This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you have staff with health savings accounts, they still have until April 15 to make additional contributions to their accounts if they want to reduce their tax bills for last year. HSAs allow your employees to put away funds to pay for future medical expenses. Withdrawals to reimburse for these expenses are also not taxed.

With GoCo, employees have access to a comprehensive benefits marketplace where they can compare plans and select the best options for their individual needs. The platform also offers a flexible spending account (FSA) option, allowing employees to set aside pre-tax dollars for eligible medical and dependent care expenses.

PPO deductible Nearly two-thirds of large employers provide their employees with the choice of an HDHP and a traditional health plan , such as a preferred provider organization (PPO). Typically, an employeeenrolled in a PPO will have higher premiums and a lower deductible than an employeeenrolled in an HDHP.

With more than half of all private sector employeesenrolled in high-deductible health plans , it’s important that employers have in place certain protocols to ensure that they are a success. HSAs are tax-advantaged accounts that allow enrollees to save up to pay qualified medical expenses.

Earlier this year the IRS announced proposed regulations extending ACA affordability to other tiers of employer-sponsored group medical coverage (employee + child/spouse, family, etc.). Previously, ACA affordability was based solely on the employee-only tier of coverage. Today the IRS released final regulations.

With more than half of all private sector employeesenrolled in high-deductible health plans , it’s important that employers have in place certain protocols to ensure that they are a success. HSAs are tax-advantaged accounts that allow enrollees to save up to pay qualified medical expenses.

Flexible Spending Accounts allow employees to set aside pre-tax dollars from their paycheck to use for medical or dependent care expenses. These funds are placed in an FSA account that employees can use to pay for eligible expenses. The maximum that an employee may contribute to a healthcare FSA is $2,750.

This includes employees’ work benefits, particularly pre-tax accounts. For employees with an HSA, Dependent Care FSA, and/or commuter plan, there may be the opportunity to make changes to their accounts. Changes to Medical FSAs are currently not permitted). Here are the main updates employees should know about.

FSAs are primarily funded by employees through pretax deductions, although employers may make contributions. Tax advantage: Employees’ and employers’ contributions are excluded from employees’ wages and aren’t subject to income or FICA taxes. Eligibility: FSAs are generally available only to current employees.

In the simplest terms, a medical expense reimbursement plan refunds employees for covered medical costs. For example: In an individual coverage health reimbursement arrangement, the health reimbursement arrangement is offered in place of a group health plan, allowing employees to purchase a health plan on their own.

Flexible spending accounts (FSAs) are employer-established accounts that allow you to put aside pre-tax dollars from your paycheck into a special account to be used for eligible health or dependent care expenses. This means that employees do not have to wait to use their health FSA funds. The patient does not have to be the employee.

According to a recent article from SHRM covering research from the Employees Benefit Research Institute (EBRI), enrollment in an HDHP promotes more conscious health care purchase decisions. For example, 55% of employeesenrolled in an HDHP checked whether their health plan would cover their care or medication.

Without insurance coverage, it can be difficult to pay for medical expenses, whether or not they are expected. Employers who do not offer coverage can have a more difficult time attracting recruits and retaining employees. Group health insurance may cover a range of health care needs, including medical, vision or dental.

High deductible health plans (HDHPs) are on the rise as a growing number of employers turn to consumer-directed health plans to try to curb costs—the portion of employeesenrolled in HDHPs rose from 26.3% In addition, employers can contribute tax-free dollars if they choose—all of which is employee money.

An ounce of prevention may be worth a pound of cure, but up until this point, high-deductible health plans have been boxed in regarding tax-free reimbursements for most preventive care services or items. Reason: With certain exceptions, HDHPs can’t start reimbursing employees until they meet those high deductibles.

Their tax advantages and investment potential can help employees reduce healthcare costs, save for retirement, and maximize tax refunds. And yet, that’s not how most employees understand them — if they understand them at all. In short, your employees are missing out, and so is your organization.

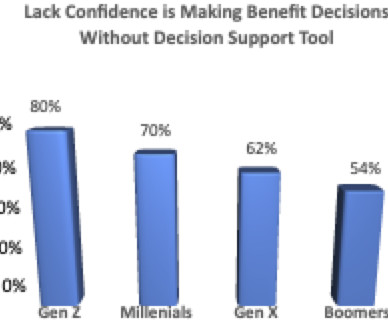

A 2022 Harris poll found that 72% of employees said “they wish someone would tell them what the best health insurance for their unique situation is.” However, the way in which employees comprehend benefit information varies greatly based on their current stage in life. Be mindful that not all decision support tools are created equal.

By opting for a higher deductible, employees can secure lower monthly premiums. Let’s say an employeeenrolls in a high-deductible health plan providing self-only coverage with an annual deductible of $2,000. Employers, employees or both can contribute funds to an HSA in the same year.

One of the most difficult aspects of annual open enrollment is reaching workers who are disengaged from the process and never bother signing up for your group health plan and other benefits they could take advantage of. Savers — This group doesn’t touch their HSA balances, even for current medical expenses.

For dependent-care benefits, employees may change their pretax deductions if: The safety or quality of their current day care provider raises concerns. The day care provider has age cutoffs and won’t take infants, and employees don’t want to split up their kids at different providers. A day care center raises it rates.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content