This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Do you need to worry about workers’ compensation for remote employees? When your organization adopts or expands a work-from-home policy, it’s a good idea to take a fresh look at your workers’ compensation coverage and processes. It’s important to understand that employee injuries at home may be covered by workers’ compensation.

Managing workers’ compensation claims in New York can be a complex task for any HR professional, especially when it comes to ensuring a smooth process for all involved. New Yorks workers’ compensation laws are strict and designed to protect both the employee and employer. This must be done within 30 days of the injury.

Navigating employee benefits can be complex for employers, especially when balancing cost control with providing comprehensive offerings to workers. Acting as an intermediary between employers and insurance providers, benefit brokers help design, implement and manage employee benefits programs.

If you’re looking for ways to save on workers’ compensation insurance, you’re well aware of the direct costs that you pay in premiums. But what you may not have considered is the indirect costs of on-the-job accidents and injuries, which go beyond what you pay for workers’ compensation insurance.

Are you struggling with how to reduce workers’ compensation costs for your business? If not, do you understand the sizeable risk that workers’ compensation claims pose to your business, and do you have a plan in place for when these claims arise? That’s why controlling workers’ compensations costs is so important to your bottom line.

Everybody knows at least one gig worker—people who drive for Uber or Lyft, deliver food for DoorDash, freelance on Upwork, rent out rooms on Airbnb, or work a combination of jobs to piece an income together. Gig workers are also exposed to more legal liability. Still, some gig workers are fearless of the challenge.

We will deliver smarter, more engaging benefits communication solutions to stregthen companies, workers, and their families. . “By working with Flimp we’re elevating how we drive value into the relationship our clients have with their people.

Many group health insurance plan sponsors and administrators have the mistaken belief that the law allows employees enrolling in Section 125 cafeteria plans to change their elections, as long as they do so within 30 days of the plan becoming effective. This is not correct. And this misconception can have serious consequences.

According to a recent survey, four in 10 American workers live paycheck to paycheck. You as an employer can help by offering group disability insurance to your employees. This insurance helps replace a portion of a worker’s income if they lose their income due to an injury or illness. Tax-deductible premiums.

Any thoughts about using off-site, non-profits or charities to accommodate modified duty for an injured worker? a national workers’ compensation and human resources consulting company. She’s the author of two books: “ From Workers Comp Claimant to Valued Employee ” and “The Injury Management Challenge.”.

workers are not spending a significant amount of time researching health plans during open enrollment, including: Satisfaction with their plan — The study found that 90% of employees were satisfied or somewhat satisfied with their employer’s open enrollment process. workers were enrolled in them. In 2022, 32% were.

Here are the rules that will sunset at the end of 2021: Allowing employees who had declined group health insurance for the 2021 plan year to sign up for coverage. The ACA requires that the coverage is “affordable” for the worker, which is set as a percentage of their household income.

.” These global reinsurance giants have seen their profits erode substantially in the last few years due to the rising cost of natural catastrophes around the world, forcing them to increase what they charge insurancecarriers. These moves are trickling down into the primary insurance market in the form of further rate increases.

An example of this is a client company discovering that they’ve been continuing to pay for medical insurance for a terminated employee. Some compromise may be necessary When you choose your own insurance offering through a broker, you can select from a vast number of available insurancecarriers and plan designs.

Organizations need to learn to manage workers’ compensation claims. Organizations with organized claims and disability management programs have lower rates of lost work time, reduced costs, and less attorney involvement in their workers’ compensation claims. Lower loss costs means lower workers’ compensation costs.

Insurancecarriers have been trying out new approaches to controlling costs, while improving health outcomes for their plan enrollees. Talk to us about finding health plans that are offering different structures for addressing costs while also improving care for your workers. Other cost-saving measures.

If you’re looking for ways to save on workers’ compensation insurance, you’re well aware of the direct costs that you pay in premiums. But what you may not have considered are the indirect costs of on-the-job accidents and injuries, which go beyond what you pay for workers’ compensation insurance. Return-to-Work Program.

Also, since thieves will sometimes steal mail from mailboxes, you can recommend that your workers sign up for paperless communications from their insurer. Any of the above documents should be shredded when it’s time to replace or discard them. How to identify fraud.

The appellate court added, however, that the trial court should also have required the carrier to pay its proportionate share of the non-attorney’s fee expenses associated with securing the malpractice settlement. In its letters, it asserted its subrogation rights pursuant to the Texas Workers’ Compensation Act. Insurance Co.

Burnett sought workers’ compensation benefits with the employer’s Vermont insurancecarrier, which denied the claim citing a lack of jurisdiction. 616(a) was ambiguous and must be interpreted in context with other provisions of the Workers’ Compensation Act. Burnett appealed to the Vermont Department of Labor.

