This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

According to the report, in 2023: Group term lifeinsurance premiums increased 10% from the 2022 level. Group universal life and whole life were up 9%. Critical illness insurance premiums were up 7%. Hospital indemnity premiums were 6% higher. Dental coverage was up 5%.

Deductible : the amount an employee must pay out-of-pocket each year before their insurance kicks in; this does not apply to preventative care, like annual physicals. Co-insurance: the amount an employee must pay after meeting their deductible; under most plans, this is around 20% of full price. Benefit types and classes.

Such risks can manifest themselves in larger out-of-pocket expenses, or cash flow issues at the beginning of the plan year, while they work to satisfy their deductible. Some of these decisions, such as foregoing healthcare, disability, and lifeinsurance, could prove catastrophic.

How voluntary benefits work Voluntary benefits are arranged by employers but either paid for by staff via payroll deduction or by the employers themselves. The employer deducts any fees or premiums for these benefits from employee paychecks and forwards them in a single batch to the benefit vendors. cancer insurance) Pet insurance.

Payroll deductions This item spells out each of the deductions the company withholds, including federal, state, and local taxes and other things, including voluntary deductions for benefits. It covers things including hospital and doctor visits, surgeries, and prescriptions. An HSA may earn interest, which is not taxable.

There are four major types of employee benefits many employers offer: medical insurance, lifeinsurance, disability insurance, and retirement plans. Medical Insurance. Medical insurance is likely a no-brainer— it’s one of four major types of benefits most employers offer. HospitalInsurance.

What is supplemental lifeinsurance? It’s a type of lifeinsurance policy that’s often available through work and provides additional coverage. What is supplemental lifeinsurance? Supplemental lifeinsurance fills in coverage gaps and provides additional lifeinsurance coverage.

Other types of insurance If an employee loses their ability to earn an income on a temporary or permanent basis, certain types of insurance can help protect their families and livelihoods. Disability insurance , provides employees with replacement income and pays for medical bills if they become disabled and are no longer able to work.

The term “ancillary” means “providing additional help or support,” and that’s just what ancillary health insurance does. Often referred to as “ancillary benefits,” ancillary insurance can include coverage for miscellaneous medical expenses incurred during a hospitalization that may not be covered by your group health insurance.

To qualify as such, the government states the plan must “pay at least 60% of the total cost of medical services for a standard population” and “include substantial coverage of physician and inpatient hospital services.”. Medical plans with no or low-cost deductibles. Insurance that is accepted at a greater range of places.

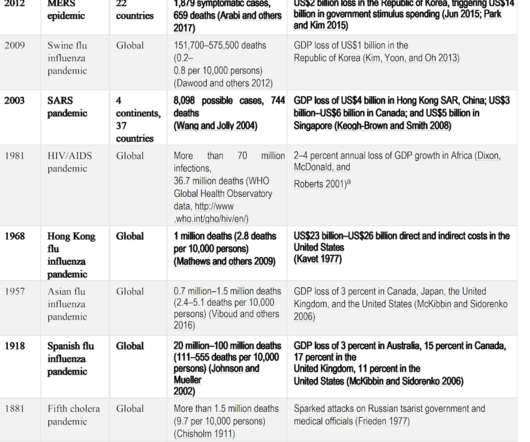

In hospitals and government offices, contingency plans were developed for many risks but one epidemic helped spur some workers’ compensation systems to take specific action to prepare for the “know unknown”: the emergence Severe acute respiratory syndrome (SARS). [P. You can think about it as insurance for insurers.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content