This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

After you subtract all of the taxes and other deductions, money left over is considered take-homepay. Read on to learn more about what is take-homepay and how to calculate it. What is takehomepay? Take-homepay may also be called net pay.

Options can include: Health insurance, Voluntary benefits premiums (like vision and dental), Life insurance, 401(k), and. Besides the fact that your employees use money that hasn’t been taxed to pay for these benefits, the payroll deductions for them also reduce their taxable income while raising take-homepay.

The MyHealthcare benefits package was launched as part of the health insurance provider’s global ambition to enhance health benefits for all of its employees. It is available from day one of employment for permanent staff and is cost-free due to the tax benefit being paid on their behalf, so as to not impact their take-homepay.

Financial resiliency is enhanced with financial resources, such as savings, health insurance, and a good-paying job. Below are five examples: ¨ Maintain a Low Debt-to-Income Ratio- Keep monthly consumer debt payments (all debts except a mortgage) at 15% or less of monthly take-homepay.

Employees can save an average of 30% in federal, state and local taxes on items they already pay for out of pocket. Because these benefits are free from federal and state income taxes, an employee’s taxable income is reduced, which increases the percentage of their take-homepay.

For example, if you make $50,000 a year, your biweekly gross pay over 26 pay periods is $1,923.07, minus any deductions like health insurance, 401(k) contributions and taxes. But in a year with 27 pay periods, your biweekly gross pay would be $1,851.85 – a reduction of $71.22 (3.7%) per pay period.

Here, to help you with your finances this year, we’re sharing the key things you need to be aware of, and the three actions you should be taking. The prime minister has announced that national insurance (NI) will increase in April to help fund the health and social care sector. . The 2022 NI increase .

This means people can earn £12,500 tax-free, and only start paying tax on income over that amount. However, if they have any other form of income, get benefits-in-kind from their employer (health insurance, life insurance or a company vehicle etc) or claim tax relief for any other reason, it will affect this tax code.

Insurance market support services provider PoloWorks is rolling out new benefits technology to increase employee engagement with benefits and enable them to access all options in a single location. The platform, which is provided by Zest, will be rolled out in November.

“Benefits that can greatly reduce financial burdens and improve financial wellbeing, such as cashback schemes and greater access to financial resources to help budget, can be helpful to stretch take-homepay as much as possible,” she says.

Even with health insurance, labor and delivery can cost around $5,000, and without insurance, it can be upwards of $40,000. Since we had contributed pre-tax to our HSA before birth our takehomepay was lower. Most insurance plans give you a certain period (often 30 days) to add your baby onto your plan.

Net Pay contributions from your employees is deducted before tax. While there’s no tax relief here, your employee will end up paying less in National Insurance and will notice an increase in their take-homepay. This could still be seen as a tax benefit. If this appears complicated, don’t fret.

Credit: Hyejin Kang/Shutterstock Need to know: Employers should start planning now for the P11D changes to the reporting and paying of tax and Class 1A national insurance contributions (NICs) on benefits in kind, to ensure a smooth transition to the new system in April 2026.

Caution: actual compensation in any state may be limited by statutory maximum insurable average earnings or maximum weekly benefit provisions. The calculation can be complex and depends largely on the taxation rate, number of exemptions, and contribution or premium rates for social insurance and other mandatory deductions.

Here’s an overview of the UK Budget announcement, there are two key areas of focus: National Insurance Contributions cuts: costing around £10 billion. Understand the implications of any changes in income tax rates or allowances on your take-homepay.

For example, some white-collar employees have said that they would willingly give up a portion of their salary if they could keep a work-at-home option. . Many hourly workers toiled long hours and endured health risks for low take-homepay. For lower-paid workers, money became a critical bottom line during the pandemic.

Like a lot of workers in the tourism sector, she relies on unemployment insurance when there is no work. Aidy’s claim for temporary total disability was accepted by the workers’ compensation insurer. of her average Net earnings—about $31 less per week than her average takehomepay.

The cost of healthcare can be daunting, especially for those who do not have adequate insurance coverage or savings to cover medical expenses. FSAs, on the other hand, allow for pre-tax contributions, reducing your taxable income and increasing take-homepay. What is an HSA?

In his Autumn Statement last November, Chancellor Jeremy Hunt extended the freeze on national insurance (NI) and income tax rate thresholds until April 2028. This can contribute to fiscal drag, which occurs when taxpayers are ‘dragged’ into paying tax, or a higher tax rate. This could add further strain to employees.

Open enrollment gives employees a small window of time to enroll in, withdraw from, or make other changes to their medical, dental, vision, disability, and life insurance coverage. However, if most of the employees are older and nearing retirement, you might discuss life insurance more. This isn’t a one size fits all process.

Now is the time to let folks know that you offer flex scheduling, work from home opportunities, a robust health insurance offering, higher than average paid time off, and a slew of other perks that make working for your company seriously compelling.

They were first resistant to escalation, fearing that they would go too far and substantially reduce employees’ take-homepay. Insurance services are offered through HUB International, an affiliate. Many of them wanted to start withholding at 3% or even 2% of compensation.