The allegation is of misrepresentation and the inappropriate collection of only $1,700 in workers' compensation benefits. The motivation was essentially "so that he could stay home from work and collect workers' compensation for months." And, some may think that words like "fraud," "millions" and similar make for good headlines.

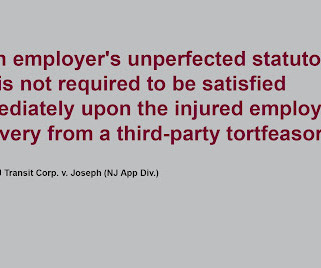

The New Jersey Superior Court, Appellate Division, ruled that a third-party lien can remain unresolved until the workers’ compensation claim is adjudicated. Joseph filed a workers’ compensation action against NJ Transit and a third-party action against the tortfeasor involved in the accident (the “underlying action”). NJ Transit).

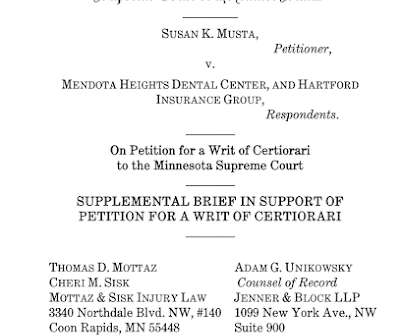

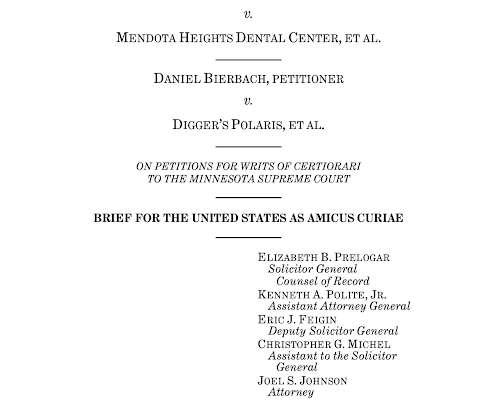

The US Supreme Court (SCOTUS) declined to review the Minnesota Supreme Court’s decision prohibiting reimbursement of medical marijuana costs in a workers’ compensation claim. Therefore, the individual States will remain the authority on whether reimbursement for medical marijuana will be permitted in a workers' compensation claim.

Request a loss run report by contacting your insurance broker so they can get in touch with your insurancecarrier or ask your insurance company directly. You may even be able to request a loss run online if your insurance broker or company has an online portal. What types of business insurance use loss runs?

Let’s say you want to provide dental and vision insurance for your employees. You bring this up to your PEO, but the insurancecarriers they work with don’t offer dental or vision insurance, so there’s little you can do about it.

Various forms of legislation have been proposed, including the Worker Health Coverage Protection Act and the American Rescue Plan Act. The employer would be responsible for working with insurancecarriers to pay monthly invoices. Both are currently under review by Congress, with a decision expected as early as next week.

Below are the five steps to take after your worker gets injured on the job: 1. For instance, you should go to the accident scene with the safety officer to take the injured worker to a safe area and ask the other employees to clear the vicinity. File A Workers’ Compensation Claim. Investigate The Accident.

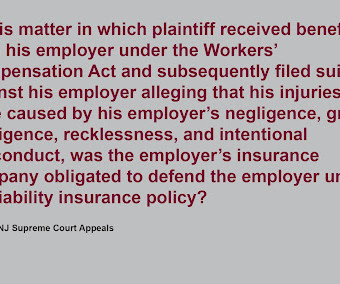

The NJ Supreme Court will review whether a workers’ compensation insurance company has a duty to defend an employer against personal injury claims brought by the employer’s employee under an employer's liability insurance policy. The insurance company denied coverage based on the policy's "Employer's Liability EII exclusion."

District Court for the District of Colorado, the Supreme Court of Colorado held that an employee who receives workers’ compensation benefits for injuries caused by an underinsured third-party tortfeasor is not barred from pursuing further recovery from his or her employer’s UM/UIM insurer [ Klabon v. Defendant: Travelers Prop.

The construction industry is currently experiencing a deficit of skilled workers. This can translate into more expensive home insurance claims for insurancecarriers – and higher premiums for homeowners. Work with an Insurance Broker. Low Housing Inventory.

