This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The first phase of STP reporting included high-level data such as Gross, Tax, Allowances, Deductions, Lump Sums and Fringe Benefits. The next phase sees the reports moving away from Payment Summary Annual Rules (PSAR) and Payment Summaries for allowances and deductions to “Income Types.”

The formula for calculating net or spendable earnings may vary but is generally considered as Gross earnings less income taxes (state/federal/provincial) and other mandatory deductions. The National Commission on State Workmen’s Compensation Laws (1972) recommended a compensation rate moving to at least 80% of spendable earning s.

The first phase of STP reporting included high-level data such as Gross, Tax, Allowances, Deductions, Lump Sums and Fringe Benefits. The next phase sees the reports moving away from Payment Summary Annual Rules (PSAR) and Payment Summaries for allowances and deductions to “Income Types.”

The UAE’s new maternity leave law mandates that female employees are entitled to a minimum of 45 days of fully paid maternity leave commencing from the date of delivery. However, the total duration of maternity leave can extend up to 90 days under certain circumstances.

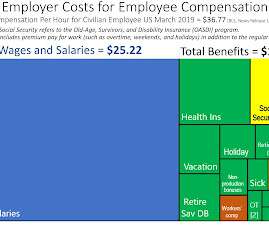

A recent study of manufacturing hourly compensation demonstrated a similar pattern for the main components (social insurance, wages or salaries, and direct benefits) paid by employers in Canada and Australia: The main divisions of employer costs for employee compensation under the BLS study are wages or salaries and benefits.

Due to COVID-19, the Equal Employment Opportunity Commission (EEOC) in 2020 waived its requirement that private sector employers submit EEO-1 data. California, Colorado, Connecticut, Maine, Massachusetts, and New York all have updated or new leave laws, each with its own details and requirements. California. Connecticut.

Families First Coronavirus Response Act (FFCRA) passed early in 2020 enacted a temporary PaidLeave Act (EPSL) as an extension of the Family Medical Leave Act (FMLA). You can still receive the Tax Credit as it applies, but it remains with only two weeks of paidleave through both years.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content