This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Whilst reducing contributions now would make relatively small savings each month, the impact on retirement savings in later life will be dramatic, due to lost employer contributions and tax relief.” It’s therefore more important than ever to ensure employees are engaged with their pensions.

Below are six take-aways about some recent seminars that I attended about longevity risk: Ticking Time Bomb - One speaker called longevity risk a “ticking time bomb” in financial planning. They must cope with issues such as lower trigger amounts for taxes on Social Security and Medicare and reduced guaranteed income.

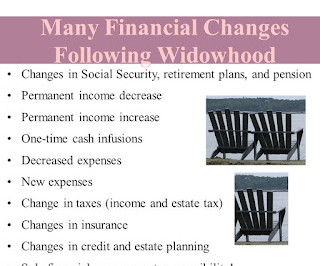

This post describes five changes in income and expenses that widowed persons can expect: Reduced Income - I heard this example at a recent seminar. If the husband dies first, the wife is left with $1,250 (50% of husband’s pension), $800-wife’s pension, and $2,000 (highest Social Security) for income of $4,050 ($48,600 annually).

Employers will need to review policies for employees who previously opted out of the pension scheme because they may have been close to the lifetime allowance. Two new limits will be introduced in April to control tax relief on pension lump sums. Some employers offered a cash benefit instead of a pension contribution.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content