 2024. Most of the dollar limits that are subject to adjustment for cost-of-living increases will increase for 2024.

Read it here Financial Stress in 2024: Its Real You dont have to look far to find a financial guru counseling calm about the 2024 economy. For example, you might share short explanatory videos designed to unravel the complexities around your companys savings benefits, such as your 401(k) plan or HSA offering.

But with inflation at or near 40-year highs, those changes are especially relevant for 2024. The Internal Revenue Service, or IRS, regularly makes changes to adjust its regulations in response to inflation.

On November 1st, the IRS released a number of inflation adjustments for 2024, including to certain limits for qualified retirement plans. As expected, this year’s adjustments are more modest than last year’s significant increases. The table below provides an overview of the key adjustments for qualified retirement plans.

Employers, many of whom are in the midst of or have already completed open enrollment for […] The post IRS Announces 2024 Employee Benefit Plan Limits appeared first on EMPLOYEE BENEFITS BLOG.

A Sample Total Compensation Statement Here is a sample TCS that illustrates how this information can be presented: Employee Name: John Doe Job Title: Software Engineer Date: January 1, 2024 Direct Pay Base Salary: $85,000 per year Indirect Pay Health Insurance: $7,000 annual premium (employer-paid) Retirement Plan: 401(k) match of 3% of salary Paid (..)

For 2024, the limits are $4,150 for single coverage and $8,300 for family coverage.) One of the key features of these plans is that the funds in them can be carried over from year to year and can be invested like a 401(k) plan. Withdrawals to reimburse for these expenses are also not taxed.

In it, she breaks down all the new payroll compliance changes affecting payroll administration in 2024, including post-pandemic trends that don’t appear to be going anywhere anytime soon. Without further ado, here’s step-by-step guidance for achieving payroll compliance in 2024. not signing up for your 401(k) plan).

On November 1, 2023, the Internal Revenue Service (IRS) released Notice 2023-75 , which sets forth the 2024 cost-of-living adjustments affecting dollar limits on benefits and contributions for qualified retirement plans. The following chart summarizes the 2024 limits for benefit plans. The 2023 limits are provided for reference.

That means you need to be acutely aware of changes, such as new annual limits on contributions and required coverage in 2024. For plan years beginning in 2024, the minimum annual deductible is $1,600 for self-only coverage and $3,200 for family coverage. It’s a lot and you need to make sure other departments are in the know.

HSA funds can be invested in mutual funds as you would with a 401(k), which lets employees grow their dollars. In an HSA, in 2024, a single has a limit of $4,150 and family $8,300. Employees must be enrolled in an HSA-eligible health plan (or high-deductible health plan ) to be eligible for an HSA. Investment potential.

Last month, the Internal Revenue Service (IRS) released long-awaited guidance on matching contributions for qualified student loan payments under § 401(k) of the Internal Revenue Code and other similar retirement plans.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content