This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Personal finances can get complex for many older adults with multiple streams of income, the need to create a retirement “paycheck,” Social Security benefits, required minimum distributions, and more. Increased Standard Deduction - Taxpayers age 65+ (and those who are blind) get an increased standard deduction on federal income taxes.

Since there is no longer a non-itemizer’s charitable deduction in 2022 and only about 10% of tax filers itemize, you’ll probably have fewer receipts to save. 401(k), 403(b), and traditional IRA). . ¨ Improve Your Tax Records - If disorganized records were a problem for 2021 taxes due in 2022, set up a better system.

401(k)s) and IRAs are pegged to inflation. Standard Deduction - The amount of income taxpayers can shelter from income taxes rises with inflation (e.g., for couples filing jointly, the standard deduction is $27,700 in 2023 vs. $25,900 in 2022). When inflation rises, workers can save more money. million in 2022).

One of the few things that taxpayers can do to reduce their income taxes after a calendar year ends is to make a tax-deductible contribution to a traditional individual retirement account (IRA) or a SEP-IRA (for small business owners and/or their employees). 401(k), 403(b), 457, or Thrift Savings Plan). There is no way out.

saving 10% of pay in a 401(k) plan). Payroll deductions for defined contribution plans, like 401(k)s, make adhering to advice to “pay your first” automatic. A good rule to follow to build financial knowledge is to learn one new thing every day about personal finance (e.g., budgeting).

A letter from the Social Security Administration (SSA) notifies beneficiaries of their expected benefit, including IRMAA deductions, if any. Three IRMAA Action Steps ¨ Reduce MAGI- MAGI is based on adjusted gross income (AGI) plus tax-exempt interest income and certain deductions that are added back. IRMAA seems very punitive.

I recently attended a NY Public Library webinar about tax planning and below is a summary: Standard Deduction - 2023 saw the largest ever automatic adjustment to standard deductions since indexing was introduced in the 1980s. A larger standard deduction means that taxpayers can shelter more income from income taxes.

401(k) and 403(b) plans) because contributions are deducted automatically from workers’ paychecks and employers may match them, in which case, it is smart to save enough to earn the maximum employer match. Regular investing over 3-4 decades of work is essential to close future income gaps.

Other tax numbers that get indexed are the standard deduction, certain tax credits, and the deduction for business-related and medical mileage. In 2022, retirement savers in 401(k)/403(b)/457 plans and the federal Thrift Savings Plan (TSP) who are under age 50 can contribute up to $20,500, a $1,000 increase from $19,500 in 2021.

Below are ten suggestions to improve your finances during the year ahead: 1. The easiest way to “pay yourself first” is to have savings deducted automatically from your paycheck through a 401(k) or other workplace savings plan. Another new year is underway, which provides an incentive to get “your financial act together.”

Here are 12 tax topics to consider: Itemized Deductions- Only about 10% of taxpayers can itemize since the Tax Cuts and Jobs Act went into effect in 2018. Strategies to garner a tax benefit for charitable gifts to qualified charities include “bunching” deductions into one tax year and setting up and funding a donor advised fund.

Either way, you’ll need to master the basics of business finance if you want to find success. Even employees not working directly in finance generally need a basic understanding of it to succeed. Nothing exists in a bubble, and business finance is no different. Why is that?

Last year, I wrote a blog post about mid-year financial check-up s for the OneOp Personal Finance team. In it, I urged a review of tax deductions/credits, tax withholding, budgeting/cash flow, flexible spending accounts, financial goal progress, and investment portfolio status. 401(k) or 403(b) plan).

Dollar-cost averaging works best if investment deposits are “automated,” such as authorizing 401(k) plan payroll deductions or automatically debiting a bank account monthly for mutual fund share purchases. For example, $100 in a mutual fund or 5% of pay every payday in an employer retirement savings plan.

With a dedicated financial wellness program, you can help employees manage their finances reducing stress and improving productivity. This added stress can drastically affect an employees finances, especially if they do not have an adequate amount saved and now, companies are providing solutions.

