This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As an employer, you are responsible for withholding various taxes from employees’ wages. After you subtract all of the taxes and other deductions, money left over is considered take-homepay. Read on to learn more about what is take-homepay and how to calculate it.

As an employer, you are responsible for withholding various taxes from employees’ wages. After you subtract all of the taxes and other deductions, money left over is considered take-homepay. Read on to learn more about what is take-homepay and how to calculate it. Wage garnishments.

As health care costs continue rising and employees are being asked to shoulder more of the expense burden, you can help them by offering a tax-advantaged plan that allows them to save for medical expenses. Employees can save an average of 30% in federal, state and local taxes on items they already pay for out of pocket.

Their tax advantages and investment potential can help employees reduce healthcare costs, save for retirement, and maximize tax refunds. About half of American employers offer HSAs — coupled with high-deductible health plans (HDHPs) — but, according to one study , 69% of employees don’t understand their benefits or uses.

Many employers find it challenging to provide a budget-friendly and attractive benefits package. Although benefits costs are impacted by factors like healthcare costs, which are continually rising , a section 125 plan, or cafeteria plan, allows you to boost your employee benefits while staying in-budget with its significant tax savings.

Most employers handle direct deposit through their payroll software. Payroll services calculate employees’ wages, taxes and deductions, and take-homepay. […] Read More Direct deposit is a convenient payment method for employees, who receive their paycheck quickly and securely on payday.

Employers fund these flexible benefit plans with funds that are deducted from their employees’ salaries on a pre-tax basis. Since the salary reductions are not received by the employee, they are not considered wages for income tax purposes. Set-up and tax implications.

It is available from day one of employment for permanent staff and is cost-free due to the tax benefit being paid on their behalf, so as to not impact their take-homepay. We are proud to be an employer of choice and want people to come and grow their careers with Bupa.

Flexible spending accounts (FSAs) are a powerful tool for individuals and employers to save money on healthcare and dependent care expenses. Some individuals may be wary of reducing their take-homepay, especially if they are already on a tight budget. It is not legal, financial, or tax advice. Download now!

The frozen tax thresholds could see some employees ‘dragged’ into paying more tax and have less disposable income as a result. Employers should ask employees about their financial pressures to understand how to support them. In order to combat this, how can employers help manage employees’ financial pressures ?

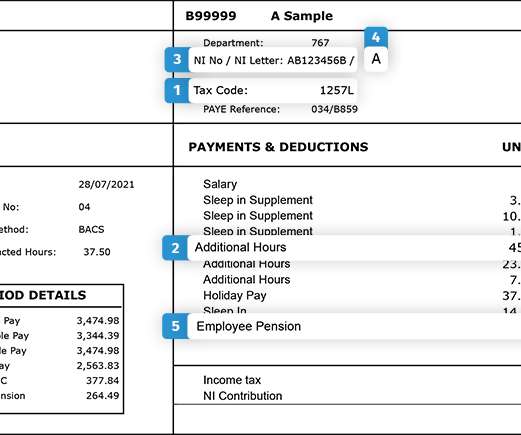

It’s worth remembering that it’s an employee’s responsibility to check they’re on the right tax code, as it impacts how much tax they pay – whether it’s too much tax or too little. For the 2021/22 tax year (and through to 2025/26), the tax code for most people under 65 who only have one job or pension is 1257L.

At its core, a workplace pension is a retirement savings plan organised by an employer for the benefit of their employees, who also contribute to the pension. As of 2012, the introduction of auto-enrolment mandates all employers to provide a workplace pension. Which Tax Relief Method is Used? What is a workplace pension?

This is especially true when an employer matches any additional contributions. For example, someone in their 20s, saving an extra 1% a year with their employer matching this, may be able to increase their pension pot in retirement by 25%. They are all 25 years old and plan to retire at age 68.

It depends on how your employer will manage this unusual year. Some employers may choose to divide employees’ annual salary over 27 pay periods instead of 26. This means that gross pay would be 3.7% lower each pay period during 2020 (although you’d make the same total salary).

Credit: Hyejin Kang/Shutterstock Need to know: Employers should start planning now for the P11D changes to the reporting and paying of tax and Class 1A national insurance contributions (NICs) on benefits in kind, to ensure a smooth transition to the new system in April 2026. There may be some challenges for employers.

noted that gross pay results in inequities—uneven results for workers due to tax factors and number of dependents, concluding “.spendable Employees inform their employers by completing an Internal Revenue Services (IRS) Form W-4. Most approaches rely on information provided by the employer. Burton, Jr.,

Health Savings Accounts allow employees (and employers) to contribute to a tax-free account to be used for eligible medical expenses. Flexible Spending Accounts are designed to provide employees with an opportunity to set aside funds on a pre-tax basis to pay for eligible out-of-pocket medical expenses. What is an HSA?

Inflation doesn’t just mean rising costs for workers and their employers; UK organisations could soon be faced with workforces that are unengaged, distracted and unhappy because of the state of their finances. However, employees may be able to minimise these losses by paying for some items before they are taxed.

In the ever-evolving world of employment, organizations are increasingly focusing on enhancing employee satisfaction and well-being. Alongside competitive salaries and career growth opportunities, companies are now offering a wide array of tax free or non taxable employee benefits to attract and retain top talent.

Management consultancy Eyekon Services has been ordered to pay a former employee £8,980 after an employment tribunal found him to have been unfairly dismissed. hours per week with a takehomepay of £1,363. Employment judge D Hoey said in the ruling: “His dismissal was unfair. Rodgers worked 37.5

As an employer, you’re obliged to provide your staff with a workplace pension – a mandate made compulsory by the UK government in 2012. The required minimum contribution is set at 8%, typically comprising of a 3% contribution by the employer and a 5% contribution by the employee. Is your provider helping with this?

