This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Reports suggest that by November 27, 2024, the Disney Aspire in-network schools will enforce a funding cap of $5,250 on the educational assistance provided to an individual employee. This cap is the same as the IRS limit on tax-free benefits for educational assistance programs and is commonly followed by many organizations.

With GoCo, employees have access to a comprehensive benefits marketplace where they can compare plans and select the best options for their individual needs. The platform also offers a flexible spending account (FSA) option, allowing employees to set aside pre-tax dollars for eligible medical and dependent care expenses.

PPO deductible Nearly two-thirds of large employers provide their employees with the choice of an HDHP and a traditional health plan , such as a preferred provider organization (PPO). Typically, an employeeenrolled in a PPO will have higher premiums and a lower deductible than an employeeenrolled in an HDHP.

.” Employees cannot change their minds and make changes to pre-tax cafeteria elections during the plan year, once benefits become effective — unless a special enrollment period as defined under IRC Section 125 applies , or the employer is correcting an administrative error. This is not correct.

If you have staff with health savings accounts, they still have until April 15 to make additional contributions to their accounts if they want to reduce their tax bills for last year. HSAs allow your employees to put away funds to pay for future medical expenses. Withdrawals to reimburse for these expenses are also not taxed.

For purposes of affordability, family members only include children who are tax dependents. Unless C is still considered a tax dependent of S1 & S2, C would not be considered an eligible family member for purposes of affordability. In the final example, on the bottom row, assume C is 24 rather than 14 years of age.

Additionally, the notice must be written in plain, non-technical terms and in a large enough font size to call to a viewer’s attention that the information pertains to tax statements reporting that individuals had health coverage. The reporting entity must furnish a copy of the form within 30 days of a request.

With more than half of all private sector employeesenrolled in high-deductible health plans , it’s important that employers have in place certain protocols to ensure that they are a success. HSAs are tax-advantaged accounts that allow enrollees to save up to pay qualified medical expenses.

More dental and vision Among employers with benefits administration through WEX , 68% of eligible employeesenrolled in vision and 77% of eligible employeesenrolled in dental. However, not all employees are offered these benefits. It is not legal, financial, or tax advice.

This includes employees’ work benefits, particularly pre-tax accounts. For employees with an HSA, Dependent Care FSA, and/or commuter plan, there may be the opportunity to make changes to their accounts. Here are the main updates employees should know about. Especially compared to other pre-tax accounts, like FSAs.

If your firm has fewer than 20 employees, workers who are 65 or older can no longer contribute to an HSA as they are not compatible with Medicare. Employees who are 65 or older should stop making contributions to their HSA six months before they enroll in Medicare or before they apply for Social Security benefits if they are still working.

It allows employees to save a portion of their pre-tax income for retirement. Here’s how it works: When an employeeenrolls in a 401(k) plan, they choose a percentage of their salary to contribute to the plan, up to a certain limit set by the Internal Revenue Service (IRS). How does 401(k) work?

As we enter 2022, there are a number of changes on the horizon that plan sponsors need to be aware of as they will affect group health plans as well as employeesenrolled in those plans. Some of the changes concern temporary rules that were implemented during the COVID-19 pandemic. That’s a change from the prior threshold of 250.

With more than half of all private sector employeesenrolled in high-deductible health plans , it’s important that employers have in place certain protocols to ensure that they are a success. HSAs are tax-advantaged accounts that allow enrollees to save up to pay qualified medical expenses.

Similarly, when it comes to Open Enrollment, there are two big questions to ask: What method or platform are your employees using to enroll? The way your employeesenroll will influence how that information is sent to your TPA. How are you sending that information to your Third Party Administrator (TPA)?

Flexible Spending Accounts allow employees to set aside pre-tax dollars from their paycheck to use for medical or dependent care expenses. These funds are placed in an FSA account that employees can use to pay for eligible expenses. The maximum that an employee may contribute to a healthcare FSA is $2,750. Healthcare FSA.

FSAs are primarily funded by employees through pretax deductions, although employers may make contributions. Tax advantage: Employees’ and employers’ contributions are excluded from employees’ wages and aren’t subject to income or FICA taxes. Eligibility: FSAs are generally available only to current employees.

Employees can use two tax-advantaged accounts to cover many primary eligible expenses. If employeesenroll in a Limited FSA they have the option to forgo enrolling in vision or dental insurance, avoiding the need to pay those premiums. You also still receive a tax write off.

According to a recent article from SHRM covering research from the Employees Benefit Research Institute (EBRI), enrollment in an HDHP promotes more conscious health care purchase decisions. For example, 55% of employeesenrolled in an HDHP checked whether their health plan would cover their care or medication.

