This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Below are six take-aways about some recent seminars that I attended about longevity risk: Ticking Time Bomb - One speaker called longevity risk a “ticking time bomb” in financial planning. For example, instead of two Social Security checks, there will be one, along with a reduced (survivor) pensionbenefit.

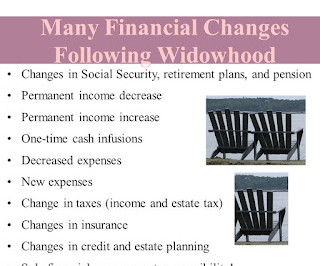

This post describes five changes in income and expenses that widowed persons can expect: Reduced Income - I heard this example at a recent seminar. If the husband dies first, the wife is left with $1,250 (50% of husband’s pension), $800-wife’s pension, and $2,000 (highest Social Security) for income of $4,050 ($48,600 annually).

Empower employees with financial education Whilst some information may be provided via a website or leaflet, actually attending an interactive financial education workshop about pension options and retirement income options is far more engaging.

From April 2023, the LTA charge was removed and pensionbenefits have been taxed as income with no additional penalty since then, but the formal abolition of the LTA required a raft of new legislation which is now complete, so this will take place from April 2024.

Not a week goes by that I dont receive colorful tri-fold invitations to free meal seminars for investments and preplanned burials and cremations. Below are five Barbservations about the seminar format, content, and take-aways: You Will Get Hungry- I typically eat dinner around 6:30 pm, which is when the presentation was slated to start.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content