This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In other words, take action once to automate financial transactions such as payroll deductions for a 401(k) or regular automatic deposits to buy stock or mutual funds. pension or annuity) are more likely to spend money and less likely to feel financial stress than those who withdraw money from investments to pay living expenses.

2021) or 90% of current year (2022) tax liability using a W-4 form at work for job-related income tax withholding; withholding for Social Security, a pension, and required minimum distributions through account custodians; and/or quarterly estimated payments using IRS Form 1040-ES.

A significant return on investment from awards is augmented by their tax deductibility. As per the Internal Revenue Service, you can deduct up to $400 for non-qualified employee achievement awards and $1,600 for qualified awards given to the same employee within a year.

However, the tax deduction is limited to a maximum of 25% of the total salary of the employees in this qualified employee benefit plan. SEP – Simplified Employee Pension. As an employer, your contributions towards a qualified plan are tax-deductible. Hybrid plan. SOP – Employee stock ownership plans. Keogh (HR-10).

This includes Social Security recipients, retirees with COLA-adjusted pensions, and workers with COLAs stipulated in their job or union contracts. Standard Deduction - The amount of income taxpayers can shelter from income taxes rises with inflation (e.g., When bracket incomes rise, people may be taxed at lower tax rates.

Many older adults also have multiple income sources including Social Security, a pension, full-or part-time work or self-employment, withdrawals from retirement savings (including taxable required minimum distributions or RMDs), and interest, dividends, and capital gains on investments. In other instances (e.g.,

Tax Write-Off for Self-Employment Tax - On line 15 of Schedule 2 (for a 1040 form), self-employed workers can write off the deductible portion of their self-employment tax (calculated on Schedule SE), which will lower adjusted gross income (AGI), a trigger for many other taxes.

Pension Payment Sequencing - Taxpayers fortunate to have a pension may want to delay their work exit date/pension start date to do Roth conversions or realize capital gains on taxable accounts before RMDs begin. Individuals must “do the math” to see if this strategy will work.

Transitioning to a superior provider is no longer a hassle: If you’re contemplating changing your current workplace pension scheme, the process isn’t as challenging as you might think. Many pension companies (we’re one of them!) What is a workplace pension? are prepared to assist you with the heavy lifting.

Set aside a portion of self-employment income to send to the IRS for quarterly estimated tax payments (and/or over-withhold on a pension or Social Security) to ensure compliance with tax regulations. Contributions to non-Roth accounts are often tax-deductible, thereby reducing adjusted gross and, ultimately taxable, income.

When you’re filing your tax returns, what expenses can you deduct from business income? To start with, a business expense must be both ordinary and necessary to be deductible, according to the IRS. Deducting Business Expenses: Separating Fact From Myth. You must capitalize some costs rather than deduct them.

For example, workers with a guaranteed pension and/or a high investment risk tolerance might want to have more stock exposure in a TDF and would chose a target date farther off in the future. Make Tax-Advantaged Gifts - Consider “bunching” charitable donations with other tax deductions (e.g.,

Tax Refund Adjustments - Sometimes people miss a tax credit, deduction, or adjustment and need to file an amended tax return. Unclaimed Money - This is money held by state governments from a variety of sources including bank accounts, utility deposits, pension benefits, and insurance policies.

One of the few things that taxpayers can do to reduce their income taxes after a calendar year ends is to make a tax-deductible contribution to a traditional individual retirement account (IRA) or a SEP-IRA (for small business owners and/or their employees). Many have accumulated significant sums and need tax planning help.

Tax Bracket Triggers - When earnings are added to a pension, Social Security, RMDs, and other taxable income, planning is needed to avoid a higher tax rate or Medicare premium. Medicare Premium Tax Write-Off - Self-employed people age 65+ who are enrolled in Medicare Part B and D can deduct their monthly premiums against business income.

