This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Certified Compensation Professional (CCP®) The CCP® certification, also from WorldatWork, specializes in compensation but covers a critical aspect of employee benefits — pay structures, salary planning, and compensation strategy. Best For: Financial advisors, benefits professionals, and HR specialists responsible for 401(k) retirement plans.

One of the cornerstones of retirement planning is the 401(k) plan, and choosing the right provider can significantly impact your financial future. In this article, we’ll explore the top 10 401(k) providers for 2023, each offering unique features and benefits to help you make an informed decision. What is a 401(k)?

If you’re a small business owner interested in starting a 401(k) plan for your employees, you already understand how they will benefit, but you should also understand how the plan will affect you. Sometimes, the traditional 401(k) plan doesn’t end up providing you the full benefit you’d hoped for.

Besides the 409A deferred compensation, there is also the qualified deferred compensation plan such as the 401(k)s. The executive staff receives portions of their earned salaries during retirement or later as agreed between both parties. Salary Continuation Plans: This NQDC plan is funded by the employees.

Should you auto-enroll your employees into your company’s 401(k) program? Automatic enrollment is exactly what it sounds like—you, the employer, automatically enroll your employees into your organization’s 401(k) plan. The 401(k) is pre-tax. You don’t need to shake a magic eight ball to make a decision.

How is your HSA vs. your 401(k) vs. your IRA shaping up for retirement planning? To help you prepare, here is a breakdown of three common retirement accounts: an HSA vs. a 401(k) vs. an IRA. A 401(k) is … A 401(k) is a retirement savings plan offered by many employers that provides tax advantages.

However, the tax deduction is limited to a maximum of 25% of the total salary of the employees in this qualified employee benefit plan. Nonetheless, some common examples include: 401(k). What’s more, some 401(k) contributors may also be further eligible for tax credits. Hybrid plan. Examples of qualified plans.

The changes, which the IRS releases in November each year, will affect contribution limits for HSAs, FSAs and 401(k) and other retirement accounts. Funds in an HSA can be rolled over indefinitely year after year and invested, much like a 401(k) plan. 7,750 for family coverage (up $450). Retirement plan maximums.

The increase in minimum full-time hourly wage will add up to an annual salary of around $40,000 USD for those working a 40-hour workweek. Image: Hobby Lobby Hobby Lobby Announces Wage Hike Across Stores Hobby Lobby’s starting wage is being increased to $19.25 USD effective immediately. Data from the U.S. USD or $36,675 USD per year.

While this is true, the concerns have more to do with specific retirement funds and employees’ 401(k) agreements with their employer. The report explains that due to the design of many 401(k) plans, the benefits don’t always line up when you switch from one employee to another.

Make sure you are getting the 401(k) match. Many employers will offer a 401(k) match up to a certain percentage. Let’s say your employer will contribute 50 cents on every dollar, up to 4% of your salary. Additionally, contributions to a 401(k) are made will pre-tax dollars, so you save on taxes as well.

401(k), 403(b), 457 plan, and thrift savings plan), and other employer benefits (e.g., eggs and meat), agritourism income, a salary earned through continued work for an adult child or other new farm owner, and income from non-farm related work. health insurance). barn, silo, riding arena), farm equipment (e.g.,

For 41 percent of small business employees, benefits are crucial when accepting a new job, second to salary. A matching 401(k) or pension. Today, unemployment rates are at a historic low, so many workers now have the freedom to choose where they want to work. And in many cases, it’s benefits offerings that seal the deal.

Examples include a 401(k) or 403(b) plan and traditional IRA. Some older adults have a higher tax bracket when they were working which can trigger IRMAA Medicare premium surcharges and/or the net investment income tax (NIIT). “To Tax-exempt income is income that is free from federal income tax.

One popular way to get your retirement plan sorted in the United States is through a 401(k) plan. A 401(k) plan is a type of retirement account offered by employers to their employees. How does 401(k) work? A 401(k) plan is that the money grows tax-free until it is withdrawn at retirement age.

