This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I recently attended a local estate planning seminar geared for- and marketed to- older adults. incorrect gift tax and estate tax exemptions from 2021). I took my survey with me and left the seminar shortly thereafter when the presenter started pitching various “combo packages” for legal documents. Sadly, I found some.

Below are six take-aways about some recent seminars that I attended about longevity risk: Ticking Time Bomb - One speaker called longevity risk a “ticking time bomb” in financial planning. They must cope with issues such as lower trigger amounts for taxes on Social Security and Medicare and reduced guaranteed income.

After I left New Jersey and was no longer a recognizable figure as a financial educator for Rutgers University, I attended a few free meal seminars “undercover” in my new home state of Florida. In other words, no free meal; just the seminar…and the sales pitch. Curious as I was before, I attended 4 or 5 of these online seminars.

Below are some key things to know about annuities from a recent seminar that I attended: Complexity- Annuities are often sold as a “simple” investment but, in reality, they can be quite complicated. Three Types- Fixed annuities are like CDs, only tax-deferred, and guarantee a certain interest rate for a specified time period.

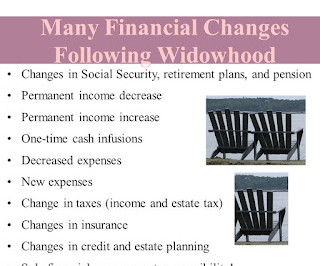

This post describes five changes in income and expenses that widowed persons can expect: Reduced Income - I heard this example at a recent seminar. Tax Considerations - Income taxes often increase for the surviving spouse, who will be filing a tax return as an individual instead of as a married couple filing jointly.

These services include HR consulting, payroll processing and tax filing, employees’ compensation insurance, safety, and risk management services, hiring across various jurisdictions, retirement vehicles, and more. They also provide leadership development training through online courses, digital books, and training seminars. .

If you’re considering setting your business apart in this way, the tax code gives you two ways to approach it — an easy way and a hard way. IRC § 127 allows you to provide up to $5,250 a year to employees in tax-free educational assistance benefits, with few strings attached. The easy way. Why is this the hard way?

This post describes tips for speaking to an attorney from a seminar that I attended that was taught by two attorneys. This situation has implications for taxes and asset transfers. Often, it is when they are older, and-perhaps-wealthier and start thinking about transferring assets. What to do?

I recently attended a seminar about financial concerns facing women in retirement. America’s 401(k) Experiment - 2023 is the 45 th anniversary of tax-deferred 401(k) retirement savings plans that workers fund with voluntary contributions from their pay. rent and car payments), variable (e.g., gas, food, and gifts), and occasional (e.g.,

While technically not a tax, IRMAA is a drag on payees’ bottom line. Tax Diversification - It is risky to put all your retirement savings in tax-deferred accounts (a.k.a., qualified plans) because you don’t know what future tax rates will be when required minimum distributions begin. tax-deferred, tax-free, taxable).

Below is a list of participants’ six most frequently mentioned concerns and suggested action steps from my class: Taxes in Retirement ¨ Hold assets (e.g., Below is a list of participants’ six most frequently mentioned concerns and suggested action steps from my class: Taxes in Retirement ¨ Hold assets (e.g.,

The German tax system operates on the federal and regional levels. The Federal Central Tax office overlooks tax payments nationwide, whereas regional offices across the country administer tax workings in different states. Everyone living in Germany has to pay tax on their earnings regardless of citizenship status.

The programme, which is provided in partnership with Wealth at Work, aims to help employees who need help understanding their options and how to implement their plan; including retirement goals and considerations, accessing retirement savings, understanding the risks, tax planning, and how to seek further guidance and regulated financial advice.

Payroll Taxes: Taxes withheld from employee paychecks, including income tax, Social Security, Medicare, and unemployment taxes, along with any contributions made by the employer. Overhead Costs: Indirect expenses associated with maintaining the workplace, such as rent, utilities, maintenance, and property taxes.