401(k) plan). Do Strategic Tax Planning- Explore tax planning strategies that may apply to your situation, such as bunching deductions, contributing to a Health Savings Account (HSA), Roth IRA conversions, or utilizing tax-loss harvesting to offset capital gains. As a result, there will be an increase in tax rates (e.g.,

What employees are saying about finances and retirement? A variety of recent studies have indicated that: Nearly twice as many employees said they were stressed about their finances than said they were stressed about their jobs. What employers are saying about employee finances and retirement?

Keep in mind that the ritual of choosing a benefits package is a brand-new experience for people who are new to the workforce, and you should prepare to educate new employees on how to effectively choose and use their new coverages, as well as all the details like premiums, deductibles and out-of-pocket expenses. Financial wellness.

It is safe to say that COVID-19 impacted the finances of every American in one or more ways. Replenish Retirement Accounts - Consult with your employer HR department or plan custodian about steps to repay what you borrowed from a tax-deferred employer retirement savings plan such as a 401(k) or 403(b) plan.

When an employee is worried, unproductive and can’t afford to participate in group activities and outings because of finances, it not only affects the person but the team as a whole. Oftentimes, people will pay more monthly for car insurance so they can get a low deductible, usually $500. Make a 401(k) plan available to them.

Hourly-paid nonexempts are impacted only to the extent of withholding and deductions. So you must plan in advance, getting all the appropriate departments—HR, Accounting, Finance, IT and the C-suite—on board. Employees’ benefits deductions and allowances (e.g., In addition, 401(k) nondiscrimination testing may be affected.

While it’s not really your job to make sure your employees are saving for retirement, having a 401(k) plan among other benefits can help you both. Giving birth to a 401(k) is like giving birth to a baby. Just a 401(k) plan as a benefit is a good thing. A 401(k) matching program is a budget item.

With everyone under unique and often financial strains, many are examining their finances, searching for ways to save money. Examining and taking control of finances is one way people are coping. Make sure employees understand the tax implications of various deductions and contributions, like for HSAs or 401(k)s.

Google Google offers very strong retirement plans by providing its employees 401(k) matching and financial planning resources to not feel vulnerable about the future, which in turn increases their loyalty and long-term satisfaction.

In such plans, the employer combines the profit-sharing with the 401(k) plan. Profit-sharing Vs. 401(k). 401(k) is the name of a section in the Internal Revenue Code (IRS). Employees receive the amount at the time of retirement if it is merged with their 401(k) plan. Profit-sharing.

Switch to a high-deductible health plan. What to Do as Your Child Grows : Prepare your finances. When partnered with the standard 401(k) plan, you could end up with two powerful retirement funds. Let’s Start from the Beginning. This allows you to save on monthly premiums while putting tax-free money aside in your HSA.

Bonuses and commissions can give annual earnings a significant boost, and various benefits can also have a major impact on your employees’ finances and wellbeing. Company A also offers a 401(k) with contribution matching. In addition to the $80,000 salary, Company B offers a high-deductible health plan.

This includes copayments, deductibles, prescriptions, and more. Health savings accounts (HSAs): HSAs are available to those with qualifying high-deductible health plans (HDHPs). Contributions to an HSA are tax-deductible, and withdrawals for qualified medical expenses are tax-free. Plus, the funds can roll over year after year.

Some employees may prefer comprehensive plans, while others may opt for high-deductible plans with health savings accounts (HSAs). Retirement Plans: Offer various retirement planning options, including 401(k)s, IRAs, and pension plans. Highlight these benefits to attract and retain millennials and Gen Zers.

Others, such as 401(k)s, are less expensive to set up and don’t always require employer contributions. 401(k) is the most well-known retirement plan available to any business. Your company may also contribute funds to employees’ 401(k) plans. Step 6: Figure out who’s in charge.

In a 401(k) plan, the most common type of retirement plan, employees can save up to a certain amount set by the U.S. An HSA is a savings account into which employees who are enrolled in high-deductible health plans (HDHPs) can transfer funds to help cover eligible medical expenses tax-free. According to the U.S.

