This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Many older adults also have multiple income sources including Social Security, a pension, full-or part-time work or self-employment, withdrawals from retirement savings (including taxable required minimum distributions or RMDs), and interest, dividends, and capital gains on investments. In other instances (e.g.,

Now that 2021 income tax season has been over for a month and the dust has settled, it is time to start some serious tax planning for 2022. Planning now provides seven months to take action and/or implement changes to avoid a stressful “tax scramble” at the end of the year. assets that are taxed in different ways).

If you picture retirement planning and taxes as a Venn Diagram, there is lots of overlap between these two areas of personal finance. This is true both during one’s working years (when taxpayers are saving for retirement) and later, when people are older and withdrawing taxable income from tax-deferred accounts.

One of the niche audiences for my business, Money Talk , is older adults grappling with financial issues such as creation of a retirement “paycheck,” paying taxes on required minimum distributions (RMDs), and simplifying financial accounts. Tax-free accounts (e.g., Tax-free accounts (e.g., Tax-deferred accounts (e.g.,

Tax Planning - Until 12/31/25, taxes are “on sale.” Nobody has a crystal ball, but we know that tax rates will rise starting in 2026 when the Tax Cuts and Jobs Act expires. There are only two ways to reduce taxes: 1. When the government lowers tax rates. Make less income and 2. Financial knowledge is power.

Key Services: Talent and Reward Consulting Employee Benefits and Risk Management HR Technology Implementation Retirement and Pension Plan Consulting Talent Analytics and Workforce Planning Why It Stands Out WTW is known for its robust talent analytics and data-driven HR solutions. Headquartered in London, WTW operates in over 140 countries.

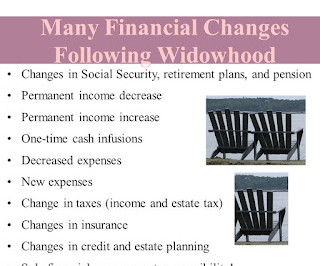

Common challenges that affect many widows/widowers are aloneness, a lower income, increased taxes/higher tax rate filing as an individual vs. a couple, loss of services that a deceased spouse used to perform, and no longer spending time with couples. It includes lying about finances and debt and hiding purchases.

I recently taught a 90-minute personal finance class for women age 50+. Depending on household income/assets and lifestyle decisions, income taxes and housing costs may increase or decrease. 401(k)s), tax-deferred accounts (e.g., IRAs), taxable accounts, rental real estate, other assets (e.g.,

Off-Farm Job Employer Benefits - These include a defined benefit pension, an employer retirement savings plan (e.g., Individual Retirement Account (IRA)- There are two types: traditional (funded with before-tax dollars) and Roth (funded with after-tax dollars). health insurance). barn, silo, riding arena), farm equipment (e.g.,

Many are middle income taxpayers who diligently saved and invested for 4-5 decades in tax-advantaged plans. As I wrote in my book Flipping a Switch , some older adults must “plan for higher taxes in the future, especially when required minimum distributions (RMDs) kick in.” IRMAA surcharges. to $573.30 for Medicare Part B and $12.40

Pension COLAs - Pension benefits for some retirees are also indexed for inflation. An example is pensions for federal government workers and military retirees and disabled veterans. Other pensions have frozen or suspended COLAs for their retirees (e.g., the New Jersey state pension plan).

Three Types- Fixed annuities are like CDs, only tax-deferred, and guarantee a certain interest rate for a specified time period. Variable annuities are like mutual funds, only tax-deferred, and their owners select underlying mutual funds, called subaccounts, which determine an annuity’s performance. Medicaid planning, 2.

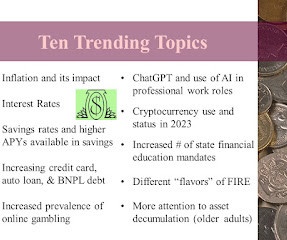

Inflation-induced price hikes on goods and services are like a regressive sales tax and hurt those with low incomes the most. This means that more young adults will enter college, careers, or the military with personal finance knowledge. Below is a brief description of the ten trends that I discussed: Inflation- The U.S.