The first provides generalised resources, such as seminars or video content, educating staff on financial topics such as income tax, savings schemes, general budgeting advice, or retirement. Are there any tax or legal implications? . Now, financial education can be broken down into three tranches: education, guidance and advice.

This could be tracking the participants in: In-person meetings Seminars Workshops Benefit fairs Q&A event participation Tracking the questions and discussions in these activities can provide an understanding that other metrics cannot provide. It is not legal or tax advice.

While many companies and HR teams may be well-intentioned, there’s a difference between debt-free and tax-free. However, it’s necessary to fully understand the distinctions, before those same employees you’re trying to impress are hit with hefty taxes unexpectedly. Time for some tax ed. Read more about this here.

Take Advantage of Tax-Deferred Investments - Set up investment accounts for retirement savings where earnings can grow free of tax for decades until required minimum distributions (RMDs) must begin at age 72. Examples include traditional individual retirement accounts (IRAs), tax-deferred employer retirement plans (e.g.,

Like getting vaccinations at the hospital or paying your taxes. Organize seminars. Another way to increase employees’ participation in these programs is to organize seminars to train them. The pandemic proved once again that there are certain things in life you cannot avoid.

Whilst reducing contributions now would make relatively small savings each month, the impact on retirement savings in later life will be dramatic, due to lost employer contributions and tax relief.” This is why increasing numbers of leading employers are using either virtual or face-to-face seminars to help their employees.

It offers pre-retirement seminars focusing on a holistic approach to pensions , tax implications, the psychological impact of leaving work, wills and estate planning, that are primarily aimed at older workers but do get interest from younger staff as well.

This not only helps you keep track of how much you’ve spent and how much is left in your account, but can also be helpful when it comes time to file taxes or submit claims. Additionally, your employer may offer seminars or workshops on topics like eligible expenses, tax savings, and healthcare planning.

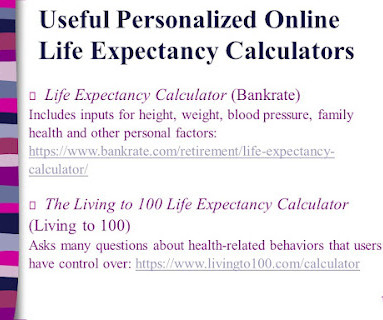

Later Life Investing Beware of “free meal seminars” that target older adults and have been linked to fraudulent or inappropriate investments. Taxes: It’s Not What You Earn, But What You Keep Consult with a CPA® or financial advisor the first tax season after leaving work to get a professionally prepared template tax return.

At every budget, there are ways institute financial wellness programming and resources, whether it be tax filing workshops or retirement planning seminars. . With the right tools and resources, companies can help employees strengthen their financial wellbeing and knowledge, simultaneously.

After the seminars, employees have access to a microsite where they can review highlights of the session that they attended, book onto future seminars and keep up-to-date with the latest news articles. Following on from this session, I would like to contribute more to my pension pot.” “The

Adrian Firth, financial education consultant at Mattioli Woods, says: “They are more likely to appreciate the benefit of tax relief and the employer contributions on top of their own payment when they can see it laid out before them.”

However, this gain meant anyone saving around £45 per month, or more, over the 3 year period could be at risk of exceeding the Capital Gains Tax Allowance (CGT) for the 2023/24 tax year of £6,000. The results The financial education seminars had a great take-up and over 82% of participants who registered for a seminar attended them.

Deductibles can be paid with tax-advantaged/tax-free spending accounts funded by employees and employers. It’s also worth noting that some fringe benefits are tax-deductible for employers depending on how much value they add to an employee’s compensation package. Let IRS Publication 15-B be your tax guide to fringe benefits.

This allows the PEO to handle functions such as payroll, benefits, tax remittance and related government filings. A PEO’s training services may also include live or virtual training seminars. As the co-employer, the PEO takes on certain, specific employer obligations, as set forth in your service agreement. Recruiting support.

