This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

About 1,000 Unite union members working at two Morrisons warehouses have undertaken strike action for three days over a cut in company contributions to their pensions. Unite also claims Morrisons is ditching a long service pay award and increasing the speed at which goods are expected to be processed in warehouses.

Transitioning to a superior provider is no longer a hassle: If you’re contemplating changing your current workplace pension scheme, the process isn’t as challenging as you might think. Many pension companies (we’re one of them!) What is a workplace pension? are prepared to assist you with the heavy lifting.

However, many don’t realise the significant difference a small increase to their pension savings can make. For example, someone in their 20s, saving an extra 1% a year with their employer matching this, may be able to increase their pension pot in retirement by 25%. They are all 25 years old and plan to retire at age 68.

The benefits on offer at Wave: Pension A master trust pension scheme for all employees. Employees can contribute as much as they wish as long as it does not take their take-homepay below the minimum wage. Age limits are 16 to state pension age. Age limits are 16 to state pension age.

This, for example, means an individual earning £30,000, with a net takehomepay of £23,112, will see this take-home figure decrease by £255. . It is crucial to build healthy financial habits that will help minimise the impact once the NI hike takes place this year. Hunt down lost pension pots.

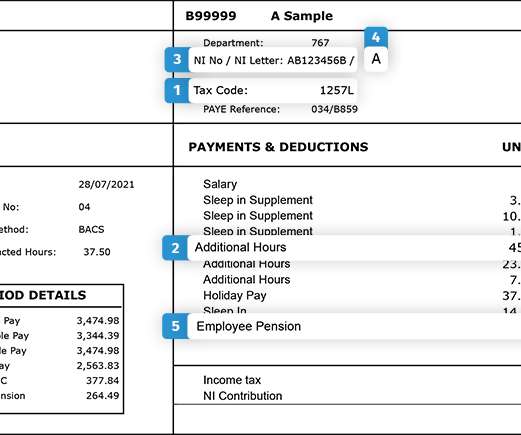

Tax codes can, and do, change, particularly if there’s been a change of personal circumstances, such as people getting married, claiming taxable state benefits, or working from home. For the 2021/22 tax year (and through to 2025/26), the tax code for most people under 65 who only have one job or pension is 1257L.

You’ve got a company pension scheme in place, so what would prompt you to change it? However, there’s a strong reason to do so: your business and employees may be at risk if you don’t take action. Additionally, shifting to a modern digital pension provider is surprisingly straightforward.

Software can allow employees to model the impact on their take-homepay of opting into certain benefits, for example, or changing their pension contribution. Fowler says giving people quick and easy access to payroll information allows them to feel in control and drives engagement.

. “The concept of nudging, applied in an ethical, sustainable and scalable way, represents one of the largest untapped opportunities in HR management” Think back to when employees had to sign up to the company pension scheme. But it left these employees with only the state pension waiting in retirement. million by 2016.

Colleagues can access information about everything on offer, as well as self-serve additional salary sacrifice options such as additional pension contributions, family private medical insurance, holiday purchase and cycle to work, and instantly see how this will impact their takehomepay.

The retailer has additionally increased minimum pay rates , which will rise to £11.50 Over the past three years, Currys has increased its minimum hourly pay by 29%. This increase in take-homepay will mean that the annual earnings of an employee who works 20 hours a week will have risen by nearly £2,700 over the three-year period.

As an employer, you’re obliged to provide your staff with a workplace pension – a mandate made compulsory by the UK government in 2012. Unfortunately, a considerable number of employees adopt a ‘set and forget’ approach once they’re enrolled in a pension scheme. So, why not ensure it delivers real value?

WILL MAINTAIN MOMENTUM ON AUTO-ENROLLMENT After the passage of the Pension Protection Act of 2006, some plan sponsors resisted auto-enrollment, concerned that they would be seen as too controlling in their employees’ lives. Employees may opt out of auto-enrollment and auto-escalation. SECURE ACT 2.0

Jeanette Makings, head of workplace financial wellbeing at Close Brothers Asset Management, says: “Employees will need help understanding the impact in relation to their take-homepay. Providing a robust financial wellbeing programme can empower employees to take action and build their financial resilience, says Stinton.

Pay: real living wage, and salary increases. Pensions contributions. Pay: real living wage, and salary increases. Pensions contributions. Pensions are designed to provide money for employees’ retirement and are one of the most popular and widely available benefits. Financial wellbeing assistance. Salary sacrifice.

Employees who get into financial distress are likely to opt out from benefits, even important ones like pensions or healthcare, to boost their takehomepay,” he explains. The current cost-of-living crisis is a good example of this, says Chris Priebe, chief executive officer (CEO) and founder of Zelt.

Your business fronts the cost of leasing an electric car, and the employee pays you back over a set period of time. Workplace Pensions A great way to boost your employees pension pots! By opting to contribute a portion of their pre-tax salary into their pension, they can enjoy immediate tax and National Insurance savings.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content