Credit: elina.nova/Shutterstock What are master trust pension schemes? Master trusts are defined contribution pension schemes , set up under trust law, which allow multiple employers that are unconnected with one other to participate. Master trusts have grown dramatically since auto-enrolment legislation was introduced.

Flexible pension policies can help employees shore up short-term financial wellbeing, while still saving for the future. In difficult periods, the ability to flexibly drop or pause pension contributions could be invaluable. One thing that might feel set in stone is pension contributions.

A former director of 1066 Target Sports in St Leonards, East Sussex, has received a £15,000 fine for withholding legally-required pensions information. This caused a degree of distress to the people affected, as the money they thought was going into their pensions didn’t. It caused them real concern.”

Herbert Smith Freehills, Citizens UK, Aviva, and Phoenix Group this week became among the first employers to sign up to the new Living Pension Employer standard , launched by the Living Wage Foundation. The living pension is a voluntary savings target of 12% of an employee’s salary, whereby the employer contributes 7%.

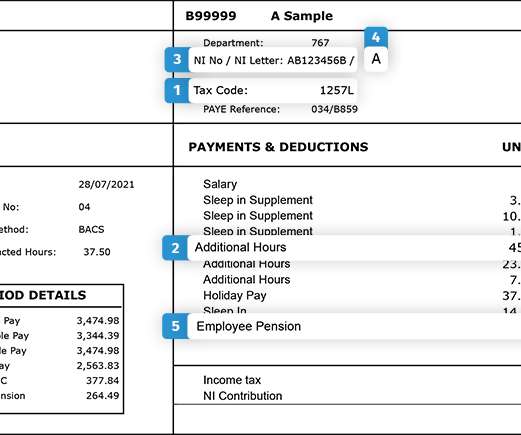

For the 2021/22 tax year (and through to 2025/26), the tax code for most people under 65 who only have one job or pension is 1257L. HMRC stores a history of everyone’s National Insurance contributions (NICs), which builds up entitlement to a basic state pension, under their NI number (which is unique to them). Pension payments.

Qualified retirement plans include: Qualified pension plans. Simplified Employee Pension (SEP) plans. Payroll deduction IRAs with automatic enrollment. Participating employers will deduct a default rate of 5% of pay from the paycheck of each employee at least 18 years old and deposit it into the individual’s CalSavers account.

Yet, many businesses might be inadvertently losing money because they lack a competitive pension package. Therefore a business with a team of 100 could pocket savings of up to £65,000 annually with a strategic pension plan. By presenting a more enticing pension proposal, firms can foster greater employee loyalty.

For employers, determining the contributions to a workplace pension scheme depends on the pensionable earnings of their employees. This article will explain the different methods for calculating pensionable earnings and how these methods affect pension contributions and tax efficiency. Employee contribution (inc.

It has a normal pension plan and a few related insured benefits. Its pension contributions are a lot higher than ours, but then our scheme is well below market, as I have been complaining about for some time. The problem is: to remove any holiday we would have to buy them out, which would add pension and bonus costs.

Whilst a workplace pension provides a savings vehicle for retirement, many organisations want to put in place a tax efficient savings option for those looking to save in general and build financial resilience. Contributions can also be made from maturing SAYE schemes to help protect from capital gains tax and ensure tax free growth.

From calculating employee salaries to managing taxes and deductions, payroll processing is a critical aspect of any business. Payroll processing is the act of computing and distributing employees’ compensation, including salaries, wages, incentives, and other benefits, as well as any relevant taxes, contributions, and deductions.

Employee benefits are defined as ‘non-salary compensation provided to employees in addition to their salary or hourly pay’ These benefits may include private medical insurance, pension contributions , childcare vouchers, a car scheme , and other perks such as discounts on gym memberships, travel, or education.

In the wake of recent developments, we are pleased to provide insights into Pension-Linked Employee Savings Accounts (PLESAs) under the Secure 2.0 The legislative intent of a PLESA is to allow low- and middle-income employees to use payroll deductions to accumulate funds that they can use in the event of an emergency.