Employees can also participate in bespoke financial wellbeing workshops, featuring guides, webinars and in-person seminars on topics such as pensions and protection, budgeting , saving and investing.

Accountants need to be aware of changes in tax law, sales managers need to know all the subtleties of the goods and services offered, and all marketers need to keep abreast of new promotion ways. You are unlikely to consider a three-day accounting seminar in Cyprus consistent with this principle, especially if you do not participate.

Understanding the HSA Advantage HSAs are tax-advantaged savings accounts specifically designed to help individuals save for medical expenses. HSAs offer triple tax benefits: contributions are tax-deductible, funds grow tax-free, and withdrawals for qualified medical expenses are tax-free.

Two new limits will be introduced in April to control tax relief on pension lump sums. The lifetime allowance (LTA) is the total value an individual can build up in their combined pension savings without incurring a tax charge: for most people in the tax year 2023/24 this is £1,073,100.

3): "If any party should prevail in any proceedings before a judge of compensation claims or court, there shall be taxed against the nonprevailing party the reasonable costs of such proceedings, not to include attorney’s fees." Years ago, I had a prominent workers' compensation scholar challenge the Florida statute's application at a seminar.

While this might seem simple initially, you must consider a slew of legalities and tax regulations when managing employee expense reimbursement. When you have plans to reimburse your employees, you want to ensure it’s done with an accountable plan in place so you can repay them 100% tax-free. Employee expense guidelines.

Seminars on stress relief, sleep improvement, relaxation, and work-life balance. These allow employees to save for their golden years while enjoying tax benefits now. If retirement seminars or access to free one-on-one retirement planning sessions are part of your employee benefits package , tout it! Health Savings Accounts.

HSAs empower individuals and families to be in charge of their healthcare journeys, allowing them to save tax-free dollars, roll them over year to year, and use them for eligible medical expenses whenever the need arises. The money that individuals contribute to their HSAs is tax-deductible, and the earnings on the account are tax-free.

The Tax Cuts and Jobs Act, however, changed the calculus by disallowing corporate deductions for expenses employees incur to entertain clients, customers, etc. That’s why we were intrigued by an idea purporting to allow you to skirt the Tax Cuts and Jobs Act’s 100% corporate deduction disallowance for your company’s entertainment expenses.

Although employers have had the option to account for tax payable on benefits-in-kind (BIK) through PAYE, payrolling of BIK remains one of the under-used tools in employers’ payroll kit. Links to video recordings of the seminars are made available afterwards and emailed to all registrants. Ciphr webinars.

Two-thirds (62%) of those that provide financial education deliver it through face-to-face seminars, while 57% use an intranet site, 43% offer online tools and modellers, and 23% use web-based seminars. In turn, the employer will not have to pay employer NI on the part of the salary that is sacrificed. Pensions .

This could be tracking the participants in: In-person meetings Seminars Workshops Benefit fairs Q&A event participation Tracking the questions and discussions in these activities can provide an understanding that other metrics cannot provide. It is not legal or tax advice.

They will also lose out on the valuable tax benefits available in the pension scheme. It’s usually better to leave the money invested in a pension fund where it keeps its tax-free status, and only withdrawing when it is actually needed.

Another option employers have is what we call a “Specialty Account” It’s a post-tax account that allows employers to offer additional for, say: gym memberships, yoga classes, it could be the “last mile” scooter program for their commuter needs, health seminars, and a whole host of other services that can benefit employees (..)

Corporate Synergies’ in-house subject matter experts will also offer several live seminars throughout the firm’s regions including Philadelphia, New York, Washington, D.C., The 2019 Employer Education Series will feature weekly articles posted weekly to Corporate Synergies’ award-winning Knowledge Center. and Orlando.

We organize all of the trending information in your field so you don't have to. Join 46,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content