This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

“I don’t really care about my employeebenefits,” said no employee ever. When it comes to employeebenefits, if your business can offer it, employees want it. That’s the case for any employeebenefit, from time off to healthcare to flexible work arrangements to workers’ comp insurance.

EmployeeBenefits poll: Approximately half (49%) of organisations think the pots-for-life plan will increase employees’ engagement with their pensions, according to a survey of EmployeeBenefits readers. Employees would also be able to choose their own pension scheme for automatic-enrolment.

appeared first on EmployeeBenefits. Image credit: photocosmos1 / Shutterstock.com Chancellor of the Exchequer, Jeremy Hunt (pictured), delivered his Spring Budget speech in the House of Commons on Wednesday 6 March.

More employers could introduce gender inclusive paid parental leave to prevent and try to close gender pension gaps. The Pensions (Extension of Automatic-Enrolment) (No. 2) Bill will remove the lower earnings limit, enabling more employees to pay into a pension. The Pensions (Extension of Automatic-Enrolment) (No.

Nearly half (46%) of UK employers with defined contribution (DC) pension schemes say that delivering positive outcomes for members in this scheme is now their top priority, according to research by global professional services firm Aon.

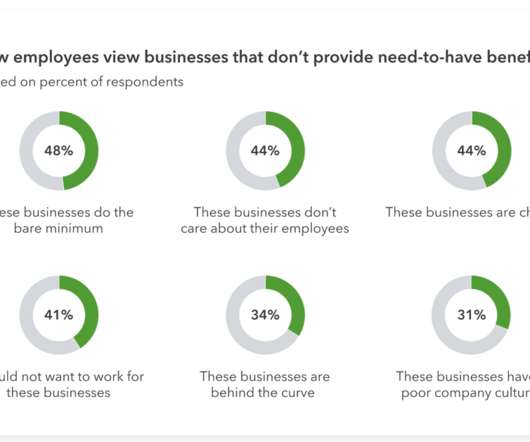

This alarming statistic signals a pressing need for businesses to reevaluate their benefits offerings. Furthermore, research shows that 73% of employees are significantly more likely to remain with an employer that provides a comprehensive benefits package. What are employeebenefits providers?

Need to know: Employers can tailor content and communication channels to different employee groups to help with their pensions knowledge. Losing the jargon will make the language of pensions easier to understand and more relevant to staff. Workplace pensions are one of the most valuable elements of the benefits package.

EmployeeBenefits poll: Just one-third (33%) of organisations think the pension pot for life plans announced in November’s Autumn Statement by Chancellor Jeremy Hunt will help employees to manage their pension, according to a survey of EmployeeBenefits readers.

New research has found the gender pension gap between men and women’s contributions is 35% for employees aged between 50 and 54, almost double the gap for 35 to 39 year-olds (18%). Due to auto-enrolment (AE) thresholds, an employee earning £30,000 who opts to reduce their hours by 40% would see their pay reduce by 40%.

What is a group personal pension (GPP)? A group personal pension is a defined contribution (DC) arrangement whereby an employer agrees to make monthly contributions into a scheme, but the contract is between the employer and the pension provider. The income is taxable. They can choose to do a combination of these.

Auto Enrolment Pension Staging Date: A Guide for Employers Whether you’re exploring the possibility of establishing a new auto enrolment pension for your company, or if you’ve already got one in operation pension auto enrolment staging dates might puzzle you. Why does auto enrolment for pensions matter?

About 1,000 Unite union members working at two Morrisons warehouses have undertaken strike action for three days over a cut in company contributions to their pensions. She said: “Unite will not stand for such behaviour from any employer, let alone one like Morrisons which is raking in massive profits in the midst of a cost-of-living crisis.

While automatic-enrolment has resulted in more individuals saving for retirement, it has created a separate issue that the Department for Work and Pensions (DWP) describes as ‘the proliferation of small pots’: the creation of multiple deferred pension pots , often low in value, when employees change employer.

Workplace savings fintech firm Cushon has acquired financial services business Creative’s workplace pension scheme. This is Cushon’s third workplace pension acquisition in two years, in line with regulatory goals to drive further consolidation in the market.

New research has revealed that 82% of young employees aged between 18 and 22 believe that individuals in employment should start saving for their pensions and retirement before the current default age of 22. The post 82% of young staff want to save for pensions before turning 22 appeared first on EmployeeBenefits.

One effective way in which employers can help drive employee engagement with pensions is by ensuring ease of access, so they can engage more easily and more regularly. In order to minimise jargon surrounding pensions, communication strategies should be easy to understand, inspiring, engaging and informing.

lost pension pots in the UK, worth around £26.6 billion WEALTH at work explains how employees can track down lost pensions and provides guidance on whether to consolidate The total value of lost pension pots has grown from £19.4 find-pension-contact-details). find-pension-contact-details). billion in 2022.

Newcastle Building Society has received living pensionemployer accreditation from the Living Wage Foundation. Through auto-enrolment, employers must contribute at least 3% and employees pay 5%. Existing employees will be advised on how to increase their contribution in line with the standard if they wish to do so.

Global technology organisation Siemens, which employs approximately 7,000 employes in the UK, believes it is important for its younger employees to understand that pension saving is most effective when they start early on. “We also use our internal social platform Yammer to promote pension messages within Siemens.”

Choosing a pension provider that offers easily accessible and age appropriate investment education can increase employees’ confidence on the topic. Investment fund choices for employees with specific needs or beliefs ensure wider needs are met. Internal surveys can provide an insight into what they know and would like to learn.

When law firm Herbert Smith Freehills was approached about taking part in the living pension pilot, it was keen to support what it saw as a vital initiative not just for its own employees, but for society in general. The living pension voluntary savings target is 12% of a worker’s annual salary.