It offers financial wellbeing support , provided by Salary Finance, such as lower interest and higher acceptance rate loans, and a help-to-save scheme that deducts savings from salaries each month, and has launched a dedicated intranet site for its cost-of-living support.

Many employers offer payroll-deducted savings schemes for effortless saving. Start saving early – Starting to save when you are younger into ISAs and a pension means that the money has lots of time to grow. Some employers will match additional contributions (up to certain limits).

Some of the reasons are: Around 75% of the employees expect their employees to provide better retirement benefit pension plans. The pension rules are complicated, and tax-related basics of retirement benefits can confuse an employer. The pension plans for employees are either qualified or non-qualified kinds. Work Smart.

“[Under] 40 percent of nonretired adults think they are on track in saving for their golden years and 25 percent have no retirement savings or pension at all.” Before saving with an HSA, you need to make sure you take care of the following: Enroll in a High Deductible Health Plan (HDHP). Households released in May 2018.

monthly or weekly) and Tax and National Insurance is deducted. Benefits Employees who were eligible for annual leave and workplace pension contributions will continue to accrue these whilst on parental leave. Statutory maternity pay (SMP) is 90% of an employees average weekly earnings (before tax) for the first 6 weeks and £156.66

This is the effect of deductions from wages which reduce pay for NMW purposes and includes salary sacrifice arrangements, such as for pension contributions. Salary sacrifice is an arrangement whereby an employee agrees to a reduction in their salary that is equal to, for example, their pension contribution.

Employers must deduct the appropriate amount from employees’ salaries and ensure timely submission to the tax authorities. These contributions fund health care, pensions, and other social benefits. Income Tax: Peru operates on a progressive income tax system, with different tax rates for various income brackets.

Self-service capabilities that enable employees to view and download payroll checks online on mobile devices and computers and to change deduction amounts. RTI and pensions auto enrolment enabled. Direct pay cheque deposits. Generated tax forms. Suite of reports. The key benefits of payroll software.

A payslip contains important information, including someone’s payroll number, gross income (the income before any taxes and deductions have been taken out) and net pay (what’s left after deductions have been taken off), and usually a tax code.

We’re doing a lot for our student employees in terms of cost-of-living benefits, including opening up [the] Isa for pensions contributions for them. The schemes helped employees learn how to manage their money better and some to save thousands of pounds through the Isa by utilising employer contributions.

Payroll administration is the difficult task of keeping track of your employees’ financial data, such as pay, benefits, taxes, and deductions. Payroll software calculates pay and deductions precisely, and you only have to enter employee information once. Employer costs also exist, but non-Polish employers may be unaware of this.

million lost working hours (Money & Pensions Service). Our Financial Wellbeing App is so much more than a money management tool, consolidating an employee’s debt into one loan, repayable to your business via manageable monthly salary deductions. Financial anxiety – money worries – cost the UK economy £120bn and 17.5

The benefits offered by Together Housing Group: Pension. Local government pension schemes (LGPS) with varying employer contribution levels. Employee pays for discounted health screening on salary exchange basis via monthly deductions. Defined benefit (DB) scheme. Employer-paid at base level for employee and dependants.

Pension and retirement plans The same Forbes Advisor study found that 34% of employees and 34% of employers agree that retirement plans are a vital part of a company’s benefits strategy. Retirement plans are tax deductible, flexible and are a great way to attract new talent to your business.

The benefits on offer at Egress: Pensions Defined contribution pension scheme, with 5% employee contributions and 4% employer contributions. Employees have the option to add cover for a partner or dependents through salary deductions. Employees have the option to add cover for a partner or dependents through salary deductions.

The definitive A-Z of payroll outsourcing in the UK A | B | C | D | E | F | G | H | I | J | K | L | M | N | O | P | Q | R | S | T | U | V | W | X | Y | Z | A: Auto-enrolment The process through which qualifying employees are automatically entered into workplace pension schemes. This is typically calculated through payroll software.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content