This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Taxes can have a significant impact on family offices, influencing decisions around structure, investing and overall planning strategies. McDermott’s Family Office Tax webinar series explores the latest trends and guidance on tax planning for family offices and identifies opportunities to optimize tax efficiency.

Last month, the Washington Court of Appeals affirmed a lower court’s decision to dismiss a challenge to the recently enacted payroll expense tax in Seattle, WA. The tax, which went into effect on January 1, 2021, […]. Seattle Metro. Chamber of Commerce v. City of Seattle, No. 82830-4-I, 2022 WL 2206828 (Wash. June 21, 2022).

They also focus on certain aspects of this insurance product as it relates to executivecompensation and employee benefits matters. Listen to the podcast David Teigman: Hello and welcome to The Proskauer Benefits Brief: Legal Insight on Employee Benefits and ExecutiveCompensation. Welcome to you both.

When federal tax reform happens, it makes headlines across all media, with the news of sweeping tax changes and how they impact businesses and individuals. Our nation’s first major tax reform in more than 30 years has spurred many business owners to spend hours with their CPAs and tax consultants over the past few months.

Are your retirement plan programs in full compliance with ERISA and fiduciary responsibilities including filings of all required tax reporting? Review any and all TOP HAT or executivecompensation programs, and be sure to address any unfunded liabilities or promises like bonus agreements.

The Tax Court’s May 3, 2023, decision in ES NPA Holding, LLC v. The Tax Court further stated that “[it does] not view Revenue Procedure 93‑27 in such a restricted manner, but rather view[s] [Revenue Procedure 93‑27] as administrative guidance on the treatment of the receipt of a partnership profits interest for services.”

In general, the effect of the irrevocable election is that taxpayers can pre-pay the tax liability associated with the property while it has a lower valuation (assuming the propertys value increases in the following years). Please contact a member of the team with questions.

Act of 2022 (“SECURE 2.0”) required that effective as of January 1, 2024 , participants in 401(k) plans, 403(b) plans, or governmental 457(b) plans, who were age 50 or older and whose Social Security wages for the previous year exceed $145,000 (indexed), only be permitted to make catch-up contributions under such plans on a Roth (after-tax) basis.

According to our tally, you’ll probably be crossing paths with Accounts Payable, Benefits, HR and the executivecompensation committee. Executivecompensation committee: 20% excise tax on golden parachute payments, income from the exercise of nonstatutory stock options and nonqualified deferred compensation.

David Teigman: Hello and welcome to The Proskauer Benefits Brief: Legal Insight on Employee Benefits and ExecutiveCompensation. Stay tuned for more insights on employee benefits and executivecompensation, and be sure to follow us on Apple Podcasts, Google Podcasts and Spotify.

A decision not to claw back compensation is required to be disclosed and is subject to review by the exchange. Proskauer’s Employee Benefits and ExecutiveCompensation team is advising issuers on implementation of new clawback policies and updating existing clawback policies to comply with the listing standards as they are finalized.

The “golden parachute” excise tax regime under Internal Revenue Code Sections 280G and 4999 (“Section 280G” and “Section 4999”, respectively) is at the core of both public and private U.S.-based compensationtax deduction. When Do the Golden Parachute Tax Provisions Apply? Background. based transactions. corporations.

The Internal Revenue Service (IRS) has announced plans to initiate dozens of new audits this spring in an attempt to ground high-flying taxpayers and their personal usage of corporate aircrafts. These audits will focus primarily on “highest-risk” corporations and large partnerships, IRS Commissioner Danny Werfel stated.

Other Issues: Repricings and exchanges implicate a number of other complex issues including, without limitation, tax issues, securities law issues (including tender offer issues), and accounting issues.

The Internal Revenue Service (IRS) recently issued needed relief to extend some amendment deadlines for non-governmental qualified retirement plans and 403(b) plans, and for individual retirement accounts (IRAs) under the Setting Every Community Up for Retirement Enhancement Act of 2019 (SECURE Act), the Bipartisan American Miners Act of 2019 (Miners (..)

On September 26, 2022, the Internal Revenue Service (IRS) extended the amendment deadline for non-governmental qualified retirement plans, plans covered under Section 403(b) of the Internal Revenue Code (Code) and individual retirement accounts (IRAs).

While it may not provide new information for individuals that regularly practice in this space, it will almost certainly be a good initial read for those that are not familiar with Section 409A of the Code or for those that do not regularly work with deferred compensation programs.

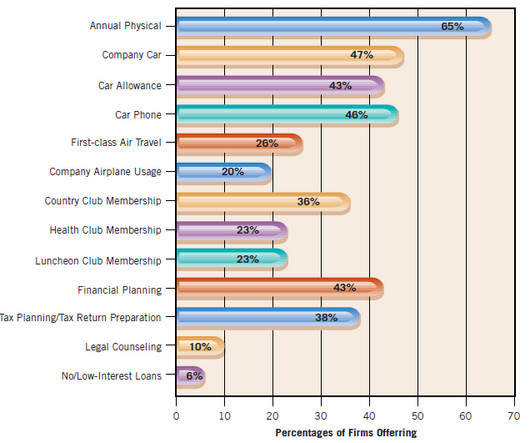

Many organizations, especially large ones, administer executivecompensation somewhat differently than compensation for lower-level employees. An executive typically is someone in the top two levels of an organization, such as Chief Executive Officer (CEO), President, or Senior Vice-President.

Key Person Insurance The untimely loss of a top executive or critical team member could severely disrupt business operations and adversely impact revenue streams. The policy’s death benefit, which is typically tax-free and available shortly after the key person’s passing, can provide essential capital.

The ARPA also allows the employer, insurer, or multiemployer plan sponsor who subsided the premiums to offset the cost by claiming a new federal tax credit. The subsidy is tax-free to the individual receiving the subsidy. Tax Credit. Below is a summary of the ARPA’s COBRA subsidy provisions. Changes to Code Section 162(m).

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content