This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

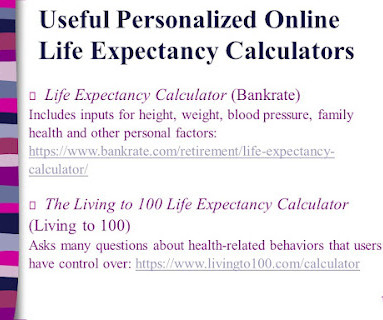

Below are six take-aways about some recent seminars that I attended about longevity risk: Ticking Time Bomb - One speaker called longevity risk a “ticking time bomb” in financial planning. For example, instead of two Social Security checks, there will be one, along with a reduced (survivor) pension benefit.

So far, it has been delivered to approximately 80,000 of its UK employees. Kerry Shiels, pension and benefits director at BT, says: “It is very important that employees understand their BT pension and the retirement decisions they will need to make in the lead up to, and at, retirement. before financial education, to 4.1

Need to know: Employers can tailor content and communication channels to different employee groups to help with their pensions knowledge. Losing the jargon will make the language of pensions easier to understand and more relevant to staff. They could invest in financial coaching for a more personal approach to pensions education.

Below are some key things to know about annuities from a recent seminar that I attended: Complexity- Annuities are often sold as a “simple” investment but, in reality, they can be quite complicated. They are often bought with money from settlements, investment accounts, and pension plan lump sum distributions.

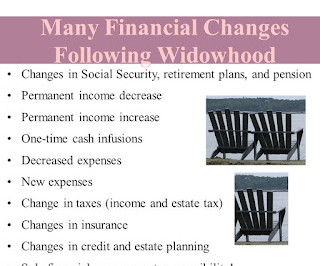

This post describes five changes in income and expenses that widowed persons can expect: Reduced Income - I heard this example at a recent seminar. If the husband dies first, the wife is left with $1,250 (50% of husband’s pension), $800-wife’s pension, and $2,000 (highest Social Security) for income of $4,050 ($48,600 annually).

Given cost of living worries and the notion this may be impacting pension savings, WEALTH at work conducted research* with employees to find out their thoughts into what’s happening in reality. It’s therefore more important than ever to ensure employees are engaged with their pensions.

I recently attended a seminar about financial concerns facing women in retirement. pension, Social Security, annuities, dividends/capital gains, full- or part -time employment, self-employment) minus fixed (e.g., Baby Boomers were “guinea pigs” for the use of 401(k)s, often as a substitute for defined benefit pensions.

Credit: Dilok Klaisataporn/Shutterstock Need to know: Significant amounts of money are tied up in small pension pots, many of which may have been forgotten. The Pensions Tracing Service can help people reconnect with lost pensions. Employers can help staff with this process and engage with pensions more generally.

It is generally acknowledged that, despite the success of pensions auto-enrolment , saving the minimum contribution levels will not lead to a comfortable standard of living in retirement. Pensions can also seem too abstract to think about. The complexity of pensions and lack of financial education is another factor, Blake adds.

Suez works closely with works councils, and pensions is always on the agenda as there is regular demand for higher employer contributions. So I wanted to find a way to prove that we as a business were getting value for money from that pension scheme and that it in turn provided value to members.”. “So That’s real value for money.”

Credit: Natata/Shutterstock Need to know: The abolition of the pensions lifetime allowance in April will require an overhaul of employee communications, and a revaluation of pension scheme design and administration, including opportunities to simplify the scheme and reduce the cost of running it.

This is still an option today; for example, most pension providers will be able to provide information or even workshops to help employees understand their retirement savings and the products on offer to them via their employer. This means speaking with existing providers, such as for pensions, and discovering what they can offer.

It offers pre-retirement seminars focusing on a holistic approach to pensions , tax implications, the psychological impact of leaving work, wills and estate planning, that are primarily aimed at older workers but do get interest from younger staff as well.

A fifth (20%) of defined contribution (DC) pension schemes continue to report increases in members opting out or reducing contributions, according to research by Aon. A number of respondents have reported that they provide a range of seminars to support members.

Most of us spend the majority of our working life saving into our pension. However, all this hard work saving can quickly unravel for those who aren’t aware of common pension mistakes. WEALTH at work outlines below the top 10 pension mistakes individuals could make, to highlight what employees facing retirement may need support with.

