This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Reports suggest that by November 27, 2024, the Disney Aspire in-network schools will enforce a funding cap of $5,250 on the educational assistance provided to an individual employee. This cap is the same as the IRS limit on tax-free benefits for educational assistance programs and is commonly followed by many organizations.

Q: We have an employee who wants to make changes to her cafeteria plan election, even though benefits are already effective. Employers: Don’t make this common cafeteria plan mistake! It can even jeopardize the tax-favored status of the entire plan. An employee changing his or her mind does not count.

PPO deductible Nearly two-thirds of large employers provide their employees with the choice of an HDHP and a traditional health plan , such as a preferred provider organization (PPO). Typically, an employeeenrolled in a PPO will have higher premiums and a lower deductible than an employeeenrolled in an HDHP.

If you have staff with health savings accounts, they still have until April 15 to make additional contributions to their accounts if they want to reduce their tax bills for last year. HSAs allow your employees to put away funds to pay for future medical expenses. Withdrawals to reimburse for these expenses are also not taxed.

Earlier this year the IRS announced proposed regulations extending ACA affordability to other tiers of employer-sponsored group medical coverage (employee + child/spouse, family, etc.). Previously, ACA affordability was based solely on the employee-only tier of coverage. EMPLOYERS ARE NOT EXPOSED TO NEW PENALTY RISKS.

Nearly two-thirds of large employers offer their employees a choice between an HSA-eligible health plan (also known as a high-deductible health plan ) and a traditional health plan. Smaller employers may face challenges in providing these options, although participants have said they are interested in these health plan choices. “I

With more than half of all private sector employeesenrolled in high-deductible health plans , it’s important that employers have in place certain protocols to ensure that they are a success. HSAs are tax-advantaged accounts that allow enrollees to save up to pay qualified medical expenses.

The Internal Revenue Code (the “Code”) requires insurance companies, self-insured plans, and applicable large employers (“ALEs,” generally those with 50+ full-time or full-time equivalent employees) to file annual statements with the IRS (via Forms 1094-B and 1094-C for insurance providers and ALEs, respectively).

FSAs are primarily funded by employees through pretax deductions, although employers may make contributions. Tax advantage: Employees’ and employers’ contributions are excluded from employees’ wages and aren’t subject to income or FICA taxes. Employees usually contribute to HSAs on a pretax basis.

There are a number of issues that Medicare-eligible workers face that your human resources staff may be asked about, such as: Penalties for late Medicare enrollment, Whether the employer plan is the primary or secondary payer of claims, and. The following are considerations for employers faced with workers nearing 65.

This includes employees’ work benefits, particularly pre-tax accounts. For employees with an HSA, Dependent Care FSA, and/or commuter plan, there may be the opportunity to make changes to their accounts. Here are the main updates employees should know about. Especially compared to other pre-tax accounts, like FSAs.

As we enter 2022, there are a number of changes on the horizon that plan sponsors need to be aware of as they will affect group health plans as well as employeesenrolled in those plans. These rules were all not mandatory and employers could choose whether to relax them or not.

A 401(k) plan is a type of retirement account offered by employers to their employees. It allows employees to save a portion of their pre-tax income for retirement. The contributions are deducted from the employee’s paycheck before taxes are withheld, which reduces their taxable income.

With more than half of all private sector employeesenrolled in high-deductible health plans , it’s important that employers have in place certain protocols to ensure that they are a success. HSAs are tax-advantaged accounts that allow enrollees to save up to pay qualified medical expenses.

Open enrollment is underway for many companies right now and one benefits offering that may be on the menu this year is an FSA. Employers are constantly looking for ways to remain competitive in their benefits offerings, and an FSA is a great add-on to your benefits package. Employers can choose one, but not both of these options.

Similarly, when it comes to Open Enrollment, there are two big questions to ask: What method or platform are your employees using to enroll? The way your employeesenroll will influence how that information is sent to your TPA. This approach is great for employers who want to offer the analog option.

” Although rising premium rates are an on-going challenge for employers, a primary (and popular) method to overcome this is to implement a high-deductible health plan (HDHP). Overcoming the Challenge Implement an HDHP with Complementary Accounts A growing number of employers have implemented an HDHP as a choice for employees.

According to a recent article from SHRM covering research from the Employees Benefit Research Institute (EBRI), enrollment in an HDHP promotes more conscious health care purchase decisions. For example, 55% of employeesenrolled in an HDHP checked whether their health plan would cover their care or medication.

