This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Pension COLAs - Pensionbenefits for some retirees are also indexed for inflation. An example is pensions for federal government workers and military retirees and disabled veterans. a $59 increase for every $1,000 of benefits) in 2022. Their COLA, like Social Security, is 5.9% (i.e.,

If the husband dies first, the wife is left with $1,250 (50% of husband’s pension), $800-wife’s pension, and $2,000 (highest Social Security) for income of $4,050 ($48,600 annually). If the wife dies first, the husband might receive a higher pensionbenefit because there will no longer be a reduction for spousal benefits.

As people age, making ends meet day-to-day takes a back seat as finances become more stable. The financial difficulties caused by these lifestyle events are similar and can be managed within a general financial wellness programme. But there is another lifestage that presents different financial challenges.

Other benefits also continue. Tricky Rules - Employers may have rules that prevent older workers from collecting pensionbenefits or former workers from returning as freelancers until a break in service.

At Ashurst, we closely consider the pension and benefits we offer and focus particularly on how we engage our people in these offerings to ensure they are of maximum benefit. Because pension forms part of an employee’s finances, tackling the broader topic of finances also increases engagement with pensions.

Trott has taken over responsibility for pensionerbenefits including state, private and occupational provisions, as well as oversight of bodies such as The Pensions Regulator (TPR). Present press speculation around tax allowances for pensions are particularly concerning.

Then in the years before retirement, support should be provided around tax efficiency, planning for retirement and understanding retirement income options, clearing debt and maximising pensionbenefits and other savings.

There are some options that employees should be aware of to either avoid or reduce the impact of the LTA: Review current situation – If they have already taken some pensionbenefits, they should start by looking at a current pension valuation and assessing how much of their LTA they have used.

If an employee is at least 65, has held a high policy-making or executive position for the preceding two years, and is entitled to receive employer-financedpensionbenefits or other retirement benefits of at least $44,000 annually, they may be subject to mandatory retirement policies.

In fact, an Employee Benefit Research Institute report 2 has shown that 64% of workers feel somewhat confident about having enough money in retirement, while 18% are confident in their retirement structure. Compared to this, the retirees, 75% in exact, have showcased confidence in their retirement finances.

A Stanford-led study revealed that nearly half of teachers surveyed were frequently anxious about their finances, compared to only 17% of the general population. Because of stagnant salaries, educators face challenges not only in managing their daily finances but also in planning for larger expenses.

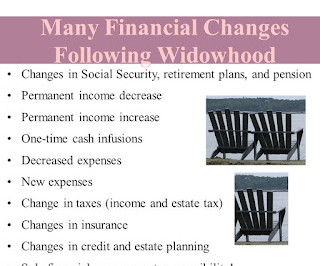

A story was shared about a couple that had $6,000 in income and only $2,000 when the wife was widowed and lost all pensionbenefits and was left with only one Social Security check. Under the 1984 Retirement Equity Act, workers cannot waive survivor benefits without the written consent of their spouses. Fear mongering?

After I ended my Rutgers Cooperative Extension career in January 2020 and started claiming a federal pension, my earned SS benefit took a big haircut due to the Windfall Elimination Provision (WEP). Some people have referred to folks like me who earned both Social Security and pensionbenefits in a derogatory way.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content