This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The new year brings a new start for people’s finances, giving you the chance to re-evaluate your situation and make changes based on your priorities. This could begin with making a plan to pay off any outstanding debts that have been causing stress, or just being aware of changes that may impact your finances.

This is typically done in employer retirement savings plans with an auto-escalation feature that automatically increases an employee’s contribution amount by a specific percentage of pay. Take time to consider your savings goals and if you are on track to achieve them. What people think about, they bring about.

Below are five examples: ¨ Maintain a Low Debt-to-Income Ratio- Keep monthly consumer debt payments (all debts except a mortgage) at 15% or less of monthly take-homepay. Example: $275 of debt payments ÷ $2,500 of net pay equals a consumer debt-to-income ratio of 11% (275 divided by 2,500).

The cost to the employee of this increase in contribution is a reduction in takehomepay of less than £12 per month (£136pa). The cost to the employee of this increase in contribution is a reduction in takehomepay of £17 per month (£204pa). 2025 UK adults aged 22+ in full time employment were surveyed.

Colleagues can access information about everything on offer, as well as self-serve additional salary sacrifice options such as additional pension contributions, family private medical insurance, holiday purchase and cycle to work, and instantly see how this will impact their takehomepay.

Phil Campbell, customer operations director at ScotRail, said: “I am pleased that Unite members have voted to accept this pay deal. All parties involved have worked hard to find an agreement that recognises the hard work of staff, as well as providing value for money for the public finances.

Importance of understanding the implications for businesses and individuals Being informed about the UK budget helps people make informed financial decisions, adapt to changes in the economy, and proactively manage both personal finances in response to government policies and priorities. appeared first on Employee Benefits.

“Benefits that can greatly reduce financial burdens and improve financial wellbeing, such as cashback schemes and greater access to financial resources to help budget, can be helpful to stretch take-homepay as much as possible,” she says.

These employees will need guidance and support to understand the impact on their finances and what options are available for them, as this can negatively impact wellbeing and productivity. Open communication is key, adds James. “This open dialogue allows employers to identify areas where they can provide targeted assistance.” .

However, if you’re an HR or Finance Lead tasked with selecting a new workplace pension, you might need a dedicated account manager who can assist with staff onboarding and implementation. Net Pay contributions from your employees is deducted before tax. Do they provide support when required?

Since we had contributed pre-tax to our HSA before birth our takehomepay was lower. What to Do as Your Child Grows : Prepare your finances. Fertility trackers and treatments Ovulation tests Pregnancy tests Some over the counter medications Prescriptions related to family planning Prenatal vitamins.

While the margin of increase in the new wage rates in Ontario is minimal, when calculated over a period of time, it should make a difference to the take-homepay for workers. Those who earn minimum wage and work 40 hours a week will see their annual pay increase by up to $835 shortly. in the province.

They were first resistant to escalation, fearing that they would go too far and substantially reduce employees’ take-homepay. New plan sponsors shouldn’t feel a 6% start is overly paternalistic or interferes with employees’ short-term finances, especially for lower-paid individuals.

For many employee-owned businesses, a significant advantage comes from increased take-homepay and better wages overall. The Right Financing Model It’s also important to align your program’s financing structure with employee ownership goals. Let’s look closer at several of these outcomes: 1.

In a nutshell, this mechanism allows employees to maintain their pension contributions and even enjoy a slightly higher take-homepay. It’s a clever tax manoeuvre that reduces the National Insurance (NI) contributions individuals need to pay.

Inflation doesn’t just mean rising costs for workers and their employers; UK organisations could soon be faced with workforces that are unengaged, distracted and unhappy because of the state of their finances. Pay your workers as much as you can afford and ensure that those at the bottom of the pay scale earn enough to live on.

Hand out payslips that include gross salary, bonuses, overtime, deductions, and the final take-homepay. Improved Reporting: HR and finance teams can generate comprehensive reports on payroll, attendance, and other HR metrics, enabling informed decision-making. Clear communication is key!

“Benefits that can greatly reduce financial burdens and improve financial wellbeing, such as cashback schemes and greater access to financial resources to help budget can be helpful to stretch take-homepay as much as possible,” she says.

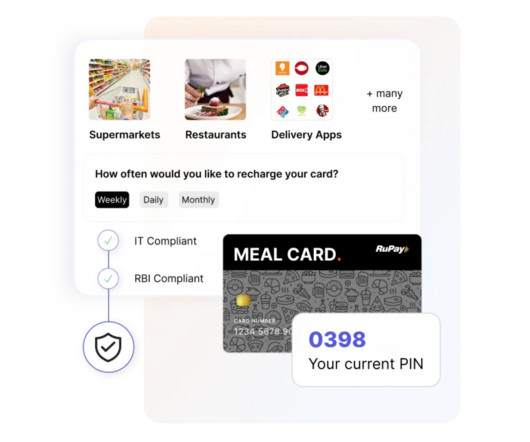

Improved budgeting and financial management Meal cards provide employees with a dedicated meal allowance, which can help them better manage their finances. Employees can maximize their tax benefits and potentially increase their take-homepay by utilizing meal cards. Here are some of them: 1.

According to the survey, 75% of Americans felt they were not financially secure, and 30% expressed that they would likely never feel confident about their finances. Workers living with these pressures are constantly worried about finances and fear unexpected expenses that may tip the scales.

Next, list your monthly expenses, including your rent or mortgage payments, utilities, groceries, pharmaceutical or medical needs, child care costs, home or auto maintenance, debt payments and insurance premiums, and anything else you regularly pay for, including expenses you might only pay annually. Prioritize debt repayment.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content