They can range from health insurance coverage to retirement plans, flexible spending accounts, transportation benefits, education assistance, and more. By reducing the taxable portion of their income, employees can effectively increase their take-homepay. Let's explore some of the most common ones: 1.

Here’s some information that may help you identify your company’s and employees’ medical insurance wants and needs. Employees aren’t going to opt in to a medical plan that cuts far into their take-homepay. Health Care Costs. Establish a budget. But you’re not the only one with a budget. PPOs vs HMOs.

Insurance types: Medical, dental, vision, disability, and life insurance plans. The most expensive benefit to offer is health insurance. For an individual, this could cost $7,000 to $10,000 per year for total health insurance, which employers and employees often split depending on the employer’s contribution strategy.

The tax you’re targeting here is National Insurance (NI). Both employees and companies pay NI, which is calculated based on salary size and total employee payroll, respectively. This happens because lower earnings mean less NI to pay.

In a nutshell, this mechanism allows employees to maintain their pension contributions and even enjoy a slightly higher take-homepay. It’s a clever tax manoeuvre that reduces the National Insurance (NI) contributions individuals need to pay.

Health insurance, retirement savings plans and tuition reimbursement are just some of the perks included to help companies attract and retain talented individuals. Not all workers take full advantage of their benefits, however. Have HR personnel explain how elective benefits would impact a worker’s take-homepay.

A POP Plan gives employees the chance to set aside pre-tax money from their paycheck (like an FSA) but it pays for the premium costs associated with employer-provided health insurance. This is a popular cafeteria plan option. Dependent Care Account.

A POP Plan gives employees the chance to set aside pre-tax money from their paycheck (like an FSA) but it pays for the premium costs associated with employer-provided health insurance. This is a popular cafeteria plan option. Dependent Care Account.

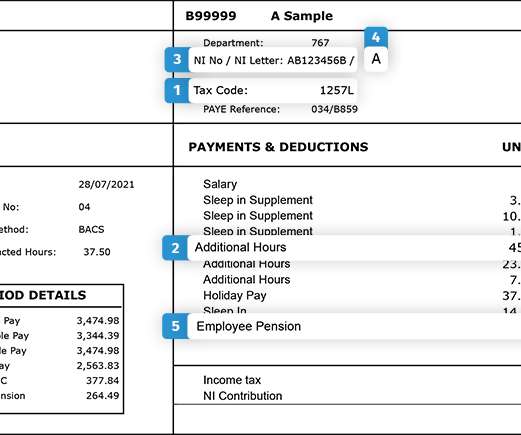

Every payslip must show an employee’s total or gross pay, their net or take-homepay, any deductions or payments, and list any variable hours that have been worked. And, if they don’t fully understand exactly what they are looking for, then they should speak to their line manager in the first instance.

“Benefits that can greatly reduce financial burdens and improve financial wellbeing, such as cashback schemes and greater access to financial resources to help budget can be helpful to stretch take-homepay as much as possible,” she says.

In fact, according to our research, UK workers think that inflation will soon pass 8% as a result of a number of factors including the Covid-19 pandemic, rises in national insurance (NI) contributions, unrest in Eastern Europe, and soaring energy prices. Salary sacrifice.

Step 6: Cash Talks Take into account wages in the industry and location and calculate salaries. Throw in benefits such as housing, transport, and insurance, staying true to the employment contract and UAE laws and regulations. If it’s outside the normal workday, you pay 1.26 Check out the market for similar positions.

Employees can contribute as much as they wish as long as it does not take their take-homepay below the minimum wage. Group income protection employer-paid for all employees, subject to acceptance by the insurer. Combined business travel/personal accident/sickness insurance policy, employer paid for all employees.

High Deductibles Are Nothing to Be Afraid Of Everybody — except maybe insurance providers and well-informed HR professionals — hates deductibles, which is why whoever came up with the term “high-deductible health plan” did the employees of America a grave disservice.

Payments come out of an employees gross salary before PAYE and National Insurance, meaning they pay less tax, and your business saves on Employer National Insurance contributions. By opting to contribute a portion of their pre-tax salary into their pension, they can enjoy immediate tax and National Insurance savings.

The increase in the price of insurance premiums and credit card interest has also added to the expenses that individuals are expected to account for. Compared to 2019, we are now witnessing a 10% increase in the number of Americans living paycheck to paycheck.

Use Total Compensation Statements to Highlight Value Employees often underestimate the full value of their compensation package, focusing solely on their take-homepay. Providing total compensation statements can bridge this gap by detailing all the benefits and perks employees receive.

Traditionally, employee benefits were limited to necessities like health insurance, retirement plans, and paid leave. With Empuls, you can: Deliver tax-free fringe benefits like fuel reimbursements, meal cards, LTA, and more—helping employees maximize their take-homepay.

How much are your basic monthly living expenses, including food, shelter, health insurance, transportation, childcare? Add up all of these expenses to understand whether you’re spending more, less or the same as your take-homepay each month. How much cash can you get your hands on quickly, if you need it?

Here are the five most common misconceptions about health savings accounts: Myth #1: An HSA Is Just Another Healthcare Headache For better or worse, getting a health insurance claim paid can often involve jumping through a series of administrative hoops verifying coverage, securing referrals, requesting pre-approval, and so on.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content