This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

To take advantage of an HSA, you need to participate in an HSA-eligible health plan (or high-deductible health plan). HSA-eligible health plans typically have lower premiums but higher deductibles. Assess your ability to cover the deductible before choosing this plan.

There are four major types of employee benefits many employers offer: medical insurance, lifeinsurance, disability insurance, and retirement plans. Medical Insurance. Using untaxed dollars in an HSA to pay for deductibles, copayments, coinsurance, and some other expenses can lower overall health care costs.

To take advantage of an HSA, you need to participate in an HSA-eligible health plan (or high-deductible health plan). HSA-eligible health plans typically have lower premiums but higher deductibles. Assess your ability to cover the deductible before choosing this plan.

Often referred to as “ancillary benefits,” ancillary insurance can include coverage for miscellaneous medical expenses incurred during a hospitalization that may not be covered by your group health insurance. Examples of this coverage could include ambulance transportation, drugs and medical supplies, such as bandages.

The plan’s popularity is also aided by the fact that the employers matching contributions to the plan are tax deductible, allowing both parties to make a useful contribution to the employee’s future. Can Employers Deduct Fringe Benefits?

Group lifeinsurance premiums provided to employees over $50,000. Group-term lifeinsurance coverage. Transportation (commuting) benefits. Most taxable benefits are subject to Canada Pension Plan, Employment Insurance, and income tax deductions. Which Benefits Are Considered Taxable? Paid vacation.

Health Insurance. Other Insurance (Dental Insurance, Vision Insurance, LifeInsurance, Disability Insurance, Pet Insurance, etc.). Various Perks (Gym Membership, Transportation Benefits, etc.). In addition to the $80,000 salary, Company B offers a high-deductible health plan.

Taxable vs. Non-taxable Benefits are always tax-deductible, aren’t they? Taxable examples of fringe benefits might include: Gym memberships Moving stipends beyond the actual moving cost Personal use of a company car Frequent flyer miles when converted to cash Certain lifeinsurance payments Information like this can come as a shock.

The IRS does not mandate accountable plans, but having such a plan in place enables your business to conform to IRS regulations concerning deductible reimbursements and reimbursements that are judged taxable income. Airfare, train, and/or other transportation expenses should be considered reimbursable expenses.

Medical plans with no or low-cost deductibles. Insurance that is accepted at a greater range of places. The company paying a higher portion of the insurance premium. Organizations also frequently provide employees with free or low-cost lifeinsurance. Outstanding pharmaceutical and/or hospitalization coverage.

Insurance types: Medical, dental, vision, disability, and lifeinsurance plans. Tax-preferred plans: Health flexible spending accounts, health savings accounts, health reimbursement accounts, transportation accounts, and more. Deductions must be set up in payroll and carrier invoices must be paid each month.

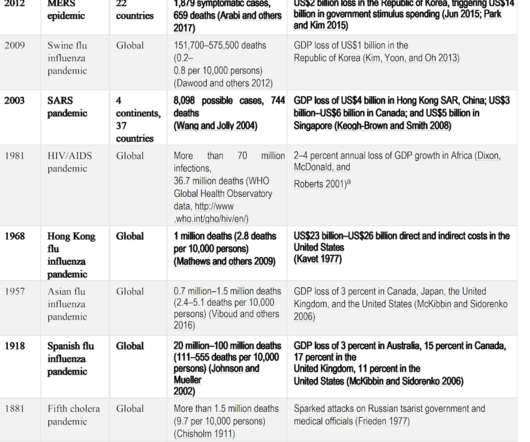

The consequences of higher death rates across all demographics during a largescale pandemic on lifeinsurance underwriters and government social insurance as well as on workers’ compensation insurers. As with most insurers, workers’ compensation insurers create “reserves” for risks like these.

Emergency towing and assistance coverage helps cover unexpected expenses for services like towing and fuel delivery, including battery replacement and transport to a repair facility. Select a higher deductible. Make sure to consult your insurance advisor before increasing your deductible. Consider seasonal insurance.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content