This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In this blog, we’ll explore how incentive theory shapes workplace strategies and the impact it has on employee engagement and performance. Whether it’s a financial perk, professional growth opportunity , or simple recognition, incentives help create a culture where employees feel valued and motivated to contribute their best.

Additionally, health savings accounts (HSAs) continue to gain attention as a powerful tool for retirementplanning, offering tax advantages and the ability to save for future healthcare costs. Employers should prepare for potential changes in healthcare policy, retirementplans, and wage laws.

The US Department of the Treasury and the Internal Revenue Service recently issued proposed regulations on the use of forfeitures by tax-qualified retirementplans. The proposed changes provide welcome clarity for plan sponsors but may require revisions to plan administration and legal plan documents.

The US Department of Labor (DOL) recently issued guidance for the first time on the investment of retirementplan assets in cryptocurrencies. The post When Are Cryptocurrencies Appropriate Investments for RetirementPlans and IRAs? appeared first on EMPLOYEE BENEFITS BLOG. Compliance Assistance Release No.

Retirementplan sponsors need to utilize updated Form W-4P (for periodic pension and annuity payments) and new Form W-4R (for nonperiodic payments and eligible rollover distributions) for income tax withholding elections beginning January 1, 2023.

In the second blog post in our three-part series to educate first-time participants, we walk through a few factors you should consider when choosing among employee benefits accounts for the first time. Click here for the first blog post in our series on choosing a health plan for the first time.

Retirementplan sponsors should be aware of a new Internal Revenue Service (IRS) pilot program, which permits plan sponsors to conduct a pre-examination “check-up” of retirementplan administration before the IRS begins a plan examination.

Fortunately, there’s an often overlooked way to help employees build wealth and prepare for retirement. Why HSAs for retirementplanning? These accounts provide another way for your employees to diversify their efforts to prepare for retirement. Click below to get your free HSA retirement white paper.

The post Save It for a Rainy Day: Recent Amendment Extensions for Qualified RetirementPlans, 403(b) Plans and Individual Retirement Accounts appeared first on EMPLOYEE BENEFITS BLOG.

Watch this short video as our own Jason Cook breaks down the retirement-planning potential of an HSA. The information in this blog post is for educational purposes only. Logging into our benefits mobile app – Log in and click on “View HSA Investments.” It is not legal or tax advice. The post It’s July.

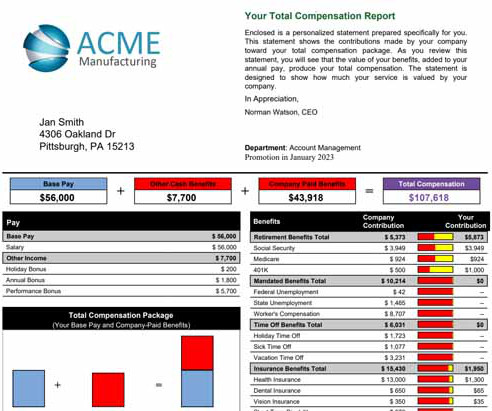

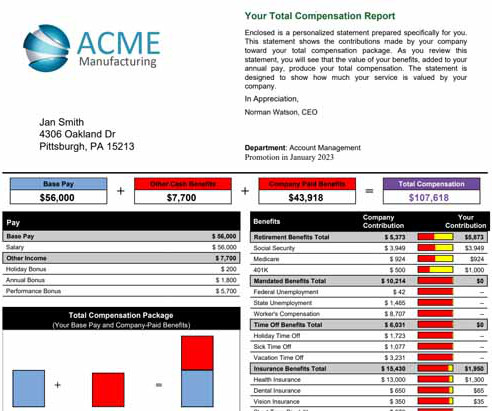

Benefits: A detailed breakdown of employer-sponsored benefits like health insurance, paid time off (PTO), retirementplans (including company contributions), and wellness programs. Salaried Employees: Focus on annual salary, bonus potential, retirementplan features, and detailed benefit summaries.