Businesses must also meet certain criteria to be able to offer group health insurance to their employees. They must have at least one full-time employee who works at least 30 hours per week, and they must pay payroll taxes. How To Enroll. The money that employers put toward group insurance premiums is tax-deductible.

Both the employee and the employer may contribute, but funds expire if they are not used within a certain period of time. The Tax Benefits of Health Reimbursement Arrangements. Employees generally do not pay taxes on health reimbursement arrangement funds used on eligible health care expenses. Manage enrollment.

Only available to individuals enrolled in a tax free parking account with BRI. ** Only available to employeesenrolled in a tax free mass transit or parking account with BRI. The post What will commuting after COVID-19 look like? appeared first on BRI | Benefit Resource.

Flexible spending accounts (FSAs) are employer-established accounts that allow you to put aside pre-tax dollars from your paycheck into a special account to be used for eligible health or dependent care expenses. The patient does not have to be the employee. Health care provider’s name. Dependent care FSA receipt requirements.

High deductible health plans (HDHPs) are on the rise as a growing number of employers turn to consumer-directed health plans to try to curb costs—the portion of employeesenrolled in HDHPs rose from 26.3% In addition, employers can contribute tax-free dollars if they choose—all of which is employee money.

Tax benefits and other perks. Companies are now sending their employees to complete their graduation and post-graduation degrees to increase their knowledge base and skills. Companies are now sending their employees to complete their graduation and post-graduation degrees to increase their knowledge base and skills.

If you plan to use the platform to communicate with employees, make sure it can host communication materials and videos. Consider enrollment windows as well. Some platforms can integrate with payroll, talent-management platforms and other systems — and even simplify tax credit applications. Customization. Integration.

Under the Sustainable DC Act of 2014, employers with more than 20 employees (including full and part-time employees) will be required to provide one of three commuter benefit options, including: Employee-paid pre-tax benefit. Explain how to enroll. Employer-paid direct benefit. Employer-provided Transportation.

Assessing open enrollment and employees’ overall involvement in benefit offerings should be a big part of any year-end HR checklist. Obviously you and the providers you select for your benefit offerings need to know how many employeesenroll in each plan. Payroll compliance checks.

This relief applies to ALEs, insurers and multiemployer plans as follows: For ALEs : applies to the requirement to provide Forms 1095-C (and/or Forms 1095-B if the coverage is self-insured), but only with respect to non-full-time employees and non-employeesenrolled in the self-insured plan.

An ounce of prevention may be worth a pound of cure, but up until this point, high-deductible health plans have been boxed in regarding tax-free reimbursements for most preventive care services or items. Reason: With certain exceptions, HDHPs can’t start reimbursing employees until they meet those high deductibles.

and so much more. That’s a LOT! Factoring in all of the time and effort it takes to handle all of the above, it makes sense for most organizations to partner with trusted third-party payroll and benefits administrators who can do the heavy lifting.

Their tax advantages and investment potential can help employees reduce healthcare costs, save for retirement, and maximize tax refunds. And yet, that’s not how most employees understand them — if they understand them at all. In short, your employees are missing out, and so is your organization.

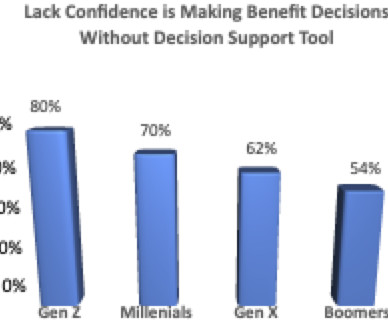

A 2022 Harris poll found that 72% of employees said “they wish someone would tell them what the best health insurance for their unique situation is.” Be mindful that not all decision support tools are created equal.

Most HRIS systems deal with tracking time and labor management (including PTO and attendance), payroll /taxes, benefits administration (and selections), employee demographic information, applicant tracking, onboarding, performance management , and more. They aim to seamlessly manage your backend people-related admin tasks.

By opting for a higher deductible, employees can secure lower monthly premiums. Let’s say an employeeenrolls in a high-deductible health plan providing self-only coverage with an annual deductible of $2,000. Employers, employees or both can contribute funds to an HSA in the same year.

One of the most difficult aspects of annual open enrollment is reaching workers who are disengaged from the process and never bother signing up for your group health plan and other benefits they could take advantage of. These accounts can be kept for life and transferred to new employers.

For dependent-care benefits, employees may change their pretax deductions if: The safety or quality of their current day care provider raises concerns. The day care provider has age cutoffs and won’t take infants, and employees don’t want to split up their kids at different providers. A day care center raises it rates.

In an effort to make 401(K) plans more attainable for small business owners, the new legislation offers businesses with up to 100 employees a tax credit equating to $250 for each non-highly compensated employee eligible for plan participation or $5,000, whichever is less. This bill has you covered!

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content