This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

You must be enrolled in an HDHP to be eligible to participate in a healthsavingsaccount (HSA). PPOs are a common type of traditional health plan. What’s a PPO? ” Costs are more manageable when you use providers that are in your plan’s network.

Employers who offer healthsavingsaccount-eligible high-deductible health plans (HDHPs) to employees can significantly expand pre-deductible coverage for certain drugs used to manage chronic conditions — with only a tiny effect on premiums. Absenteeism. Illness-related presenteeism. Cost of temporary workers.

How Medicare eligibility affects healthsavingsaccounts. Discontinuing group health coverage. That said, workers who are still on your plan should sign up for Original Medicare Part A (hospital insurance) when they are first eligible. Healthsavingsaccounts.

Potential savings and other benefits In a study published in the American Journal of Managed Care , researchers at the Perelman School of Medicine at the University of Pennsylvania found that average per-visit costs for hospitals in Penn Medicine’s OnDemand telemedicine program were 23% less than for in-person visits.

First and second time group health insurance buyers usually miss the opportunity to buy a healthsavingsaccount (HSA)-qualified high-deductible health plan (HDHP). HealthSavingsAccounts. The network doesn’t include your old doctor or hospital.

Study findings The trend of more Gen Z workers gravitating to HDHPs makes sense, since these plans are best suited for younger individuals who are generally healthier and have fewer health problems than their older counterparts — Gen Xers and Baby Boomers.

In addition to a general retirement account, consider a HealthSavingsAccount (HSA). Making HSA investments enables you to grow this tax advantaged account at a greater rate long-term, while giving you a reliable source of funds to turn to for both emergency and everyday medical expenses.

Co-pay: the fixed cost an employee must pay for each visit to a medical doctor or mental health professional’s office, urgent-care center or hospital emergency room. As long as the funds are used to pay for medical expenses, they are not taxed, and employees can keep the accounts when they leave the organization.

All of the plans offered the same network of doctors and hospitals. In other words, they paid $528 to save $250. The authors, both from the University of Wisconsin-Madison, found in a study of 331 companies, that at firms offering both a HDHP and a low-deductible plan, selecting the HDHP typically saves more than $500 a year.

Preferred provider organizations – PPOs contract with hospital and provider networks to help control costs. These plans usually have an attached healthsavingsaccount to which your workers can transfer funds pre-tax from their paychecks to use for paying deductibles, copays and other medical expenses.

Preferred provider organizations – PPOs contract with hospital and provider networks to help control costs. These plans usually have an attached healthsavingsaccount to which your workers can transfer funds pre-tax from their paychecks to use for paying deductibles, copays and other medical expenses.

HealthSavingsAccounts, Flexible Spending Accounts, and supplemental medical plans like accident, critical illness, and hospital indemnity insurance can be critical to help pay for out-of-pocket medical costs.

This can include: Basic medical services Hospital visits Emergency services Mental health services And more Key features of HDHPs High deductibles As the name suggests, HDHPs come with a high deductible. This can make HDHPs a great option for saving on monthly payments. Generally, HDHPs have lower premiums compared to others.

With a Flexible Spending Account (FSA), you can set aside up to $3,050 in pre-tax dollars per calendar year to pay for eligible medical expenses like doctor visits, hospitalizations, and prescription medications. That’s more money in your pocket! Maximize Your HSA.

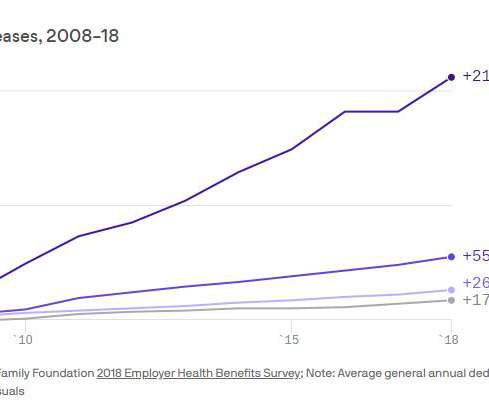

As the cost of medical plans rises, employers are offering high-deductible health plans (HDHPs) and healthsavingsaccounts (HSAs) as part of their employee benefit plans. Over 10 years, HDHP enrollment with a healthsavingsaccount (HSA) increased from 4.2% Before we get to that, consider the data.

Thankfully, she was able to pay through our HealthSavingsAccount (HSA) with her benefits card. If needed, our pre-tax healthaccount would cover additional diagnostic tests, as well as hospital services, lab fees, and mastectomy-related special bras. What to do next.