Earlier this year, the book reached #8 and #14 in Amazon’s wealth management and retirementplanning categories, respectively. blog posts and articles) and/or presentations (e.g., All three books are available on Amazon and sales for Flipping a Switch remain steady. Work Smarter, Not Harder - Books need not start “from scratch.”

Benefits: A detailed breakdown of employer-sponsored benefits like health insurance, paid time off (PTO), retirementplans, and wellness programs. Salaried Workers: Focus on annual salary, bonus potential, retirementplan options, and detailed benefit summaries.

Benefits: A breakdown of employer-sponsored benefits like health insurance, paid time off (PTO), retirementplans (including company contributions), and wellness programs. Salaried Employees: Focus on annual salary, bonus potential, retirementplan features, and detailed benefit summaries.

The Internal Revenue Service (IRS) recently opened a new determination letter approval program for 403(b) retirementplans—commonly used by nonprofit organizations—which allows sponsors of certain individually designed plans to apply for a favorable determination letter.

What do retirementplan professionals and participants need to know about the recently passed SECURE 2.0 appeared first on EMPLOYEE BENEFITS BLOG. appeared first on EMPLOYEE BENEFITS BLOG. Act of 2022?

Schedule workshops or webinars to break down complex topics like: Health savings accounts (HSAs) Flexible spending accounts (FSAs) Retirementplanning options Emphasize the total rewards picture Highlight how your benefits program fits into your companys total rewards strategy. Learn more by subscribing to our blog.

With political campaigns often influencing policy proposals from healthcare to retirementplans, this episode dives into what employers and professionals can expect and how they can prepare for potential changes. The information in this blog post is for educational purposes only. It is not legal or tax advice.

Beginning in 2024, employers and plan sponsors will need to implement new minimum eligibility rules, enacted by the SECURE and SECURE 2.0 Acts, that significantly expand eligibility for long-term, part-time employees to participate in employer-sponsored retirementplans.

Act codifying an opportunity for employers to provide matching contributions within a tax-qualified retirementplan based on their employees’ qualified student loan payments outside the plan. appeared first on EMPLOYEE BENEFITS BLOG. In December 2022, Congress enacted groundbreaking legislation as part of the SECURE 2.0

The Internal Revenue Service (IRS) recently issued new guidance clarifying key aspects of the broadened retirementplan eligibility rule for long-term, part-time employees under the SECURE 2.0

Retirementplan compliance (SECURE 2.0 Act introduces new retirementplan requirements, including automatic enrollment for some plans and changes to required minimum distributions. Action item: Consult with your plan administrator to ensure compliance with 2025 deadlines. Act updates) The SECURE 2.0

Benefits: A detailed breakdown of employer-sponsored benefits like health insurance, paid time off (PTO), retirementplans, and wellness programs. Salaried Employees: Focus on annual salary, bonus potential, retirementplan options, and detailed benefit summaries. healthcare, PTO).

Retirementplans often apply (and in some cases are required to use) multiple definitions of wages or compensation for various plan purposes. Given this complexity, failures to follow a plan’s definition of compensation are one of the most common issues experienced by retirementplan sponsors.

Benefits: A breakdown of employer-provided benefits like health insurance, paid time off (PTO), retirementplans, and wellness programs. Salaried Workers: Focus on annual salary, bonus potential, retirementplan options, and detailed benefit summaries. healthcare, PTO).

Targeted recommendations: By analyzing factors such as age, role, family status, and location, AI can suggest benefits options like health savings accounts (HSAs) , retirementplans, or wellness programs that are most relevant to each employee. The information in this blog post is for educational purposes only.

Lack of RetirementPlanning - Many people spend time planning meetings that last an hour, weddings that last a day or a weekend, and higher education (4-5 years). However, when it comes to planning what they will do over what could be a 30-year retirement, many people “just show up.”

Retirementplanning Healthcare costs are the biggest reason that household expenses increase during the first six years of retirement. The average 65-year-old couple is expected to need around $395,000 just for medical care in retirement. Traditional Health Plan Calculator today! It is not legal or tax advice.