Setting up a 401(k) for employees can be a daunting task for small business owners. 401(k)s allow employees to set aside a percentage of their salary to plan for their future retirement. 401(k)s allow employees to set aside a percentage of their salary to plan for their future retirement.

In 2025, salaries alone no longer define an attractive employment offer. At its core, the fringe benefits meaning refers to any compensation provided to employees beyond their regular wages or salaries. Financial Incentives Beyond salaries, employers might offer retirement plans (e.g., What are fringe benefits?

Examples: save $10,000 toward the cost of a new car in 10 years and save 10% of salary in a 401(k) plan for 25 years. SMART goals have an anticipated cost and time deadline. From there, you can “do the math” to determine attainability and measure progress. The Need for Flexibility - SMART goals cannot be too confining.

When it comes to FUTA tax, you will start by figuring out all the payments paid to your employees, including salaries, wages, sick pay, bonuses, contributions towards the 401(k), etc. Remember, your tax payment will be limited to the wage limit within your state.

The limit will be the greater of $10,000 or 150% of the standard catch-up amount for 401(k)s and similar salary reduction plans. Employer Retirement Plans - A “starter 401(k)” plan for employers with no current retirement plan will take effect in 2024. Auto Enrollment and Escalation - Before SECURE 2.0,

Examples include salary, wage, commission, bonus, and tip income, rents and royalties, interest, and required minimum distribution (RMD) withdrawals from tax-deferred retirement savings accounts (e.g., 401(k)s, 403(b)s, and traditional IRAs).

Figuring that defined-contribution plans such as 401(k)s weren’t nearly secure as they should be after the passage of the Setting Every Community Up for Retirement Enhancement Act of 2019, Congress is taking another stab at it with the Securing a Strong Retirement Act of 2021 (H.R. Student loans and 401(k) plans.

For instance, learning about different types of retirement accounts beyond a 401(k) can help employees decide which is best for them. Top talent wants more than a high-paying salary. In addition, learning about how to shop for a credit card can help employees avoid predatory interest rates.

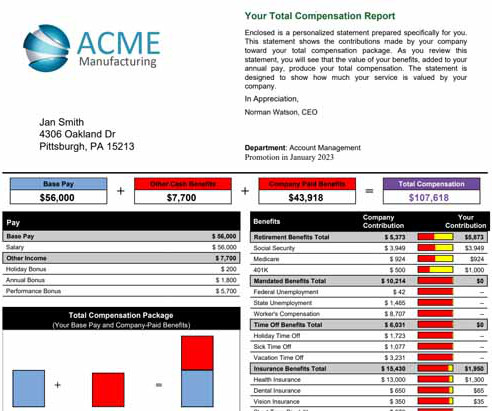

Beyond the Dollar Sign: The Power of Total Compensation Traditionally, compensation discussions often focused solely on base salary. TCRS provide a transparent breakdown of all aspects of an employee’s compensation package, including: Base Salary: The core component, outlining the annual or hourly wage.

employer-sponsored 401(k) plans. Act seeks to: Open access to 401(k) retirement plans to more people Provide greater opportunities to save Offer financial incentives to save while removing common barriers and penalties So, what does the law require of employers? The SECURE 2.0 The SECURE 2.0 The SECURE 2.0 The SECURE 2.0

401(k)s and 403(b)s), however, nor can RMDs for personal IRAs and inherited IRAs be combined. travel), charitable gifting, and re-saving the money in a taxable account or a Roth IRA if they have earned income (salary/wages and/or self-employment earnings) and are under the maximum income limits.

Whether it’s the precise match your organization offers for a 401k or how paid time off is calculated, benefits come with their share of complexity. For example, say a team member with an annual salary of $50,000 has a benefits package worth around $15,000. Their total compensation would then be valued at $65,000.

