This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

With more than half of all private sector employeesenrolled in high-deductible health plans , it’s important that employers have in place certain protocols to ensure that they are a success. Providers in an insurer’s network may charge vastly different rates for the same procedure.

As we enter 2022, there are a number of changes on the horizon that plan sponsors need to be aware of as they will affect group health plans as well as employeesenrolled in those plans. 1, 2022, HDHPs must charge enrollees for telehealth services if they have not yet met their deductible. . That comes to an end Dec.

This software is a comprehensive platform that allows HR professionals, benefits managers, and employees to efficiently manage, access, and make decisions regarding benefits such as health insurance, retirement plans, leave policies, and more. It offers automated benefits administration, including health insurance and retirement plans.

In the first post of this year’s open enrollment series, we break down some of the common feedback we received from those who said their benefits options were lacking so you can build the best benefits package going into your open enrollment. Specific responses included: “A lower deductible or copay options would be an improvement.”

If you decide to keep them on the company’s plan, how you handle their insurance depends on your size: Fewer than 20 employees — Employees who work for these firms will need to enroll in Medicare when they turn 65. Medicare will be the primary payer of health insurance claims for these workers under the law.

And yet, that’s not how most employees understand them — if they understand them at all. About half of American employers offer HSAs — coupled with high-deductible health plans (HDHPs) — but, according to one study , 69% of employees don’t understand their benefits or uses. Very few savings accounts offer similar benefits.

More employees are enrolling in a high-deductible health plan (HDHP) each year, including more than half of U.S. But there are still misunderstandings that exist among employees about the significant value of an HDHP (or HSA-eligible health plan) and how it compares to a traditional health plan.

Are you offering your employees health insurance options that work for their budgets? While not ideal for everyone, a high-deductible health plan can be very appealing to some workers, especially when it’s paired with a health savings account. By opting for a higher deductible, employees can secure lower monthly premiums.

One of the health insurance trends that went largely unnoticed in 2021 was that employers halted cost-shifting to their employees by reducing or holding steady workers’ deductibles and other cost-sharing. in 2021, employers did not increase employee’s share of premiums significantly.

With more than half of all private sector employeesenrolled in high-deductible health plans , it’s important that employers have in place certain protocols to ensure that they are a success. Providers in an insurer’s network may charge vastly different rates for the same procedure.

One of the most difficult aspects of annual open enrollment is reaching workers who are disengaged from the process and never bother signing up for your group health plan and other benefits they could take advantage of. Turning 26 — This is the age that individuals are no longer allowed to be covered by their parents’ health insurance.

workers postpone health care needs because they’re worried about cost, even if they have health insurance. Medical care can be expensive, and group health insurance isn’t always enough. Employers can help their employees by offering worksite benefits like hospital indemnity insurance and other supplemental benefits.

HSAs allow your employees to put away funds to pay for future medical expenses. Usually, these accounts are funded with pre-tax deductions from your employees’ paychecks, but if they didn’t max out their contributions last year, they still can do so up until the tax-filing deadline.

Changing life events in the middle of the year usually means changes to your health insurance plan. If an employeeenrolls in a high-deductible health plan (HDHP) mid-year, how does that affect the amount they can contribute to their health savings account (HSA)?

A good portion of Americans have health care coverage through a group insurance policy. However, most people are fairly unsure of what group insurance coverage actually is and how it works. Without insurance coverage, it can be difficult to pay for medical expenses, whether or not they are expected.

Many employees are coming to the end of the year and realizing that they still have a lot of money in their FSA accounts that they need to spend. They may also be questioning whether they have a need for an FSA and if so, how much they should choose to have deducted each month. Copays, co-insurance, and deductibles for medical care.

Health Insurance: The workers will be entitled to enroll with the comprehensive health plan which will help them overcome the future financial assistance that may arise due to an unknown event or accident that harms their health or body. The benefits will be equitably offered to all the employees.

A side-by-side comparison of premiums, contributions and/or deductibles for each option. An explanation of any changes from the previous year and any actions your employees may need to take. From there, create a communication schedule to remind employees of the benefits enrollment period.

FSAs are primarily funded by employees through pretax deductions, although employers may make contributions. Tax advantage: Employees’ and employers’ contributions are excluded from employees’ wages and aren’t subject to income or FICA taxes. Eligibility: FSAs are generally available only to current employees.

” Although rising premium rates are an on-going challenge for employers, a primary (and popular) method to overcome this is to implement a high-deductible health plan (HDHP). Overcoming the Challenge Implement an HDHP with Complementary Accounts A growing number of employers have implemented an HDHP as a choice for employees.

This may be a good option for employers that want to simplify their health plan administration while giving employees flexibility. Even with health insurance, dental insurance and vision insurance, employees tend to end up with some out-of-pocket costs that aren’t covered by their various plans. Manage enrollment.

Health savings accounts can be a good deal for employees. High deductible health plans (HDHPs) are on the rise as a growing number of employers turn to consumer-directed health plans to try to curb costs—the portion of employeesenrolled in HDHPs rose from 26.3% But do they really understand HSA value? in 2011 to 39.3%

Your employees make a lot of decisions during their work day, but one of the most important decisions they’ll make comes once a year: what to do about their employee benefits. Tech-based tools can make it easier for employees to plan, budget and plug the gaps in their insurance needs. Plan-comparison tools.

Reimbursements from a healthcare FSA can only be paid to reimburse the employee for qualified medical expenses incurred during the period of coverage. While FSA funds are deducted by the employer during payroll , the benefits vendor administering the FSA is responsible for verifying the receipts rather than the employee.

A side-by-side comparison of premiums, contributions and/or deductibles for each option. An explanation of any changes from the previous year and any actions your employees may need to take. From there, create a communication schedule to remind employees of the benefits enrollment period.

How voluntary benefits work Voluntary benefits are arranged by employers but either paid for by staff via payroll deduction or by the employers themselves. The employer deducts any fees or premiums for these benefits from employee paychecks and forwards them in a single batch to the benefit vendors.

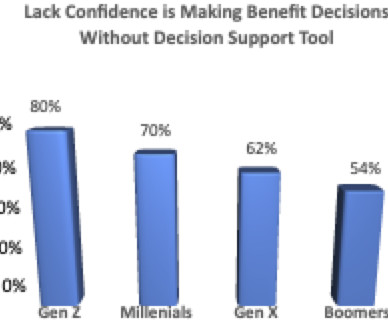

Decision Support Think your employees aren’t interested in decision support? A 2022 Harris poll found that 72% of employees said “they wish someone would tell them what the best health insurance for their unique situation is.” Think again. Be mindful that not all decision support tools are created equal.

As the workforce ages and many employers want to keep on baby-boomer staff who have the experience and institutional knowledge that is irreplaceable, one issue that always comes up is how to handle health insurance.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content