This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

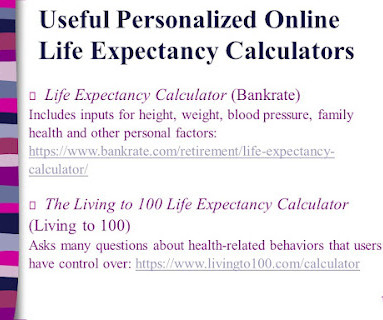

Below are six take-aways about some recent seminars that I attended about longevity risk: Ticking Time Bomb - One speaker called longevity risk a “ticking time bomb” in financial planning. They must cope with issues such as lower trigger amounts for taxes on Social Security and Medicare and reduced guaranteed income.

Below are some key things to know about annuities from a recent seminar that I attended: Complexity- Annuities are often sold as a “simple” investment but, in reality, they can be quite complicated. Three Types- Fixed annuities are like CDs, only tax-deferred, and guarantee a certain interest rate for a specified time period.

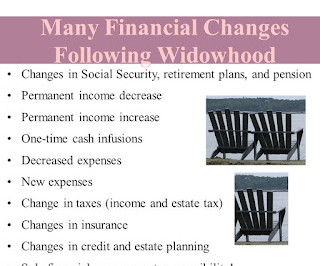

This post describes five changes in income and expenses that widowed persons can expect: Reduced Income - I heard this example at a recent seminar. If the husband dies first, the wife is left with $1,250 (50% of husband’s pension), $800-wife’s pension, and $2,000 (highest Social Security) for income of $4,050 ($48,600 annually).

So far, it has been delivered to approximately 80,000 of its UK employees. Kerry Shiels, pension and benefits director at BT, says: “It is very important that employees understand their BT pension and the retirement decisions they will need to make in the lead up to, and at, retirement. before financial education, to 4.1

Need to know: Employers can tailor content and communication channels to different employee groups to help with their pensions knowledge. Losing the jargon will make the language of pensions easier to understand and more relevant to staff. They could invest in financial coaching for a more personal approach to pensions education.

Given cost of living worries and the notion this may be impacting pension savings, WEALTH at work conducted research* with employees to find out their thoughts into what’s happening in reality. It’s therefore more important than ever to ensure employees are engaged with their pensions.

I recently attended a seminar about financial concerns facing women in retirement. pension, Social Security, annuities, dividends/capital gains, full- or part -time employment, self-employment) minus fixed (e.g., Baby Boomers were “guinea pigs” for the use of 401(k)s, often as a substitute for defined benefit pensions.

This is still an option today; for example, most pension providers will be able to provide information or even workshops to help employees understand their retirement savings and the products on offer to them via their employer. This means speaking with existing providers, such as for pensions, and discovering what they can offer.

Credit: Natata/Shutterstock Need to know: The abolition of the pensions lifetime allowance in April will require an overhaul of employee communications, and a revaluation of pension scheme design and administration, including opportunities to simplify the scheme and reduce the cost of running it.

Below is a list of participants’ six most frequently mentioned concerns and suggested action steps from my class: Taxes in Retirement ¨ Hold assets (e.g., Below is a list of participants’ six most frequently mentioned concerns and suggested action steps from my class: Taxes in Retirement ¨ Hold assets (e.g.,

It offers pre-retirement seminars focusing on a holistic approach to pensions , tax implications, the psychological impact of leaving work, wills and estate planning, that are primarily aimed at older workers but do get interest from younger staff as well.

Most of us spend the majority of our working life saving into our pension. However, all this hard work saving can quickly unravel for those who aren’t aware of common pension mistakes. WEALTH at work outlines below the top 10 pension mistakes individuals could make, to highlight what employees facing retirement may need support with.

After the seminars, employees have access to a microsite where they can review highlights of the session that they attended, book onto future seminars and keep up-to-date with the latest news articles. Following on from this session, I would like to contribute more to my pension pot.” “The

Employees can also participate in bespoke financial wellbeing workshops, featuring guides, webinars and in-person seminars on topics such as pensions and protection, budgeting , saving and investing.

Deductibles can be paid with tax-advantaged/tax-free spending accounts funded by employees and employers. It’s also worth noting that some fringe benefits are tax-deductible for employers depending on how much value they add to an employee’s compensation package. Let IRS Publication 15-B be your tax guide to fringe benefits.

In February 2020, the Money and Pension Service (MAPS) rolled out a 10-year strategy for financial wellbeing , which identifies workplaces as a key channel through which the UK can become financially healthier. Pensions . The UK government is certainly hoping employers will intervene in this area. Salary sacrifice schemes .

Events impacting pay, financial wellbeing and pensions. In terms of pensions, employers will be looking at how to position them to staff without a disposable income and how they can use their budget to support staff with retirement benefits if they cannot put it towards pay.”. The cost-of-living payments that we’ve seen will continue.

Some employers offer financial planning services or seminars on topics such as budgeting, investing, and retirement planning. 7 Tax-saving benefits for employees There are several tax-saving benefits available for employees that can help reduce their tax liabilities. In addition, an additional tax deduction of up to rs.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content