Many receive this coverage as a benefit of their employment. Employers who do not offer coverage can have a more difficult time attracting recruits and retaining employees. All members contribute to the plan, as well as the employer, to help reduce health care costs for every member. Read on for a thorough overview.

For example: In an individual coverage health reimbursement arrangement, the health reimbursement arrangement is offered in place of a group health plan, allowing employees to purchase a health plan on their own. Healthcare.gov says that employees must be enrolled in individual health plans, such as a Marketplace plan, to use the funds.

Flexible spending accounts (FSAs) are employer-established accounts that allow you to put aside pre-tax dollars from your paycheck into a special account to be used for eligible health or dependent care expenses. The card is issued by the benefits provider that the employer has chosen to work with for the FSA.

High deductible health plans (HDHPs) are on the rise as a growing number of employers turn to consumer-directed health plans to try to curb costs—the portion of employeesenrolled in HDHPs rose from 26.3% In addition, employers can contribute tax-free dollars if they choose—all of which is employee money.

Many have started the process of commuting after COVID-19, leaving employees and employers alike wondering how the transition will unfold. Only available to individuals enrolled in a tax free parking account with BRI. ** Only available to employeesenrolled in a tax free mass transit or parking account with BRI.

Often these programs are funded by the company and also the employee gets an incentive for joining the course. Continuous learning is beneficial for the employer as well as the workforce. Enhanced productivity and improved performance (for the employer). Tax benefits and other perks. The need for continuous learning.

But it was only days ago, November 14, 2019 to be exact, that employers became at risk to pay penalties. Under the Sustainable DC Act of 2014, employers with more than 20 employees (including full and part-time employees) will be required to provide one of three commuter benefit options, including: Employee-paid pre-tax benefit.

Assessing open enrollment and employees’ overall involvement in benefit offerings should be a big part of any year-end HR checklist. Obviously you and the providers you select for your benefit offerings need to know how many employeesenroll in each plan. According to attorney Robert Y. Payroll compliance checks.

The proposed regulations would now make permanent and automatic the 30-day extension for Forms 1095-B and 1095-C – employers and insurance providers would not be required to demonstrate good cause. Thus, ALEs will still have to furnish the applicable forms to full-time employees in the traditional manner.

However, it highlights the need to use multiple communication channels – especially when it comes to Open Enrollment. We conducted a survey earlier this year to evaluate how employers planned to communicate during Open Enrollment. Most employers have access to these communication methods already, so there’s no additional cost.

Their tax advantages and investment potential can help employees reduce healthcare costs, save for retirement, and maximize tax refunds. And yet, that’s not how most employees understand them — if they understand them at all. In short, your employees are missing out, and so is your organization.

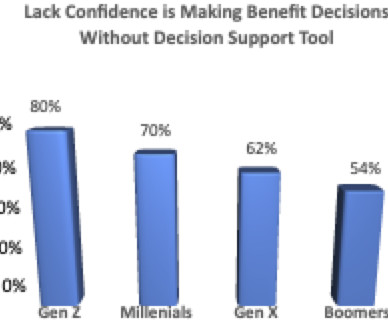

A 2022 Harris poll found that 72% of employees said “they wish someone would tell them what the best health insurance for their unique situation is.” AI Enabled Benefits Education According to a recent study by the Hartford, “76% of employers say educating employees about benefits” remains challenging.

The pandemic has given employers a lot to think about. While many companies may be ready to move quickly back to a fully on-site workforce, and others are exploring hybrid or fully remote options, employees have their own expectations and are willing to look for a new position if they aren’t met. Almost three-fourths of U.S.

By opting for a higher deductible, employees can secure lower monthly premiums. Let’s say an employeeenrolls in a high-deductible health plan providing self-only coverage with an annual deductible of $2,000. Employers, employees or both can contribute funds to an HSA in the same year.

One of the most difficult aspects of annual open enrollment is reaching workers who are disengaged from the process and never bother signing up for your group health plan and other benefits they could take advantage of. Young workers will often forgo their employer’s health plan as they are still covered by their parents’ plans.

In an effort to make 401(K) plans more attainable for small business owners, the new legislation offers businesses with up to 100 employees a tax credit equating to $250 for each non-highly compensated employee eligible for plan participation or $5,000, whichever is less. This bill has you covered!

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content