This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

With more than half of all private sector employeesenrolled in high-deductible health plans , it’s important that employers have in place certain protocols to ensure that they are a success. The employer can also contribute to its employees’ HSAs to encourage participation.

In the first post of this year’s open enrollment series, we break down some of the common feedback we received from those who said their benefits options were lacking so you can build the best benefits package going into your open enrollment. Specific responses included: “A lower deductible or copay options would be an improvement.”

One of the health insurance trends that went largely unnoticed in 2021 was that employers halted cost-shifting to their employees by reducing or holding steady workers’ deductibles and other cost-sharing. in 2021, employers did not increase employee’s share of premiums significantly.

More employees are enrolling in a high-deductible health plan (HDHP) each year, including more than half of U.S. But there are still misunderstandings that exist among employees about the significant value of an HDHP (or HSA-eligible health plan) and how it compares to a traditional health plan.

The tax benefits allow employers to deduct the stated $5,250 annually per employee as a business expense if spent on education assistance programs but any amount spent beyond that is taxable. This is likely the reason why Disney has chosen to cut down on the college tuition perks it is willing to offer.

HSAs allow your employees to put away funds to pay for future medical expenses. Usually, these accounts are funded with pre-tax deductions from your employees’ paychecks, but if they didn’t max out their contributions last year, they still can do so up until the tax-filing deadline.

The term “high deductible health plan” has often carried with it a negative connotation for employees. According to a recent article from SHRM covering research from the Employees Benefit Research Institute (EBRI), enrollment in an HDHP promotes more conscious health care purchase decisions. Like this blog?

As we enter 2022, there are a number of changes on the horizon that plan sponsors need to be aware of as they will affect group health plans as well as employeesenrolled in those plans. 1, 2022, HDHPs must charge enrollees for telehealth services if they have not yet met their deductible. . That comes to an end Dec.

With more than half of all private sector employeesenrolled in high-deductible health plans , it’s important that employers have in place certain protocols to ensure that they are a success. The employer can also contribute to its employees’ HSAs to encourage participation.

There are a number of issues that Medicare-eligible workers face that your human resources staff may be asked about, such as: Penalties for late Medicare enrollment, Whether the employer plan is the primary or secondary payer of claims, and. The following are considerations for employers faced with workers nearing 65.

FSAs are primarily funded by employees through pretax deductions, although employers may make contributions. Tax advantage: Employees’ and employers’ contributions are excluded from employees’ wages and aren’t subject to income or FICA taxes. Employers set their maximum contributions when designing the plan.

Open enrollment is underway for many companies right now and one benefits offering that may be on the menu this year is an FSA. Employers are constantly looking for ways to remain competitive in their benefits offerings, and an FSA is a great add-on to your benefits package. Copays, co-insurance, and deductibles for medical care.

A 401(k) plan is a type of retirement account offered by employers to their employees. It allows employees to save a portion of their pre-tax income for retirement. The contributions are deducted from the employee’s paycheck before taxes are withheld, which reduces their taxable income. How does 401(k) work?

Employers can help their employees by offering worksite benefits like hospital indemnity insurance and other supplemental benefits. And, for most hospital indemnity plans, there are no deductibles, provider networks or other complications to worry about. Encourage employees to seek care when they need it.

Health Insurance: The workers will be entitled to enroll with the comprehensive health plan which will help them overcome the future financial assistance that may arise due to an unknown event or accident that harms their health or body. The benefits will be equitably offered to all the employees.

” Although rising premium rates are an on-going challenge for employers, a primary (and popular) method to overcome this is to implement a high-deductible health plan (HDHP). Overcoming the Challenge Implement an HDHP with Complementary Accounts A growing number of employers have implemented an HDHP as a choice for employees.

Many employers’ tech stacks consist of disparate systems for payroll/HRIS and benefits administration (ben admin). This means if you change an employee from hourly to salary in the ben admin platform, the payroll system would not be updated. If so, consider how this might impact the enrollment window you allow for your employees.

For example: In an individual coverage health reimbursement arrangement, the health reimbursement arrangement is offered in place of a group health plan, allowing employees to purchase a health plan on their own. Healthcare.gov says that employees must be enrolled in individual health plans, such as a Marketplace plan, to use the funds.

Many receive this coverage as a benefit of their employment. Employers who do not offer coverage can have a more difficult time attracting recruits and retaining employees. All members contribute to the plan, as well as the employer, to help reduce health care costs for every member. Read on for a thorough overview.

Health savings accounts can be a good deal for employees. High deductible health plans (HDHPs) are on the rise as a growing number of employers turn to consumer-directed health plans to try to curb costs—the portion of employeesenrolled in HDHPs rose from 26.3% Use Employee Education to Educate about HSA Value.

Flexible spending accounts (FSAs) are employer-established accounts that allow you to put aside pre-tax dollars from your paycheck into a special account to be used for eligible health or dependent care expenses. The card is issued by the benefits provider that the employer has chosen to work with for the FSA.

If employees requested more communication or decision-support tools on your enrollment portal, they might be disappointed and discouraged if they don’t see any updates. Even just updating your enrollment booklet online and adding new FAQs can be a tremendous help to your employee population. What If We Add New Benefits?

Unlike traditional benefit accounts such as Flexible Spending Accounts (FSAs) or Health Savings Accounts (HSAs), LSAs are primarily designed to cover a broad range of expenses related to employees’ physical, mental, and financial wellness. HSAs can be funded by both employer and employee.

Assessing open enrollment and employees’ overall involvement in benefit offerings should be a big part of any year-end HR checklist. Obviously you and the providers you select for your benefit offerings need to know how many employeesenroll in each plan. According to attorney Robert Y.

However, it highlights the need to use multiple communication channels – especially when it comes to Open Enrollment. We conducted a survey earlier this year to evaluate how employers planned to communicate during Open Enrollment. Most employers have access to these communication methods already, so there’s no additional cost.

And yet, that’s not how most employees understand them — if they understand them at all. About half of American employers offer HSAs — coupled with high-deductible health plans (HDHPs) — but, according to one study , 69% of employees don’t understand their benefits or uses.

As a result, many employers are increasingly turning to voluntary employee benefits, which allow them to provide valued, high-demand benefits to employees at little or no cost to the company. Voluntary benefits have been becoming more popular among employers in recent years as unemployment falls.

While not ideal for everyone, a high-deductible health plan can be very appealing to some workers, especially when it’s paired with a health savings account. Offering a high-deductible health plan as part of an employee benefits package, therefore, may be a strategic option for your organization.

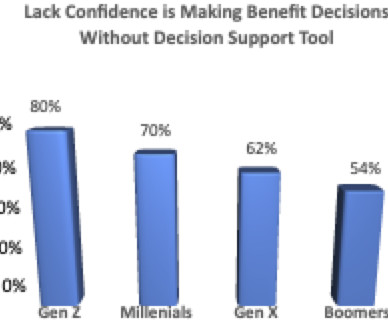

A 2022 Harris poll found that 72% of employees said “they wish someone would tell them what the best health insurance for their unique situation is.” AI Enabled Benefits Education According to a recent study by the Hartford, “76% of employers say educating employees about benefits” remains challenging.

One of the most difficult aspects of annual open enrollment is reaching workers who are disengaged from the process and never bother signing up for your group health plan and other benefits they could take advantage of. Young workers will often forgo their employer’s health plan as they are still covered by their parents’ plans.

As the workforce ages and many employers want to keep on baby-boomer staff who have the experience and institutional knowledge that is irreplaceable, one issue that always comes up is how to handle health insurance. Part D, meanwhile, covers prescription drug costs.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content