This type of cafeteria plan gives employees the option to enroll in an account that allows them to set aside money from their paycheck tax-free and use it for qualified medical expenses. Types of expenses the FSA can pay for include co-pays, deductibles, and even some vision and dental expenses. Dependent Care Account.

This rule will apply to employers who have started retirement plans after December 29, 2022, and take effect for plan years starting in 2025. There is an exception for new companies in business for less than three years, employers with 10 or fewer employees, and governmental and church plans. The SECURE Act 2.0

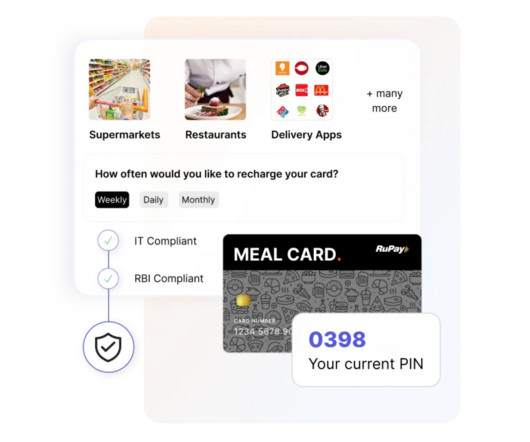

In today's fast-paced work environment, employers increasingly recognize the importance of providing employee meal allowances. In this complete guide, we will explore the concept of meal cards, their significance, and how you can introduce them in the workplace for the benefit of employees and employers. What are meal cards?

This type of cafeteria plan gives employees the option to enroll in an account that allows them to set aside money from their paycheck tax-free and use it for qualified medical expenses. Types of expenses the FSA can pay for include co-pays, deductibles, and even some vision and dental expenses. Dependent Care Account.

If there’s an annual increase going through, or someone’s just had a promotion, or it’s the start of the new tax year, for example, then they’ll be much more inclined to check how much they are being paid. Anything that is likely to change earnings, tax codes or NI letters, for example. “If

If your provider hasn’t informed you about salary sacrifice, the tax strategy that offers significant benefits, then you’re being short-changed. The tax you’re targeting here is National Insurance (NI). This happens because lower earnings mean less NI to pay. in Q1 2023 (the lowest ever being 3.4%

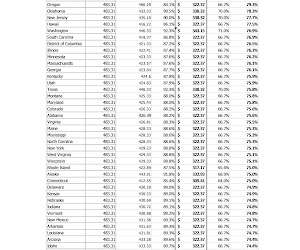

Her employment provides 42 weeks of work most years. While she and her employer might expect workers’ compensation to fully cover her earnings, what she will actually receive to cover her earnings loss depends greatly on where she lives. Interestingly, many of the states without state income taxes are at the lower end of this array.

Employmenttax compliance expert Alice Gilman, along with the editors of Business Management Daily’s Payroll Legal Alert, answer subscribers questions on payroll. W-2s: Pay to play? Question: One of the reasons the company switched third-party payroll providers was to allow employees to access their W-2s from home.

Pays the fees and waits for the nod. Step 6: Cash Talks Take into account wages in the industry and location and calculate salaries. Throw in benefits such as housing, transport, and insurance, staying true to the employment contract and UAE laws and regulations. If it’s outside the normal workday, you pay 1.26

Tax-preferred plans: Health flexible spending accounts, health savings accounts, health reimbursement accounts, transportation accounts, and more. Sometimes benefits are paid for wholly by employers; other times they are paid for by employees, and sometimes the expenses are shared. 401(k) and retirement plans. Considering a PEO?

Since yesterday, overtime paytaxes have dominated headlines, driven by a proposal from the current administration to exempt overtime earnings from federal income tax. Beyond the paycheck, this overtime tax policy could reshape workforce planning, employee morale, employee incentives and organizational strategies.

President Trump’s executive order suspending the employee portion of Social Security taxes, issued two weeks ago, left many employers wondering what to do. Then, the Treasury Department offered some clarity on the payroll tax. We’ve spent the better part of this week reading other tax lawyers’ opinions about this.

Whether its leveraging tax-efficient Salary Sacrifice schemes or taking a more holistic approach such as flexible working, its definitely possible to offer great benefits while boosting your bottom line. Investing in your employees’ growth can pay off in multiple ways. Want Real Value For Money?

You understand the triple-tax-advantaged, money-saving, long-term-investment potential of an HSA. After all, both can be used to cover health-related expenses and can be funded with pre-tax dollars. HSA accounts, on the other hand, belong to the employee, not the employer. Its a reasonable assumption.

A dependent care flexible spending account (FSA) lets participants set aside pre-tax dollars to help pay for dependent care. Contributing to this benefit reduces taxable income and spreads the benefits of pre-tax dollars throughout the year, helping you save 30 percent or more (based on your tax rate) on your dependent care costs.

These are the extras that employers can choose to offer, from gym memberships to flexible work hours, designed to make your work life more enjoyable. With Empuls, you can: Deliver tax-free fringe benefits like fuel reimbursements, meal cards, LTA, and more—helping employees maximize their take-homepay.

Military personnel and federal employees will not be able to opt-out of the plan to defer payroll taxes beginning from mid-September through December, despite protests from the lawmakers and employee representatives. a month will not have their Social Security taxes deferred. per pay period. Those who earn more than $8,666.66

Next, list your monthly expenses, including your rent or mortgage payments, utilities, groceries, pharmaceutical or medical needs, child care costs, home or auto maintenance, debt payments and insurance premiums, and anything else you regularly pay for, including expenses you might only pay annually.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content