Given cost of living worries and the notion this may be impacting pension savings, WEALTH at work conducted research* with employees to find out their thoughts into what’s happening in reality. It’s therefore more important than ever to ensure employees are engaged with their pensions.

Need to know: Change will happen when it comes to employers’ pensions plans. An employer should really get to know the audience of employees and meet them where they are. In many situations, it is good news for employees. Employees will appreciate honesty, he adds. Being upfront about bad news is vital.

A quarter (26%) of large employers have seen an increase in the number of pension scheme opt-outs among employees in the face of the cost-of-living crisis , according to research by Cushon. The majority (84%) of those with a workplace pension agreed that increased financial education around pensions would be helpful.

BBC v Christina Burns concerns the ability of employers to amend their old-fashioned and prohibitively expensive defined benefitpension schemes to make cost-saving changes. Often this is done by closing a scheme to future accrual, so members no longer earn any further benefits in it.

Private medical insurance (PMI) has become the most important perk that employees look for in their benefits package, according to new research by Zest. They also ranked PMI ahead of benefits that could help them with the cost-of-living crisis, such as employer support for home energy costs (25%) and workplace savings schemes (21%).

Higher pay rises for men than women could result in a gender pensions gap of £142,603, according to new findings. Using assumed workplace pension contributions of 8% of an employees’ salary, this disparity could leave men with £142,603 more in their pension pots than women.

Flexible Work Arrangements A healthy work-life balance is crucial for both employers and employees. A shift from the traditional 9-to-5 work routine to a more flexible work model enhances employee morale and productivity. The cost for employers to enable remote work is usually a provision of up to £30 per employee.

As a voluntary savings target, the living pension initiative sets out the minimum annual contribution needed to afford basic living costs in retirement. Employers should ensure that employees who increase their contributions in line with this are not saving at a rate they cannot afford. Enter the living pension initiative.

WEALTH at work, a leading financial wellbeing and retirement specialist has run financial education workshops for staff in hundreds of organisations and is encouraging people to consider using this saving in National Insurance if they can, to increase their monthly pension contributions. When made into a pension contribution it is worth £206.39

In its blog published 4 November, AE has come a long way, but we all have further to go, the Pensions Regulator (TPR) recognises the successes of automatic-enrolment in encouraging retirement saving. It also acknowledges that it could do more to enforce employer compliance with AE obligations. appeared first on EmployeeBenefits.

With interest rates on the rise, we often get asked at our financial education sessions, is it best to pay off your mortgage or pay into your pension? He concludes, “Many employers offer financial education in the workplace, to help their staff to understand their finances so they are better prepared to make decisions like these.”

When Ford Motor Company moved to a master trust in April 2022, explaining the changes to people at pensions roadshows was a priority. Oliver Payne, international pensions and data analytics manager at Ford and founder of the Reinventing Pensions event, explains: “The reason for that is you get people’s focused attention.

Transitioning to a superior provider is no longer a hassle: If you’re contemplating changing your current workplace pension scheme, the process isn’t as challenging as you might think. Many pension companies (we’re one of them!) What is a workplace pension? are prepared to assist you with the heavy lifting.

The Department of Work and Pensions (DWP) has reported a mean gender pay gap for 2022 of 5.9%. Awareness and support of those with caring responsibilities is embedded into all our HR policies and our commitment to this is strengthened by DWP’s membership to the Employers for Carers forum. “We

Aptia clients now have the added benefit of improving benefits education and engagement with Flimps robust digital benefits campaigns and white-glove, consultative approach. Our expertise in benefits communication campaigns runs deep and can make a fast and meaningful impact for employers and their employees.

Need to know: The Department for Work and Pensions announced a delay to the delivery of the pensions dashboard programme in March 2023. Employers should use this additional time to make sure they have their data up-to-date, in order and correct. What do employers need to do? Who will oversee the dashboards?

Pension scheme members may get a similar feeling if their scheme has a mandatory forfeiture rule and the trustees inform them their pension is less than it should have been. It is clear from recent cases that these rules will be effective to deprive members of benefits. Requesting your full pension when you retire is not enough.

billion pension to cut future benefits for plan members but can make other changes without employees’ consent. The case explored the treatment of future service benefits under the BBC pension scheme, which provides retirement benefits on a defined benefit (DB) basis for BBC employees who joined before 1 December 2010.

In a defined benefit plan, an employer pays a predetermined amount at either termination of employment or retirement. The employer breaks the sum into annual payments, which they deposit as savings to provide the benefits prescribed by the program’s terms. SOP – Employee stock ownership plans.

Health provider Novus Health has received living pensionemployer accreditation from the Living Wage Foundation. The employer delivers free audiology, physiotherapy and dermatology services on behalf of the NHS. The employer pays in at least 7%, or £1,630.

In our newest report, ‘Zooming in on Gen Z’, we compiled our findings from ‘ The Benefits Factor ’ to discover what Gen Z expects from employers. Here, we’re sharing the five benefits your organisation must provide to become a Gen Z magnet. H2; Gen Z in the Workplace — What Do They Want? out of 10 in importance for Gen Z.

Credt: P Maxwell Photography/Shutterstock The pension pots-for-life plan take the onus off of employees to keep track of their pensions as they move jobs. Clarification is needed on how employers would manage the process of putting employees’ contributions into many different pension pots. Opinions differ.

Almost half UK employers have been touting statutory requirements or basic rights as workplace benefits in their job adverts, according to a new analysis by Rippl. The employeebenefits platform looked at employers’ recruitment advertising on the largest job listing sites. Free fruit appeared 675 times.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content