Employers can support them by providing employee financial wellness programs that help workers manage their money and take control of their finances. Why Employers Should Care About Financial Wellness According to Capital One, 73 percent of people say their finances are a major cause of stress.

Most of these were defined contribution plans, such as a 401(k) or 403(b) plan, but 12 percent had access to both defined benefit and defined contribution plans, and 3 percent only had access to a defined benefit retirement plan. Are they worried about how a health emergency might impact their finances? Other Key Benefits.

Congress has developed a variety of solutions to provide individuals and employers with tax-free solutions for financing health care expenses. An HRA with a higher deductible health plan can also provide savings opportunities for employers while providing more flexibility in the design of the health benefits. Problem: High turnover.

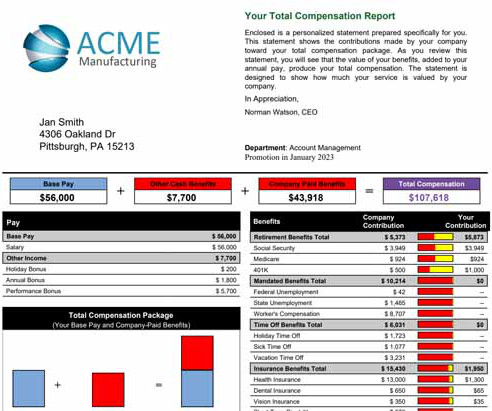

Unlike traditional pay stubs that only list basic salary and deductions, TCS encompass all monetary and non-monetary benefits that an employer provides. Retirement Plans : Contributions to 401(k) plans, pensions, and other retirement savings accounts. This includes: Base Salary : The fixed annual salary or hourly wage.

Can I afford to offer benefits such as 401(k)? Having a dashboard where you can check on these and other key performance indicators in a chart form can help you manage your company’s finances better. Can I afford to hire a new person, and what can I pay? So, the big question is: Do you know whether you’re making money?

Employers who offer a 401k plan can help by using a financial advisor that also provides free consultations to their investors. That knowledge can prevent already stressful situations like medical emergencies from becoming compounded by a lack of understanding about claims, deductibles, reimbursements, and the like.

Here are some ideas for financial benefits and professional development: Retirement savings plans : Offering retirement savings plans, such as 401(k) plans or IRAs, is a common benefit offered by many employers. The contributions made towards the pf are eligible for tax deduction under section 80c of the income tax act, 1961.

The personal finance benefits to married LGBTQ couples have expanded by leaps and bounds in the last decade since same-sex marriage was legalized. These individuals are 5% less likely to have a 401(k) or retirement plan and 12% less likely to have an IRA.

Retirement Plans: Such as 401(k) plans with employer matching contributions Retirement plans, especially 401(k) plans with employer matching contributions, are paramount among employee perks in the United States. A 401(k) is a tax-advantaged retirement savings program provided by employers.

Rippling Rippling offers a comprehensive suite of features to manage HR, IT, and finance- all under one roof, simplifying and centralizing operations for businesses of all sizes. Some of the features reviewed by ADP’s customers are quoted below- “The best thing I like is payroll processing for its accuracy and reliability.

Below is a description of seven income tax features that involve mathematical calculations: Tax Deductions- About 90% of taxpayers take the standard deduction and the rest itemize deductions when they are larger than their standard deduction. Next, deductions are subtracted from AGI to get taxable income.

I remembered the book, The Index Card , where ten tips related to many aspects of personal finance were shared on an index card. 401(k), 403(b), TSP). Keep Learning About Personal Finance - Learn one new thing every day about a personal finance. What to Do? I titled my presentation Just Do Then Things Right.

March is Womens History Month , a time to celebrate the achievements of women across industriesincluding finance. ” Many women prioritize family finances, retirement, or debt repayment over investing their HSA funds. One of those areas? Investing in health savings accounts (HSAs). “HSAs are too complicated to manage.”

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content