Methods include webinars, podcasts, blogs, television and radio shows, print media, websites, and more. A key take-away, especially for healthy individuals and their families, is that HSAs can be used as a quasi-retirementplan. unmatched employer retirement savings, 6. listening to podcasts while walking).

Fiduciaries of 403(b), 401(a) and 457(b) retirementplans have come under increased scrutiny in recent years, in part due to participant lawsuits filed against plan sponsors and the resulting media attention.

On September 26, 2022, the Internal Revenue Service (IRS) extended the amendment deadline for non-governmental qualified retirementplans, plans covered under Section 403(b) of the Internal Revenue Code (Code) and individual retirement accounts (IRAs).

Having a clear understanding of their full compensation package allows employees to: Appreciate the Value of Benefits: Many employees underestimate the financial value of benefits like health insurance and retirementplans. For salaried workers, a focus on annual salary, bonus potential, and retirementplan options may be relevant.

The Internal Revenue Service’s (IRS) Employee Plans Compliance Resolution System (EPCRS) allows employers to correct errors involving the maintenance and operation of tax-qualified retirementplans. Act and the Future of the Employee Plans Compliance Resolution System appeared first on EMPLOYEE BENEFITS BLOG.

Act of 2022 enables business leaders to: Deliver additional financial benefits to round out an organization’s compensation strategy Remain competitive in an increasingly dynamic labor market Win the war for talent In this blog, we’ll discuss: What the SECURE 2.0 employer-sponsored 401(k) plans. The SECURE 2.0

With over 90 changes to retirementplans and individual retirement accounts (IRAs), this webinar will highlight the key changes for 401(k) and 403(b) plans and defined benefit plans, as […] The post JOIN US: SECURE 2.0 Takes Second Bite at Retirement Security appeared first on EMPLOYEE BENEFITS BLOG.

Nearly all employers offer eligible participants the opportunity to make additional catch-up contributions to their retirementplans. s Catch-Up Contributions, Age Is More Than Just a Number appeared first on EMPLOYEE BENEFITS BLOG. However, beginning in 2025, the SECURE 2.0 For SECURE 2.0’s

The Society for Human Resources Management’s (SHRM) express request service provides links and information about a wide variety of topics including state laws, seasonal topics like OSHA 300 postings, IRS RetirementPlan Limits, etc. HR service providers, like Kronos, offer resources by industry (i.e. banking, hospitality, retail, etc.)

I recently wrote a blog post about doing a mid-year financial check-up in early July so you have six months to work on planned action steps. Also be sure to adjust tax withholding for RMD withdrawals using quarterly estimated tax payments to the IRS or tax withholding by the retirementplan custodian.

How is your HSA vs. your 401(k) vs. your IRA shaping up for retirementplanning? Retirementplanning is a lot easier when you imagine what you want it to be like. Will you retire in Florida, or at a cabin in the woods? Would you like to learn more about HSAs and retirementplanning?

In this blog, well explore how payroll software can help organizations eliminate compliance risks, streamline payroll processes, and provide peace of mind for HR professionals and business owners. It might be difficult for companies with a large workforce to manually track and ensure compliance with these rules.

Retirementplanning for gen Z’ers? The post The Complete Guide to Flexible Benefits appeared first on Pacific Prime's Blog. Student loan benefits for baby boomers? Parental leave for the millennial that’s decided never to have kids? These are the dilemmas that many employers are now facing.

includes significant changes for retirementplan sponsors and employers, as discussed in our prior blog posts. If you are looking for a short summary organized by effective date, we have prepared a “pocket guide” chart, which can be downloaded here.

Because an HSA is a savings account, youll want to designate a beneficiary (or beneficiaries), just as you would with a 401(k) or other retirement-planning accounts. Stay updated on the latest trends and insight by subscribing to our blog ! The information in this blog post is for educational purposes only.

Benefits: A list of all benefits provided by the employer, such as health insurance, retirementplans, paid time off, and life insurance. It typically includes: Base Salary or Wages: The employee’s hourly or annual pay rate. Incentive Compensation: Any bonuses, commissions, or other performance-based pay.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content