Additionally, the federal government has started increasing price transparency for health care services, which can help with comparison shopping. For example, new rules require hospitals to post pricing online for various services and procedures. Starting next year, health insurers must share their negotiated prices with the public.

First and second time group health insurance buyers usually miss the opportunity to buy a healthsavingsaccount (HSA)-qualified high-deductible health plan (HDHP). HealthSavingsAccounts. The network doesn’t include your old doctor or hospital.

A flexible spending account (FSA), which can be used to cover childcare and medical costs tax-free. A healthsavingsaccount (HSA), which can also be used to cover medical expenses tax-free. Importantly, employees need to elect this coverage before pregnancy in order to be eligible for it.

Especially if you have a HealthSavingsAccount, or HSA. As a crash course for those of you who maybe aren’t as familiar with your benefits as you’d like to be, a HealthSavingsAccount is a tax-free account that allows you to purchase certain medical expenses that are determined by the IRS and your employer.

To temper an HDHP’s bite, they can be paired with healthsavingsaccounts. Advantage: Employees can contribute more on a pretax basis than they can put into flexible spending accounts. 2020 adjustments for group health plans set. EBRI found that HDHP enrollees are more likely to: Research doctors and hospitals.

This would include comprehensive health insurance that covers doctor visits, stays at the hospital, the cost of prescription drugs, and preventive care. It will keep the staff covered against all manner of medical facilities and remuneration for partaking in various healthcare services.

From 2009 to 2016 (the most recent data available), the average amount that hospitals billed insurance carriers for an emergency room visit more than doubled, from $600 to $1,322. The cost to the employer (and often the employee) is often far less than the ER. The high cost of ER care is enough to make anyone run a high temp.

A healthsavingsaccount (HSA) or flexible spending account (FSA) will let you pay your drug copays with pre-tax dollars. Don’t forget to check hospitals, labs, and other facilities. Subject line: How Can a Health Plan Help You Save for Retirement? Make sure you are using a preferred pharmacy.

It covers things including hospital and doctor visits, surgeries, and prescriptions. Employees don’t pay taxes on this money, which means they save an amount equal to the taxes they would have paid on the money you set aside. HealthSavingsAccount (HSA). Hospital Insurance. Medical Insurance. UHC.com ).

Health and welfare benefits and insurance Explain your company’s benefits and insurance offerings in detail, touching on all the following areas (if offered): Medical insurance: This type of insurance is likely a no-brainer—it’s one of four major types of benefits most employers offer. Employers usually cover a portion of this premium.

To qualify as such, the government states the plan must “pay at least 60% of the total cost of medical services for a standard population” and “include substantial coverage of physician and inpatient hospital services.”. Employers looking to impress with their employee benefits package go beyond this basic level of health benefits.

Flexible spending accounts (FSAs) and healthsavingsaccounts (HSAs) HSAs and FSAs can help employees better prepare for medical expenses and, in the case of HSAs, even help employees enhance their retirement savings. Having such a program may set your company apart in the job market.

Employees don’t pay taxes on this money, which means they save an amount equal to the taxes they would have paid on the money you set aside. HealthSavingsAccount (HSA): An HSA is a savingsaccount that lets employees set aside money on a pre-tax basis to pay for qualified medical expenses.

Coinsurance Meaning in Health Insurance Plans HealthCare.gov says coinsurance is a percentage of covered health care expenses that the policyholder must pay after meeting the deductible. This means that you have to pay 20% of the costs for covered care, such as hospital stays, doctor appointments and diagnostic tests.

Offer a High-Deductible Health Plan (HDHP) A high-deductible health plan (HDHP) is often combined with contributions to a Health Reimbursement Account (HRA) or a HealthSavingsAccount (HSA). There is no better example of this than the recent pandemic.

Medicare is also a government-run program that provides health insurance coverage for anyone 65 or older who has worked and paid Medicare taxes for at least ten years. Part A helps pay for hospital stays and inpatient care. Understanding your coverage choices can help you make informed health care decisions.

180,000 – 310,000 flu-related hospitalizations. If you have a HealthSavingsAccount (HSA) , Flexible Spending Account (FSA) , or Health Reimbursement Account (HRA) , you can typically cover the costs of getting the flu vaccination since it is considered a medically necessary procedure.

Source: MA Health Connector) This frees up an average of $2200 per year that can go towards a healthsavingsaccount or maybe pay down one’s credit cards. Employers are forcing employees to pay more for health insurance leaving less money to pay for actual health care.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content