This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

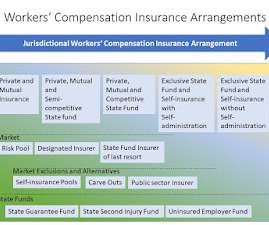

Regardless of the workers’ compensation model (private insurance, competitive state fund, exclusive state fund), every insurer has to prepare for the unexpected. Afterall, insurance is the transfers the financial risk of rare but costly events from the insured to the insurer. This limitation was noted at the time. billion).

Requiring employers provide financial compensation to workers or their families for work-related injury, illness and death is central to achieving this objective. This category includes state fund insurers that act as the “insurer of last resort” within the jurisdiction.

There was no Americans with Disabilities Act, no FamilyMedicalLeaveAct, and even the ground-breaking Title VII of the Civil Rights Act of 1964 was not even a decade old. First, the National Commission was enabled by the same law that created OSHA, the Occupational Safety and Health Act of 1970.

For workers’ compensation insurers, there are additional complications in their day-to-day operations. The medical and rehabilitation services often provided by workers’ compensation typically are very “hands on”. The degree to which this challenge may impact particular insurers remains to be seen but the risk is real.

COVID is the most extensive occupational exposure event in the history of the United States. Workplaces are now primed for a massive wave of compensation claims due to the Omicron variant. The issues will include: evaluating temporary disability benefits, delivering medical treatment, and estimating the nature and extent of disability.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content