Estimate Your 2024 Income - Project your income from all sources, including wages/salary, investments, rental income, business income, etc. Consider any expected changes such as salary increases, job changes, side hustles, or expected increases or decreases in income. 401(k) plan).

The saga of 401(k) catch-up contributions under SECURE 2.0 For employees who contribute to more than one 401(k) plan during a year—an old employer’s plan and a new employer’s plan, for example—contributions into each plan would be treated separately for purposes of determining whether the $145,000 threshold has been reached.

A Gallup report stated that the cost of replacing an employee could range from one-half to two times the employee’s annual salary. Being willing to provide competitive pay for a role is the most straightforward approach a company can adopt, that is, providing a higher salary than other companies in the industry are offering.

Employers are often tasked with whether they should go for an ESOP or 401K plan since they are the most common. If you don’t want to delve into the whole ESOP vs 401K debate, then should you go for both an ESOP and a 401K? In this article, we cover the following to compare ESOP vs 401K plan: What is ESOP? What is 401K?

Does this mean you’ll earn more than your annual salary in 2020? Some employers may choose to divide employees’ annual salary over 27 pay periods instead of 26. lower each pay period during 2020 (although you’d make the same total salary). lower each pay period during 2020 (although you’d make the same total salary).

By providing employees with a clear and comprehensive overview of their total compensation package, including both direct pay (salary or wages) and indirect benefits, TCSs can significantly enhance employee satisfaction, loyalty, and engagement. It typically includes: Base Salary or Wages: The employee’s hourly or annual pay rate.

If you’re looking for the best and brightest talent, it’s smart to consider your 401(k) options. A retirement assistance plan, like a 401(k) plan, ranks #4 of 54 benefits and has the highest correlation with employee satisfaction. Consider the fee structure of the 401(k) plan you are interested in implementing.

One low fee enables a small business to keep track of their hourly, contracted, salaried, and tipped workers with ease. OnPay also offers a range of benefits for employees, including access to a 401(k) retirement plan and a range of health insurance options.

If you’re in the job market and get an offer with a salary that pays you $20,000 more than what you currently make, it goes without saying that you are supposed to take the money. Oftentimes a higher salary might not actually mean more money in your pocket. Retirement benefits – include 401(k)/403(b), pension plans, etc.

The cost of replacing an employee can range anywhere from six to nine months’ salary, according to data from SHRM. Retirement planning is one of the most common employee benefits offered by employers, specifically a 401(k) matching plan. Employer-sponsered emergency savings accounts may be funded similarly to 401(k) accounts.

Your EVP should include a number of components, including financial rewards, employment benefits, career development, a great work environment, and a strong company culture: Financial rewards cover things like salary, bonuses, and stock options.

Losing an entry-level employee can cost you up to half their salary, but losing a senior level executive can cost more than 400 percent of their salary. The cost of losing an employee at any level is significant. Those are just the direct turnover costs. A strong executive onboarding program can help reduce that risk of failure.

Jones] Employee benefits are typically any additional non-wage compensation provided to the employee beyond their typical salary or hourly wage. Traditional benefits include employer-offered healthcare, a 401(k) program, and vision benefits. What are benefits, perks, and discount programs?

The right educational offering just might be the deciding factor for candidates who are being sourced for similar jobs with matching salary packages. In addition to usual wants, like higher salaries and better work-life balance, employees are looking for special in-house training and skills development to help advance their careers.

59% of employees feel their salary has not maintained pace with the rising cost of living. You also don’t want to have to continually replace people who leave for a better salary – it’s costly and time consuming to recruit and train new employees. But increased salaries may not always be feasible.

Their services include 401(k) plans, pension plans, and personalized financial planning. times each employee's base salary on employee benefits, or add 20-50% to the employee's salary to cover benefits. Consider cost and value : Research indicates businesses typically spend 1.25

A six-figure salary doesn’t always translate to financial security. It’s a common misconception that a six-figure salary always translates to financial security and that high-earning employees have no need for financial wellness benefits. High-earning employees need financial help, too.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content