This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Below are some key things to know about annuities from a recent seminar that I attended: Complexity- Annuities are often sold as a “simple” investment but, in reality, they can be quite complicated. They are often bought with money from settlements, investment accounts, and pension plan lump sum distributions.

So far, it has been delivered to approximately 80,000 of its UK employees. Kerry Shiels, pension and benefits director at BT, says: “It is very important that employees understand their BT pension and the retirement decisions they will need to make in the lead up to, and at, retirement. before financial education, to 4.1

Need to know: Employers can tailor content and communication channels to different employee groups to help with their pensions knowledge. Losing the jargon will make the language of pensions easier to understand and more relevant to staff. They could invest in financial coaching for a more personal approach to pensions education.

I recently attended a seminar about financial concerns facing women in retirement. pension, Social Security, annuities, dividends/capital gains, full- or part -time employment, self-employment) minus fixed (e.g., Baby Boomers were “guinea pigs” for the use of 401(k)s, often as a substitute for defined benefit pensions.

At its simplest, it could simply mean providing online or workplace-based resources which employees can access in order to boost their understanding of their finances. Advice means speaking with an accredited expert who can actively advise and help the individual through managing their finances. What are the costs involved? .

This could include an Employee Assistance Programme (EAP) offering debt advice, access to discount schemes, and the option to attend financial education sessions, all of which combined can help employees take control of their day-to-day finances.

Most of us spend the majority of our working life saving into our pension. However, all this hard work saving can quickly unravel for those who aren’t aware of common pension mistakes. WEALTH at work outlines below the top 10 pension mistakes individuals could make, to highlight what employees facing retirement may need support with.

In February 2020, the Money and Pension Service (MAPS) rolled out a 10-year strategy for financial wellbeing , which identifies workplaces as a key channel through which the UK can become financially healthier. Pensions . The UK government is certainly hoping employers will intervene in this area. Salary sacrifice schemes .

Employees can also participate in bespoke financial wellbeing workshops, featuring guides, webinars and in-person seminars on topics such as pensions and protection, budgeting , saving and investing.

The FCA and Government are seeking views as part of the joint Advice Guidance Boundary Review which focuses on proposals for closing the advice gap – the difficulty individuals face in recognising the need for accessing support in managing their finances. In doing so, they may then realise that they need specialist advice.

Here are some examples: Structured learning: eLearning courses In-person training Structured, recorded 1-2-1 conversations Professional qualifications Unstructured learning: Online seminars and webinars (like Ciphr’s series of HR webinars ) Reading Research Coaching or mentoring How FCA compliance and regulatory training courses from Ciphr can help (..)

One in six (17%) has made further ‘savings’ by cutting back (or cancelling) their personal insurance cover, such as income protection, life insurance, and medical or dental insurance, and one in seven (14%) has reduced their pension contributions – decisions which may prove to have costly consequences in the future.

Financial education and planning resources : Providing financial education and planning resources can help employees make better financial decisions and reduce stress related to personal finances. Some employers offer financial planning services or seminars on topics such as budgeting, investing, and retirement planning.

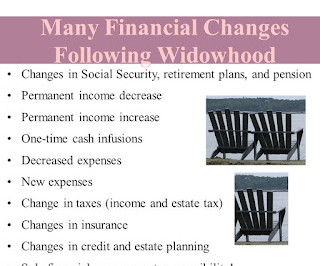

This post describes five changes in income and expenses that widowed persons can expect: Reduced Income - I heard this example at a recent seminar. If the husband dies first, the wife is left with $1,250 (50% of husband’s pension), $800-wife’s pension, and $2,000 (highest Social Security) for income of $4,050 ($48,600 annually).

I used to get invites to free meal seminars when I lived in New Jersey (after I turned 50) but they all say “No brokers, agents, or advisors.” Since few people in Florida know that I am a financial educator, I decided to go “undercover” to observe the seminar content, presentation style, and participants.

Not a week goes by that I dont receive colorful tri-fold invitations to free meal seminars for investments and preplanned burials and cremations. Below are five Barbservations about the seminar format, content, and take-aways: You Will Get Hungry- I typically eat dinner around 6:30 pm, which is when the presentation was slated to start.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content