I used to get invites to free meal seminars when I lived in New Jersey (after I turned 50) but they all say “No brokers, agents, or advisors.” Since few people in Florida know that I am a financial educator, I decided to go “undercover” to observe the seminar content, presentation style, and participants.

Offer a range of support The REBA research reveals that pensions still dominate employers’ financial wellbeing support, with 76% of employers having rated their support for retirement saving as ‘very good’ or ‘fair’, compared with just 37% of organisations that rated their support for building a financial safety net as ‘very good’ or ‘fair’.

The Integrated Benefits Institute during an annual forum recently held a session highlighting what some employers are doing to educate their workers on how to manage diabetes: The San Francisco Municipal Transportation Agency has partnered with the American Diabetes Association to deliver educational seminars on diabetes to its workforce.

After the seminars, employees have access to a microsite where they can review highlights of the session that they attended, book onto future seminars and keep up-to-date with the latest news articles. Following on from this session, I would like to contribute more to my pension pot.” “The

In February 2020, the Money and Pension Service (MAPS) rolled out a 10-year strategy for financial wellbeing , which identifies workplaces as a key channel through which the UK can become financially healthier. Pensions . The UK government is certainly hoping employers will intervene in this area. Salary sacrifice schemes .

Making regular contributions into a pension pot is also becoming more of a challenge, with salaries struggling to keep pace with rising costs. WEALTH at work’s research showed that 13% of employees have reduced or stopped their pensions because of rising costs. You can also see their comments below.

Employees can also participate in bespoke financial wellbeing workshops, featuring guides, webinars and in-person seminars on topics such as pensions and protection, budgeting , saving and investing.

Events impacting pay, financial wellbeing and pensions. In terms of pensions, employers will be looking at how to position them to staff without a disposable income and how they can use their budget to support staff with retirement benefits if they cannot put it towards pay.”. The cost-of-living payments that we’ve seen will continue.

This has included seminars for all employees on World Menopause Day and the launch of a menopause policy, as well as training for senior management. We recognise that true inclusion is a journey, but we are proud to be officially accredited for everything that has been accomplished so far.”

Many leading employers work with workplace specialists to deliver financial education and guidance programmes to help their employees achieve better financial outcomes, whether it is support with making investment decisions to build savings or accessing a pension for the first time.”

401(k) plans, pensions, and employer contributions to retirement accounts are increasingly important to young workers. Those born after 1982 have lived through multiple recessions and have seen their Social Security safety net plundered to cover government mismanagement and overspending. It’s a touchy subject.

From ensuring they have a good amount of money going into their pension to providing career prospects for them to climb the career ladder. It is the employer’s responsibility to work with the government and their employees to create a decent pension plan, but that isn’t the only way you can help them with their retirement.

Benefits: In an age of rising health and pension costs, Human Resources is the go-to source for smart sourcing of insurance and retirement solutions. Training and development: Gone are the days when bosses called up HR to say the company needed more technical training, sexual harassment classes or career development seminars.

Benefits: In an age of rising health and pension costs, Human Resources is the go-to source for smart sourcing of insurance and retirement solutions. Training and development: Gone are the days when bosses called up HR to say the company needed more technical training, sexual harassment classes or career development seminars.

Here are some examples: Structured learning: eLearning courses In-person training Structured, recorded 1-2-1 conversations Professional qualifications Unstructured learning: Online seminars and webinars (like Ciphr’s series of HR webinars ) Reading Research Coaching or mentoring How FCA compliance and regulatory training courses from Ciphr can help (..)

One in six (17%) has made further ‘savings’ by cutting back (or cancelling) their personal insurance cover, such as income protection, life insurance, and medical or dental insurance, and one in seven (14%) has reduced their pension contributions – decisions which may prove to have costly consequences in the future.

Some employers offer financial planning services or seminars on topics such as budgeting, investing, and retirement planning. National pension scheme (NPS) The national pension scheme is a voluntary retirement savings scheme where employees can contribute towards their retirement savings.

Not a week goes by that I dont receive colorful tri-fold invitations to free meal seminars for investments and preplanned burials and cremations. Below are five Barbservations about the seminar format, content, and take-aways: You Will Get Hungry- I typically eat dinner around 6:30 pm, which is when the presentation was slated to start.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content