This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As an employer, you are responsible for withholding various taxes from employees’ wages. After you subtract all of the taxes and other deductions, money left over is considered take-homepay. Read on to learn more about what is take-homepay and how to calculate it. What is takehomepay?

As an employer, you are responsible for withholding various taxes from employees’ wages. After you subtract all of the taxes and other deductions, money left over is considered take-homepay. Read on to learn more about what is take-homepay and how to calculate it. What is takehomepay?

Because these benefits are free from federal and state income taxes, an employee’s taxable income is reduced, which increases the percentage of their take-homepay. The plans benefit employers, as well. A cafeteria plan can save employers an average of almost $115 per participant in FICA payroll taxes.

The Covid-19 pandemic and cost-of-living crisis have changed which benefits employees value the most and what employers offer. Organisations that balance their own needs with those of their employees are likely to succeed in attracting and retaining talent as an employer of choice. But what does this mean in today’s labour market?

Many employers find it challenging to provide a budget-friendly and attractive benefits package. Employers wanting to compete for top talent can offer section 125 plans as a fringe benefit to help attract and retain employees. Check out our complete guide to fringe benefits to learn more about various employee benefits.

Most employers handle direct deposit through their payroll software. Payroll services calculate employees’ wages, taxes and deductions, and take-homepay. […] Read More Direct deposit is a convenient payment method for employees, who receive their paycheck quickly and securely on payday.

It is available from day one of employment for permanent staff and is cost-free due to the tax benefit being paid on their behalf, so as to not impact their take-homepay. We are proud to be an employer of choice and want people to come and grow their careers with Bupa.

She said: “Unite will not stand for such behaviour from any employer, let alone one like Morrisons which is raking in massive profits in the midst of a cost-of-living crisis. Its flagrant profiteering and then cutting our members’ take-homepay is a disgrace.”

While the margin of increase in the new wage rates in Ontario is minimal, when calculated over a period of time, it should make a difference to the take-homepay for workers. Those who earn minimum wage and work 40 hours a week will see their annual pay increase by up to $835 shortly. in the province.

Flexible spending accounts (FSAs) are a powerful tool for individuals and employers to save money on healthcare and dependent care expenses. Some individuals may be wary of reducing their take-homepay, especially if they are already on a tight budget. So why are many employees reluctant to participate in FSAs?

Rising costs are changing the employment landscape, and workers are taking steps to improve their financial standing by trimming their expenses, increasing their income, or both. In efforts to increase their take-homepay, 77 percent of employees see the opportunity to work overtime or extra shifts.

Employers fund these flexible benefit plans with funds that are deducted from their employees’ salaries on a pre-tax basis. Besides the fact that your employees use money that hasn’t been taxed to pay for these benefits, the payroll deductions for them also reduce their taxable income while raising take-homepay.

Economists define human capital as all of the knowledge, skills, experiences, and other personal qualities that people have to “sell” to potential employers. Below are five examples: ¨ Maintain a Low Debt-to-Income Ratio- Keep monthly consumer debt payments (all debts except a mortgage) at 15% or less of monthly take-homepay.

Software can allow employees to model the impact on their take-homepay of opting into certain benefits, for example, or changing their pension contribution. Employers] get more buy-in and loyalty from employees,” Fowler says. Overall, however, Shah believes the time is right for many employers to make the switch.

This, for example, means an individual earning £30,000, with a net takehomepay of £23,112, will see this take-home figure decrease by £255. . It is crucial to build healthy financial habits that will help minimise the impact once the NI hike takes place this year. Hunt down lost pension pots.

This is especially true when an employer matches any additional contributions. For example, someone in their 20s, saving an extra 1% a year with their employer matching this, may be able to increase their pension pot in retirement by 25%. 2025 UK adults aged 22+ in full time employment were surveyed.

The frozen tax thresholds could see some employees ‘dragged’ into paying more tax and have less disposable income as a result. Employers should ask employees about their financial pressures to understand how to support them. In order to combat this, how can employers help manage employees’ financial pressures ?

As employers gradually get back to business as usual, many employees are searching for a new normal. Many hourly workers toiled long hours and endured health risks for low take-homepay. Employers must increase their hourly wages to attract and retain workers. . Continue work from home options.

Need to know: Enriching benefits data with information from other sources can help employers create personalised benefit offerings. Low take-up rates do not always indicate a benefit is not popular: it may need an awareness or education campaign to boost engagement. Several different types of benefit technology are available.

It depends on how your employer will manage this unusual year. Some employers may choose to divide employees’ annual salary over 27 pay periods instead of 26. This means that gross pay would be 3.7% lower each pay period during 2020 (although you’d make the same total salary).

For its latest Labour market outlook report , the professional body for HR and people development surveyed 2,032 UK employers about their pay, hiring and redundancy intentions. Among public sector employer respondents, median basic pay increase expectations dropped from 3% to 2.5%.

The Covid-19 pandemic and cost-of-living crisis have changed what benefits employees value the most and what employers offer. With the right approach, employers can build a supportive and inclusive work environment in both a hybrid setting as well as a formal workplace. But what does this mean in today’s labour market?

pay rise offer following ongoing negotiations. We are pleased to have successfully negotiated a significant boost to our members’ take-homepay.” Pat McIlvogue, industrial officer at Unite, said: “The Scotrail pay offer is a credible one. More than 300 workers employed by ScotRail have accepted a 4.5%

Management consultancy Eyekon Services has been ordered to pay a former employee £8,980 after an employment tribunal found him to have been unfairly dismissed. hours per week with a takehomepay of £1,363. Employment judge D Hoey said in the ruling: “His dismissal was unfair. Rodgers worked 37.5

At its core, a workplace pension is a retirement savings plan organised by an employer for the benefit of their employees, who also contribute to the pension. As of 2012, the introduction of auto-enrolment mandates all employers to provide a workplace pension. Net Pay contributions from your employees is deducted before tax.

