This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Legislation Determines the Mandate, Rules, and Arrangements Legislation in the United States, Canada, and Australia defines the mandate of workers’ compensation at both the state/provincial and federal levels. This includes coverage extent, benefit definitions, dispute resolution rules, and more. Self Insured : 24.7% Self Insured : 24.7%

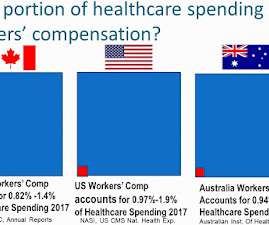

Private funding includes out-of-pocket healthcare spending by individuals on medical supplies and services, co-pays or deductibles. Using data from a number of sources, workers’ compensation spending on healthcare accounts for approximately 1% to 2% of total national healthcare spending in the US, Canada and Australia.

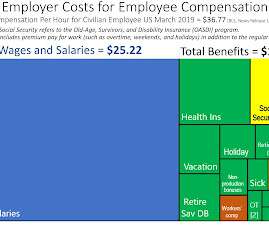

The cost of these coverages may be shared with the employees (with worker contributions deducted from the wages or salary) but are otherwise a form of earnings, providing value that a worker might otherwise have to purchase. What’s Reportable as Payroll for Workers’ Compensation? This is generally not the case.

In the accompanying slides and in some responses, I provide additional references as a starting point for understanding and comparing initial workers’ compensation. All workers’ compensationsystems pay the same rate for lost wages…right? A more obvious issues relates to the definition of any “initial period” of TTD.

The full claim cost under these types of insurance agreement develop quickly and definitively. Not necessarily so for workers’ compensation insurance. The true, full cost of the claim will develop over time and known definitively once the claim is concluded or "finalled". The insurer makes the payment and the claim is closed.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content