This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Below are five examples: ¨ Maintain a Low Debt-to-Income Ratio- Keep monthly consumer debt payments (all debts except a mortgage) at 15% or less of monthly take-homepay. Example: $275 of debt payments ÷ $2,500 of net pay equals a consumer debt-to-income ratio of 11% (275 divided by 2,500).

Options can include: Health insurance, Voluntary benefits premiums (like vision and dental), Lifeinsurance, 401(k), and. Besides the fact that your employees use money that hasn’t been taxed to pay for these benefits, the payroll deductions for them also reduce their taxable income while raising take-homepay.

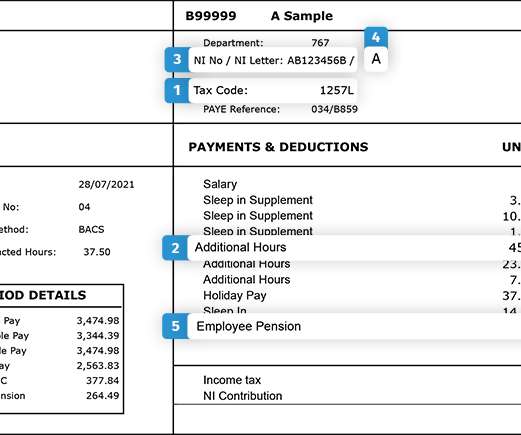

This means people can earn £12,500 tax-free, and only start paying tax on income over that amount. However, if they have any other form of income, get benefits-in-kind from their employer (health insurance, lifeinsurance or a company vehicle etc) or claim tax relief for any other reason, it will affect this tax code.

Open enrollment gives employees a small window of time to enroll in, withdraw from, or make other changes to their medical, dental, vision, disability, and lifeinsurance coverage. However, if most of the employees are older and nearing retirement, you might discuss lifeinsurance more.

Insurance types: Medical, dental, vision, disability, and lifeinsurance plans. This can help employees see things they may not consider when they think of just take-homepay. In this article, we’ll look at: The benefits most businesses offer. How much of an employee’s salary is made up of benefits.

Employees can contribute as much as they wish as long as it does not take their take-homepay below the minimum wage. Combined business travel/personal accident/sickness insurance policy, employer paid for all employees. Lifeinsurance for all employees with a death-in-service benefit of four-times salary.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content