The retailer has additionally increased minimum pay rates , which will rise to £11.50 Over the past three years, Currys has increased its minimum hourly pay by 29%. This increase in take-homepay will mean that the annual earnings of an employee who works 20 hours a week will have risen by nearly £2,700 over the three-year period.

This means people can earn £12,500 tax-free, and only start paying tax on income over that amount. However, if they have any other form of income, get benefits-in-kind from their employer (health insurance, life insurance or a company vehicle etc) or claim tax relief for any other reason, it will affect this tax code. Pension payments.

Almost a third (29%) of UK deskless workers said they have borrowed money from family and friends to pay bills, resulting in an employee experience overshadowed by financial stresses.

Inflation doesn’t just mean rising costs for workers and their employers; UK organisations could soon be faced with workforces that are unengaged, distracted and unhappy because of the state of their finances. However, employees may be able to minimise these losses by paying for some items before they are taxed. Salary sacrifice.

Credit: Hyejin Kang/Shutterstock Need to know: Employers should start planning now for the P11D changes to the reporting and paying of tax and Class 1A national insurance contributions (NICs) on benefits in kind, to ensure a smooth transition to the new system in April 2026. There may be some challenges for employers.

The method tends to overcompensate higher wage earners and under-compensate lower wage earners relative to their usual weekly take-homepay primarily because what you takehome is ultimately mediated by deductions from your gross pay for income taxes, social security and unemployment insurance.

Health Savings Accounts allow employees (and employers) to contribute to a tax-free account to be used for eligible medical expenses. Flexible Spending Accounts are designed to provide employees with an opportunity to set aside funds on a pre-tax basis to pay for eligible out-of-pocket medical expenses. What is an HSA?

This rule will apply to employers who have started retirement plans after December 29, 2022, and take effect for plan years starting in 2025. There is an exception for new companies in business for less than three years, employers with 10 or fewer employees, and governmental and church plans. The SECURE Act 2.0

With thirty million people employed by businesses in the UK, that is a huge number of employees who could benefit if employers acted now to support them and their wellbeing. Employers need to ensure that their employees are not facing these struggles alone. Employers need to clearly communicate what support is available.

Her employment provides 42 weeks of work most years. While she and her employer might expect workers’ compensation to fully cover her earnings, what she will actually receive to cover her earnings loss depends greatly on where she lives. of her average Net earnings—about $31 less per week than her average takehomepay.

As an employer, you’re obliged to provide your staff with a workplace pension – a mandate made compulsory by the UK government in 2012. The required minimum contribution is set at 8%, typically comprising of a 3% contribution by the employer and a 5% contribution by the employee.

In the ever-evolving world of employment, organizations are increasingly focusing on enhancing employee satisfaction and well-being. tax free benefits are those that provide financial advantages for both employees and employers by avoiding certain taxes and deductions. Tax savings for employers.

A POP Plan gives employees the chance to set aside pre-tax money from their paycheck (like an FSA) but it pays for the premium costs associated with employer-provided health insurance. It is not uncommon for an employer to offer a POP Plan and a Flexible Spending Account to employees at the same time. Dependent Care Account.

Few enter the military for the pay. While the benefits are good, the take-homepay is generally lower than most entry-level positions. In the military, it’s ongoing. The culture of continued learning has been instilled in them. People join the military for a lot of reasons, and all show ambition: To serve their country.

A POP Plan gives employees the chance to set aside pre-tax money from their paycheck (like an FSA) but it pays for the premium costs associated with employer-provided health insurance. It is not uncommon for an employer to offer a POP Plan and a Flexible Spending Account to employees at the same time. Dependent Care Account.

By asking employees to lower their gross income (for example, by the percentage they contribute to their pension), and committing to contribute the difference directly into their pension, employees can actually increase their take-homepay. This happens because lower earnings mean less NI to pay.

However, unlike other generations, they can very much look beyond their takehomepay in terms of assigning value to their role. Generational Trait: Deep pockets How you can leverage it: As with just about any generation, millennials are certainly motivated by money. Instead, millennials are attracted to company perks.

Some employers send out surveys to their employees to get more insight on what they want included in the company’s health care plan. Employees aren’t going to opt in to a medical plan that cuts far into their take-homepay. To make sure you’re headed in the right direction, talk to your employees.

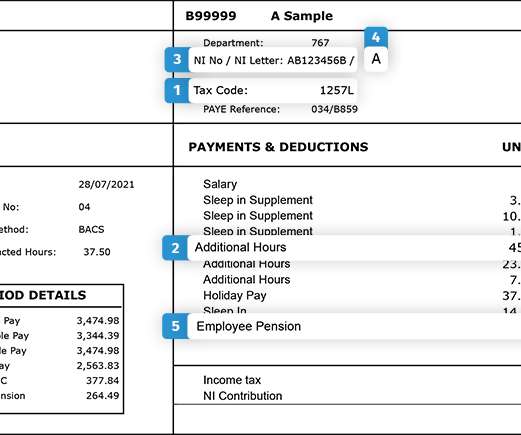

That said, while the onus is on employers to pay their employees correctly, there is still some responsibility on employees to check that their details are correct from month to month. And, if they don’t fully understand exactly what they are looking for, then they should speak to their line manager in the first instance.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content