This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As people age, making ends meet day-to-day takes a back seat as finances become more stable. Then, when they’re ready, they want to understand how to turn their pension savings into an income for life. Perhaps they’ve taken a career break to raise a family or freelanced without a pension in place. In one sense, they’re right.

Tax Bracket Triggers - When earnings are added to a pension, Social Security, RMDs, and other taxable income, planning is needed to avoid a higher tax rate or Medicare premium. Other benefits also continue. Income in Lieu of Savings - Earnings from work can postpone withdrawals from retirement savings (e.g.,

Prime Minister Rishi Sunak has appointed Laura Trott MBE as minister for pensions, after predecessor Alex Burghart officially held the role for less than one month. Trott was appointed on 27 October, and the Department for Work and Pensions (DWP) made the announcement on 7 November via its official Twitter account.

At Ashurst, we closely consider the pension and benefits we offer and focus particularly on how we engage our people in these offerings to ensure they are of maximum benefit. Because pension forms part of an employee’s finances, tackling the broader topic of finances also increases engagement with pensions.

The Work and Pensions Committee is calling for trials of automatic appointments with the Pension Wise service as part of its new ‘Stronger Nudge’ interventions. The post Early and multiple interventions will improve pensions engagement! appeared first on Employee Benefits.

million pension savers [1] are set to reach the limit and will be hit with a tax charge of 55% in retirement. This could particularly affect those who never check the value of their pension, or haven’t done so for some time. Positive pension fund growth as well as a pay rise may easily push them over the LTA before they know it.

In fact, an Employee Benefit Research Institute report 2 has shown that 64% of workers feel somewhat confident about having enough money in retirement, while 18% are confident in their retirement structure. Compared to this, the retirees, 75% in exact, have showcased confidence in their retirement finances.

If an employee is at least 65, has held a high policy-making or executive position for the preceding two years, and is entitled to receive employer-financedpensionbenefits or other retirement benefits of at least $44,000 annually, they may be subject to mandatory retirement policies.

Pension COLAs - Pensionbenefits for some retirees are also indexed for inflation. An example is pensions for federal government workers and military retirees and disabled veterans. a $59 increase for every $1,000 of benefits) in 2022. Other pensions have frozen or suspended COLAs for their retirees (e.g.,

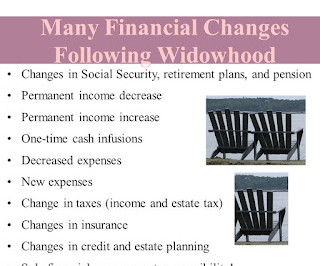

A married couple has four monthly income streams: $2,500- husband’s pension, $2,000- husband’s Social Security, $800- wife’s pension, and $1,500- wife’s Social Security for a total of $6,800 ($81,600 annually). The wife’s pension and Social Security would go away, however, which could still result in a decrease in household income.

A Stanford-led study revealed that nearly half of teachers surveyed were frequently anxious about their finances, compared to only 17% of the general population. Because of stagnant salaries, educators face challenges not only in managing their daily finances but also in planning for larger expenses.

The law will repeal the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) that reduced public sector workers' earned Social Security benefits. Some people have referred to folks like me who earned both Social Security and pensionbenefits in a derogatory way. After decades of failed attempts, H.R.

A story was shared about a couple that had $6,000 in income and only $2,000 when the wife was widowed and lost all pensionbenefits and was left with only one Social Security check. Under the 1984 Retirement Equity Act, workers cannot waive survivor benefits without the written consent of their spouses. Fear mongering?

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content