This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Tax Planning - Until 12/31/25, taxes are “on sale.” Nobody has a crystal ball, but we know that tax rates will rise starting in 2026 when the Tax Cuts and Jobs Act expires. There are only two ways to reduce taxes: 1. When the government lowers tax rates. Make less income and 2.

Common challenges that affect many widows/widowers are aloneness, a lower income, increased taxes/higher tax rate filing as an individual vs. a couple, loss of services that a deceased spouse used to perform, and no longer spending time with couples. placing savings in taxable, tax-free, and tax-deferred accounts).

Therefore, people’s pension savings will likely start catching up with the frozen Allowance. This could particularly affect those who never check the value of their pension or haven’t done so for some time. Positive pension fund growth as well as a pay rise may easily push them over the LTA before they know it.

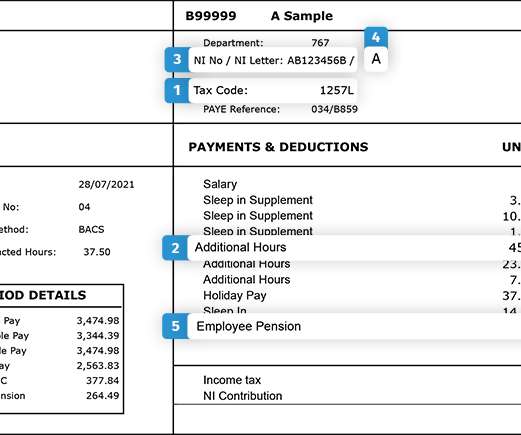

It’s worth remembering that it’s an employee’s responsibility to check they’re on the right tax code, as it impacts how much tax they pay – whether it’s too much tax or too little. For the 2021/22 tax year (and through to 2025/26), the tax code for most people under 65 who only have one job or pension is 1257L.

As announced in April’s Budget, the Lifetime Allowance (LTA) will be frozen at its current level of £1,073,100 until April 2026. million pension savers [1] are set to reach the limit and will be hit with a tax charge of 55% in retirement. Assumes growth rate of 5% and excludes charges on the pension plans.

Tax deduction – For HR or management, here’s a quick tax tip; it also counts as a tax deduction, thus decreasing your tax liability for the year. by 2026, a significant rise that shows the demand for this gift option. In the UK, the gift voucher market is projected to grow by 10.3%

Events impacting pay, financial wellbeing and pensions. In terms of pensions, employers will be looking at how to position them to staff without a disposable income and how they can use their budget to support staff with retirement benefits if they cannot put it towards pay.”. The cost-of-living payments that we’ve seen will continue.

With the current tax year ending on 5 April 2022, the 2022/2023 tax year introduces many key pieces of legislation affecting millions of employers and employees across the UK. In preparation for the upcoming tax year end, we’ve prepared an extensive list of all the regulatory changes that you need to be aware of. Payroll news.

The GNI measure was introduced by the Irish Government to adjust for the inflated GDP figure caused by Ireland’s position as a tax haven for mainly US corporations.) Ireland’s adjusted per capita GDP figure known as Gross National Income is around 16 percent higher than the UK’s and higher than that of both Germany and France.

The plans are protected by federal insurance provided through the Pension Benefit Guaranty Corporation or PBGC. - The PBGC ensures traditional pension plans to ensure that some benefits are paid even if employers go bankrupt. However, the contributions are invested on the employee's behalf on their account.

Replaces the saver’s tax credit with the “saver’s match,” which is a federal matching contribution deposited in the retirement plan account for qualifying employees (based on modified adjusted gross income); the match is 50% of qualifying contributions up to $2,000 ( effective for tax years beginning after December 31, 2026 ).

The ARPA also allows the employer, insurer, or multiemployer plan sponsor who subsided the premiums to offset the cost by claiming a new federal tax credit. The subsidy is tax-free to the individual receiving the subsidy. Tax Credit. Single Employer Pension Plan Provisions. Individuals Eligible to Receive Subsidy.

The new law eliminates what was labeled the "Windfall Elimination Provision and the Government Pension Offset." They earned pensions on their public jobs, and the Social Security they paid was generally in those concurrent "private-sector jobs." That prediction is a reality in 2025 or 2026. The problem is scarcity.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content