This includes Social Security recipients, retirees with COLA-adjusted pensions, and workers with COLAs stipulated in their job or union contracts. Marginal Tax Brackets - Income ranges in the seven marginal tax brackets ranging from 10% to 37% are inflation-based. When inflation rises, workers can save more money.

when there are no more early withdrawal penalties on money removed from tax-deferred accounts) and the start of required minimum distributions (RMDs). Many people are in a lower marginal tax bracket during their gap years (especially after leaving a primary career) than they will be later when RMD withdrawals must begin.

A married couple has four monthly income streams: $2,500- husband’s pension, $2,000- husband’s Social Security, $800- wife’s pension, and $1,500- wife’s Social Security for a total of $6,800 ($81,600 annually). The wife’s pension and Social Security would go away, however, which could still result in a decrease in household income.

Tax Write-Off for Self-Employment Tax - On line 15 of Schedule 2 (for a 1040 form), self-employed workers can write off the deductible portion of their self-employment tax (calculated on Schedule SE), which will lower adjusted gross income (AGI), a trigger for many other taxes.

The 2023 income tax filing deadline is only days away (April 15, 2024 in most of the U.S.). It will be a busy weekend for many taxpayers and tax preparers who are filing tax returns or tax filing extensions. money that has been taxed) and can be withdrawn at any time for any reason tax-free and penalty-free.

It is also easier to keep personal and business finances separate by maintaining dedicated bank accounts and credit cards for business transactions. Stick to a Schedule - Invoicing clients promptly and following up on overdue payments can maintain healthy cash flow and avoid disruptions to personal finances. of net business income.

Tax on Social Security Benefits - Income from unretiring may push older taxpayers into the income range where tax is due on a portion of Social Security benefits. Tax Withholding Adjustments - Adding income from employment to what could be multiple streams of income in later life (e.g., food, gas, utilities, housing, etc.)

Chapter 3 - Three tricky retirement expenses to project in advance are health care, housing, and taxes and the four Ls of spending in later life are Lifestyle, Longevity, Legacy, and Liquidity. a pension and Social Security). health care, long-term care, inflation, death of a spouse, family responsibilities, and divorce).

So far, it has been delivered to approximately 80,000 of its UK employees. Kerry Shiels, pension and benefits director at BT, says: “It is very important that employees understand their BT pension and the retirement decisions they will need to make in the lead up to, and at, retirement.

Need to know: Employers can tailor content and communication channels to different employee groups to help with their pensions knowledge. Losing the jargon will make the language of pensions easier to understand and more relevant to staff. They could invest in financial coaching for a more personal approach to pensions education.

For example, workers with a guaranteed pension and/or a high investment risk tolerance might want to have more stock exposure in a TDF and would chose a target date farther off in the future. Make Tax-Advantaged Gifts - Consider “bunching” charitable donations with other tax deductions (e.g.,

lost pension pots in the UK, worth around £26.6 billion WEALTH at work explains how employees can track down lost pensions and provides guidance on whether to consolidate The total value of lost pension pots has grown from £19.4 million lost pension pots sitting unclaimed because they’ve been simply lost or forgotten about.

One of the most daunting financial aspects of retirement, especially for people who have been diligent savers throughout their working years, is taking required minimum distributions (RMDs) from their tax-deferred retirement savings accounts beginning at age 72. New RMD tables went into effect in 2022, so this is a good time to discuss RMDs.

bank and investment accounts, pension, Social Security) should have a two-factor (a.k.a., Keeping current” also means paying attention to scams that feed off current events such as COVID-19, tax season, wars, and natural disasters. Another hygiene practice is using strong passwords with a variety of types of characters.

With increasing costs continually putting pressure on household finances, 2023 is set to be a financially challenging year for many. It’s therefore now more important than ever to support employees to take control of their finances to successfully navigate the cost-of-living crisis. Track your finances. Create a budget.

