This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Transitioning to a superior provider is no longer a hassle: If you’re contemplating changing your current workplace pension scheme, the process isn’t as challenging as you might think. Many pension companies (we’re one of them!) What is a workplace pension? are prepared to assist you with the heavy lifting.

However, many don’t realise the significant difference a small increase to their pension savings can make. For example, someone in their 20s, saving an extra 1% a year with their employer matching this, may be able to increase their pension pot in retirement by 25%. They are all 25 years old and plan to retire at age 68.

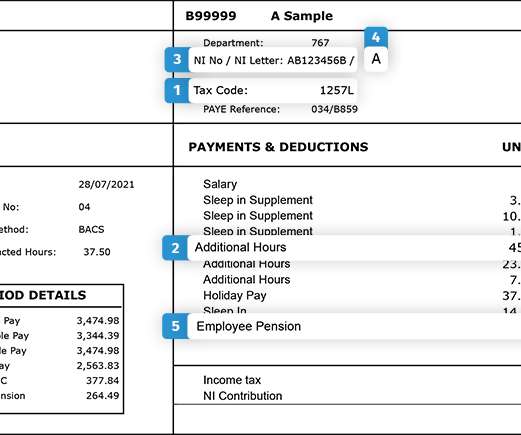

It’s worth remembering that it’s an employee’s responsibility to check they’re on the right tax code, as it impacts how much tax they pay – whether it’s too much tax or too little. For the 2021/22 tax year (and through to 2025/26), the tax code for most people under 65 who only have one job or pension is 1257L.

You’ve got a company pension scheme in place, so what would prompt you to change it? However, there’s a strong reason to do so: your business and employees may be at risk if you don’t take action. Additionally, shifting to a modern digital pension provider is surprisingly straightforward.

As an employer, you’re obliged to provide your staff with a workplace pension – a mandate made compulsory by the UK government in 2012. Unfortunately, a considerable number of employees adopt a ‘set and forget’ approach once they’re enrolled in a pension scheme. So, why not ensure it delivers real value?

The frozen tax thresholds could see some employees ‘dragged’ into paying more tax and have less disposable income as a result. In his Autumn Statement last November, Chancellor Jeremy Hunt extended the freeze on national insurance (NI) and income tax rate thresholds until April 2028.

WILL MAINTAIN MOMENTUM ON AUTO-ENROLLMENT After the passage of the Pension Protection Act of 2006, some plan sponsors resisted auto-enrollment, concerned that they would be seen as too controlling in their employees’ lives. Employees may opt out of auto-enrollment and auto-escalation. SECURE ACT 2.0

Pay: real living wage, and salary increases. Pensions contributions. Pay: real living wage, and salary increases. Pensions contributions. Pensions are designed to provide money for employees’ retirement and are one of the most popular and widely available benefits. Financial wellbeing assistance. Salary sacrifice.

Whether its leveraging tax-efficient Salary Sacrifice schemes or taking a more holistic approach such as flexible working, its definitely possible to offer great benefits while boosting your bottom line. Your business fronts the cost of leasing an electric car, and the employee pays you back over a set period of time.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content