This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

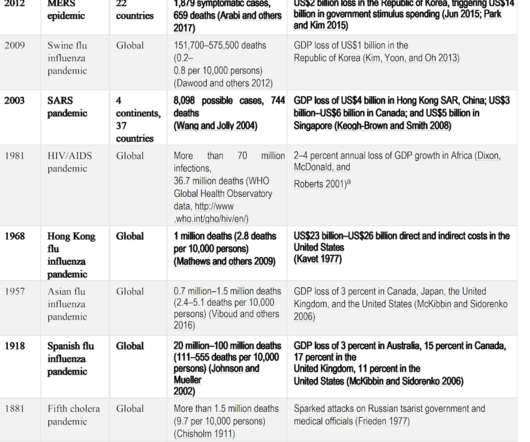

Regardless of the workers’ compensation model (private insurance, competitive state fund, exclusive state fund), every insurer has to prepare for the unexpected. As noted in my last post, the COVID-19 event most certainly is a rare event and just as assuredly will result in accepted workers’ compensation claims.

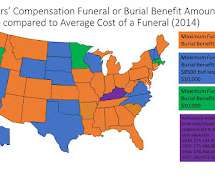

Every workers’ compensationsystem provides certain payments in the event of a work-related death of a worker. The expectation that workers’ compensation insurance will cover the full cost of a funeral and burial of an injured worker, however, is not the reality in all jurisdictions.

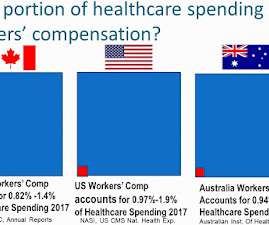

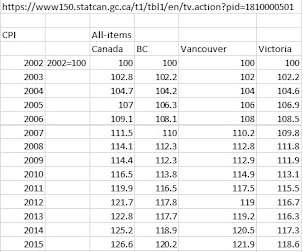

I’ve received a lot of questions recently on workers’ compensation healthcare spending in Canada, the US and other countries. These questions appear have arisen as several US states and political analysts have proposed consideration of “single payer” healthcare systems for their jurisdictions. See figure at top of this post.]

For more than twenty years I have been speaking about demographic change to workers’ compensation insurers in the hopes of spurring policy changes in advance of an aging workforce and greater numbers of older workers in the workplace. Workers’ compensation and occupational health and safety are not keeping pace.

In March 2022, I was honored to speak (briefly) at the Workers' Compensation Research Institute (WCRI) conference in Boston, see Friends, Romans, countrymen, lendme your ears (March 2022). However, society has moved on and "workers" today is more more acceptable; our workplaces are more diverse, vibrant, and inclusive.

[The following is a general response to questions from students in workers’ compensation, disability management, and workplace insurance courses. While prevention, control, and treatment questions top the list, workers’ compensation questions are being raised. The law and policy will vary by specific jurisdiction].

Workers with permanent disabilities often don’t have those options. The monthly workers’ compensation amount they receive may have sustained them initially but unless it is adjusted for the cost of living, permanently disabled workers will see the buying power of their workers’ compensation income decline with each passing year.

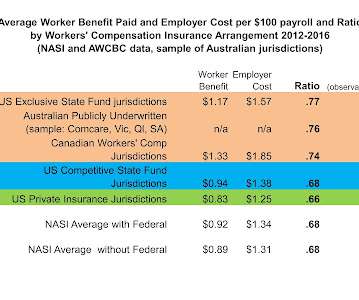

[For the first part of this discussion, see “Workers’ Compensation Insurance Arrangements: Does the model make a difference? Part 1” at [link] or [link] ] In my previous post, I described the range of public policy insurance arrangements governments use in the workers’ compensation insurance market.

Whether you work as a Case Manager for workers’ compensationsystem, a client services representative for a transport-accident personal-injury insurance, a claims administrator for a non-occupational disability insurance plan, or a return-to-work specialist for a third-party administrator, you will face the disability insurance “trust gap”.

[Supplemental background for students of DMCCJ – Workers’ Compensation and Return to Work and DMCCL- Insurance and Other Benefits – Pacific Coast University for Workplace Health Sciences] Workers’ compensation insurers and legislators are taking the first steps in dealing with the COVID-19 crises.

On May 19, 2020, claimant, a freight delivery driver, applied for workers’ compensation benefits on the basis of a COVID-19 diagnosis. Upon administrative review, the New York Workers’ Compensation Board affirmed. Background. The carrier appealed. COVID-19 is “Unusual Hazard”. Commentary.

The injured worker had alleged the co-employees had a financial motive in minimizing his medical care—they would receive additional pay if certain safety goals were maintained. The Supreme Court said accordingly, workers’ compensation immunity barred Plaintiff’s claim for negligent hiring, retention, and supervision.

The case began its journey through the states workerscompensationsystem: first to Deputy Commissioner Stephenson, who, after a hearing on September 10, 1975, found the claim compensable and awarded benefits. But in 1971, such cases fell into a troublesome gap in North Carolinas workerscompensation framework.

The soon-former Secretary of Transportation said Airlines have a legal obligation to ensure that their flight schedules provide travelers with realistic departure and arrival times." In short, it sounds a lot like the Florida workers' compensationsystem of the 1990s. You have "status" here.

Her statement resonated with my own experience attending workerscompensation conferences in each of the past five decades. Many of the issues facing workerscompensationsystems are perennial; the relative priority and details change with the times, but the themes are enduring. 1952) Workmens compensation law.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content