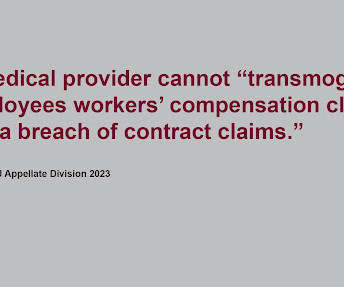

FACTS Five workers employed in the State of New York suffered work-related injuries in NY while working for a NY employer. They were treated in a NJ hospital that obtained assignments for medical costs from the patients against the workers’ compensation carrier of the NY employer. Port Authority of N.Y. and N.J. ,

The COVID-19 pandemic and all the stressors placed on workers during this tumultuous time have highlighted how critical mental health , work-life balance and overall wellbeing are. Often, this type of tool is available via your company’s health insurancecarrier.

Workers’ Compensation Claim The Academy’s insurancecarrier denied the claim. The Court added that, as the insurancecarrier explained in its brief, the CAB discounted the treating physician’s opinion because the doctor did not opine that the claimant “actually contracted MRSA at work.”

Your call might involve benchmarking, a review or your culture, workers preferences, surveying employee opinion on benefit choices, and understanding the cost sharing structure that you currently offer to your team – which can drive net costs to you as an employer. There’s no additional charge for our services. Call or email us.

Various federal and state laws apply, including your state’s workers’ compensation rules, the FMLA and the ADA. Workers’ compensation absences. Employees who are injured at work are eligible for workers’ compensation benefits. For example, many injured workers can perform other work while recovering.

The US Supreme Court (SCOTUS) is scheduled to conference the Minnesota Supreme Court’s decision prohibiting reimbursement of medical marijuana costs in a workers’ compensation claim. The petitioner further argues that Minnesota’s workers’ compensation system does not facilitate access to marijuana. 801 et seq.,

The case involved a worker who was injured when opening an electrical panel in the course of his employment. ORDER NOW Gelman on Workers' Compensation Law 3rd Ed. The exclusion is embodied in the Employer’s Liability EII exclusion.” Superior Court of New Jersey, Appellate Division. 2024 Update In Press.

The US Government filed an amicus curiae brief requesting that the US Supreme Court (SCOTUS) not review the Minnesota Supreme Court’s decision prohibiting reimbursement of medical marijuana costs in a workers’ compensation claim. The US Government was invited to submit a brief by SCOTUS. Mendota Heights Dental Center, et al., 801 et seq.,

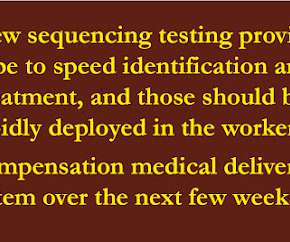

A recent study provides a potential opportunity for employers and insurance companies to reduce their risk exposure through early sequencing and treatment proactively. Background The workers’ compensation system faces an enormous challenge in 2022 as the novel consequences of the most recent surge of SARS-CoV-2 infection engulf the nation.

While electric cars generally require fewer repairs than gas-powered vehicles, the cost of replacement parts and labor for EVs can be higher due to the need for specialized worker training, scarcity of parts and potential supply chain issues. Remember, bundling discounts can differ among insurancecarriers.

Background Connelly was a passenger in a vehicle driven by her co-worker Trezona during the course and scope of their employment when Trezona negligently caused an accident, injuring Connelly. Both companies denied the claim, maintaining Connelly’s exclusive remedy lay with the the Act. Smallwood , 308 S.C. 471, 419 S.E.2d

As a co-employer, the PEO you choose will ultimately take responsibility for payroll processing, providing workers’ compensation insurance coverage, providing an employee benefits package and a host of other sensitive human resources (HR) and administrative tasks. What carriers or third-party administrator (TPA) does the PEO use?

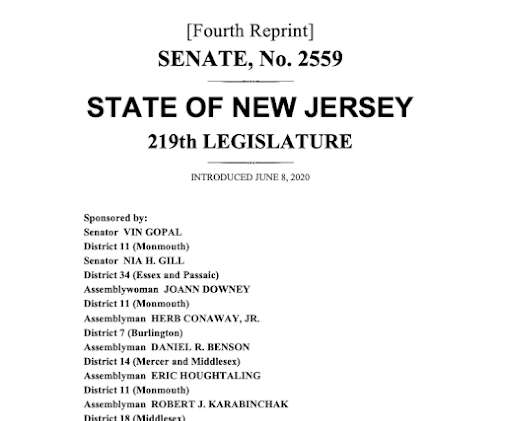

The legislation also permanently prohibits insurancecarriers from imposing geographic or technological restrictions on the provision of telehealth services, as long as the services being provided meet the same standard of care as if the services were delivered in person. Recommended Citation: Gelman, Jon L.,

Workers’ Comp. Since the employer’s outlay for workers’ compensation benefits exceeded the $150,000 held in escrow, all the funds (after payment of litigation expenses) had to be paid over to the employer. According to Claimant, the employer’s accrued workers’ compensation lien in the amount of $327,861.85, represented 17.3

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content