WEALTH at work, a leading financial wellbeing and retirement specialist has run financial education workshops for staff in hundreds of organisations and is encouraging people to consider using this saving in National Insurance if they can, to increase their monthly pension contributions. When made into a pension contribution it is worth £206.39

Transitioning to a superior provider is no longer a hassle: If you’re contemplating changing your current workplace pension scheme, the process isn’t as challenging as you might think. Many pension companies (we’re one of them!) What is a workplace pension? are prepared to assist you with the heavy lifting.

With interest rates on the rise, we often get asked at our financial education sessions, is it best to pay off your mortgage or pay into your pension? He concludes, “Many employers offer financial education in the workplace, to help their staff to understand their finances so they are better prepared to make decisions like these.”

It’s now more important than ever to support employees to take control of their finances. Create a budget – The first step to taking control of your finances is to create a budget. Start saving early – Starting to save when you are younger into ISAs and a pension means that the money has lots of time to grow.

As the cost of living crisis continues, it is now more important than ever that new parents understand how their finances will be affected and what actions they can take. WEALTH at work, a leading financial wellbeing and retirement specialist, highlights some top tips to help new parents stay in control of their finances: 1.

Below are seven key take-aways: Benefit Payments - Retirement benefits are determined by the amount workers earn and pay in FICA (Federal Insurance Contributions Act) tax, which often shows on paychecks as OASDI. Total FICA tax is 15.3% The 7.65% tax is divided: 6.2% quarters of coverage) when they work and pay FICA tax.

pension, Social Security, annuities, dividends/capital gains, full- or part -time employment, self-employment) minus fixed (e.g., America’s 401(k) Experiment - 2023 is the 45 th anniversary of tax-deferred 401(k) retirement savings plans that workers fund with voluntary contributions from their pay. insurance premium) expenses.

lawn care, tax preparer, hair dresser), natural gas for home heating, electricity, and auto and homeowners insurance. pensions, Social Security, annuities) can “ride it out.” In informal polls of my students, LinkedIn connections, and Facebook friends, higher expenses that stood out to them were food (e.g., $5+ 5+ for 12 eggs!),

Tax on Social Security Benefits - Those who work and claim benefits will trigger taxes with a combined income above $25,000 (individuals) or $32,000 (married couples filing jointly). Continued FICA Tax - Like all workers, employed older adults must pay Social Security/ Medicare tax. Other benefits also continue.

Four in ten (41%) say they don’t feel supported in their workplace when it comes to getting help to understand their finances. Worryingly, 54% would seek guidance about their pension from someone unqualified like family and friends, or no one at all, and only 14% would speak to their employer. There are 2.8

However, many don’t realise the significant difference a small increase to their pension savings can make. For example, someone in their 20s, saving an extra 1% a year with their employer matching this, may be able to increase their pension pot in retirement by 25%. They are all 25 years old and plan to retire at age 68.

Unported Deed, resized Emma Reynolds, the elected Labour MP for Wycombe, has been appointed parliamentary secretary for both the Department of Work and Pensions (DWP) and HM Treasury. The new joint role is part of the new government’s recognition that pensions are the responsibilities of both departments.

Prime Minister Rishi Sunak has appointed Laura Trott MBE as minister for pensions, after predecessor Alex Burghart officially held the role for less than one month. Trott was appointed on 27 October, and the Department for Work and Pensions (DWP) made the announcement on 7 November via its official Twitter account.

The FCA announced that more over 55s are accessing their pensions, and over half are cashing out their pension pots completely. Jonathan Watts-Lay, Director, WEALTH at work – a leading financial wellbeing and retirement specialist comments; “It’s concerning that so many pensions are being cashed out in full.

At its simplest, it could simply mean providing online or workplace-based resources which employees can access in order to boost their understanding of their finances. Advice means speaking with an accredited expert who can actively advise and help the individual through managing their finances. What are the benefits? .

Huddersfield-based children’s Hospice charity Forget Me Not has launched a salary sacrifice pension arrangement in order to look after the financial wellbeing of its 140 employees. This is then paid into their pension account before national insurance and tax is taken from their salary.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content